Summary Analysis: Whirlpool (NYSE:WHR)

A struggling turnaround story

I am going to talk about Whirlpool (NYSE:WHR) today. It is the second worst performing stock in my coffee can portfolio, only behind PetsMed, about which I wrote about in the past.

History

Whirlpool is a multinational manufacturer and marketer of home appliances, including refrigerators, washing machines, and other household appliances. The company is headquartered in Benton Harbor, Michigan, and is one of the largest home appliance makers in the world. Whirlpool Corporation was founded in 1911, originally named the Upton Machine Company by its founders Louis Upton and Emory Upton. It later became the Whirlpool Corporation in 1950 and has been publicly listed since 1955.

Whirlpool Corporation's historical business lines have evolved significantly since its founding. Here are some key stages in its history1:

Early Years (1911-1940s)

The Upton Machine Company, Whirlpool's precursor, initially produced electric, motor-driven wringer washing machines. It then expanded its product line to include various home appliances through collaborations and acquisitions.

Post-War Expansion (1950s-1970s)

Whirlpool diversified its product offerings, including refrigerators, freezers, and other major household appliances. The company also introduced various innovations in home appliances, such as automatic washers and dryers.

Global Expansion (1980s-1990s)

Whirlpool expanded globally through acquisitions, including companies like Philips' appliance division in Europe and the Brazilian appliance maker Multibrás. The company added well-known brands like KitchenAid, Roper, and Bauknecht to its portfolio.

Modern Era (2000s-Present)

Whirlpool has followed the latest technology trends emphasizing energy efficiency and smart home connectivity. The acquisition of Maytag Corporation in 2006 was a significant milestone, adding brands like Maytag, Jenn-Air, and Amana to Whirlpool's lineup. The company increased its focus on sustainability, developing eco-friendly appliances and reducing its environmental footprint.

Throughout its history, Whirlpool has remained a leader in the home appliance industry, continually adapting to market demands and technological advancements.

Financials

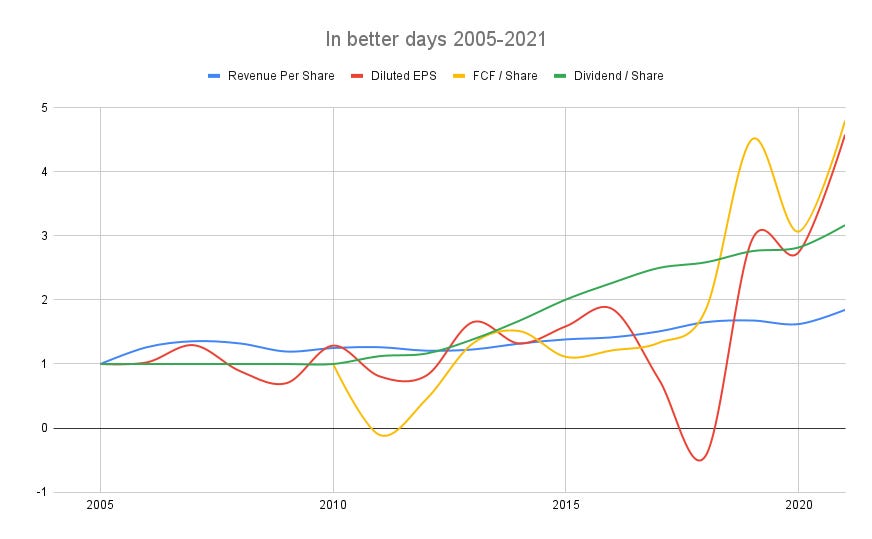

Leading into 2021, Whirlpool’s long term track record as a company was quite spectacular. Here are a few metrics from those times, with an emphasis on per share numbers.

The reason I select per share numbers is that the company reduced its share count by about a 3rd2 through buybacks between the years 2013 and 2023. In the intervening period, they also doubled the dividend. Cashflow was solid and it was clearly a well run compounding machine.

As late as the years 2019-2021, Whirlpool was an outperforming company. The wheels of the company have only come off in the past 2 years. Costs have gone up putting a lot of pressure on EBIT margins. Demand soared during pandemic time, and has since tempered, effectively flatlining revenue. It is apparent that Whirlpool is having problems competing with LG and Samsung in the appliance area. These factors are affecting them not just in a single market, but seems to be almost universal, which is really worrisome.

This is all despite the fact that Whirlpool actually benefitted from a Trump tariff that recently expired. The tariff increased the prices of foreign brands like Samsung and LG by about 30%. Instead of keeping their prices steady WHR jacked up their prices by 30% for the past 6 years or so and booked all that as profit. With the tariff expiring and needing to compete on price again their revenues are tumbling.

Furthermore if comments from unverified sources on Reditt are to be believed, they are struggling with investing in their automation, as well as with maintaining their preferences with the top homebuilders with Samsung coming in to take that lost marketshare.

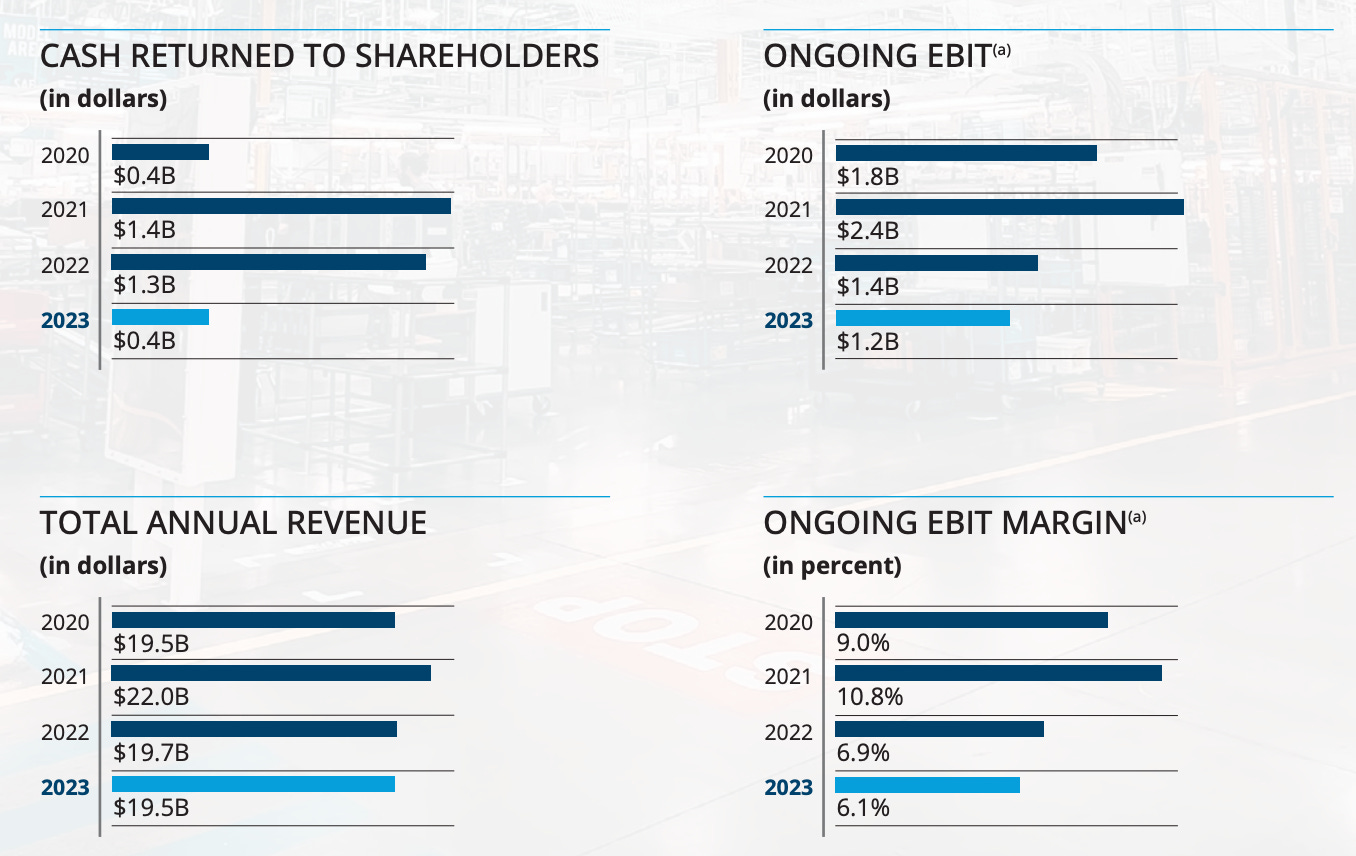

Financially there are other red flags, including $6.4Bn of long term debt (down from $7.3Bn last year) and a short term hole of $750M in current liabilities not met by current assets. The company has rightfully stopped its buyback program temporarily, though it has unused board authorisation for $2.6Bn of buybacks. While the company has a very long term track record of paying dividends, that’s now extracting almost all the cash generated from operating activities and cash and cash equivalents are in decline in 2023. Obviously, this dividend is not sustainable unless the business rerates significantly.

Tough Turnaround

As we can see, the company has fallen into tough times and I consider this company to be a tough turnaround case. The company seems to be making the right capital allocation decisions focussing on reducing debt3, embarking on an effort to cut costs by roughly 800Mn a year to offset the $2.5Bn increase in the past 3 years4, planning to sell a third of its stake in Whirlpool India to improve balancesheet5, and agreements to sell their EMEA business6, hopefully again improving medium term cashflow. As a small consolation, the management is a seasoned one and seems to be in control of their plan.

Notwithstanding the right noises, I believe the turnaround will be tough and unless the management can fix their balance sheet quickly and operating cashflow imminently, the company will have to resort to dividend cuts, likely dilution of equity to raise cash and it is possibly even a target for a fire-sale takeover by a private equity firm. Many of these possible scenarios could lead to permanent loss of capital for investors.

On the other hand, companies that have great track record of shareholder returns, as Whirlpool has, have probably more resilience than is evident by purely financial numbers. For the sake of my portfolio, I very much hope that this optimistic version turns out to be true, even if it takes time to get there.

Summary

I am currently carrying this stock at a mark-to-market loss of 32% and an IRR of -25%, even after factoring in dividends. I don’t plan to add to my position unless there is some clarity on the execution of the turnaround plan. The only consolation is that it is only 0.60% of my holdings and given I am not adding, I will likely let it dilute away within my portfolio.

I have said so at other times - I don’t expect all the stocks in my portfolio to breakeven, forget being winners. What is important however is to let the losers become a smaller and smaller part of the portfolio and the winners to magnify. If the company genuinely turns around, it will breakeven or probably generate some upside and I am happy. If not, the losses will be limited and that’s fine too.

Onward and Upward - Happy Investing!!

This section has been sourced through ChatGPT

From 80M in 2013 to 55M shares in 2023

From 2023 Annual Report - “In 2023, we continued our 68th year of quarterly dividends, with $384 million in dividends paid in 2023. We continue to prioritize debt repayments, with $500 million of debt repayment in the fourth quarter of 2023.”

From 2023 Annual Report - “During 2023, we delivered approximately $800 million in cost take out through our decisive actions and a disciplined approach to reset our cost structure after $2.5 billion of cost inflation in 2021 and 2022.”

From 2023 Annual Report - “In November 2023, we announced our intention to reduce our ownership interest in our Whirlpool of India subsidiary while maintaining a majority interest, and we expect to utilize the proceeds to further reduce debt levels in 2024.”

From 2023 Annual Report - “In 2023, we entered into the contribution agreement with Arçelik to contribute our European major domestic appliance business into a newly formed European appliance company and into a separate agreement for the sale of the Middle East and North Africa business, and expect to close both transactions by April 2024.”