Summary Analysis: PetMed Express

A company with significant headwinds through competition

Survey on next stage of the substack

Thank you for the love and support you have show to the Coffee Can Investor substack. It has been many months of regular writing for me and I have loved every minute of it so far & I hope I have not wasted too much of your time in doing so. Now seems like a good time to gauge from current readers on what you like reading today on the website. I am also trying to assess if newer streams of content (like a podcast or more coffee can portfolios) might be of interest. Please take 2 minutes of your time to respond to a survey please.

In continuing the journey of talking about stocks with extreme returns (see my write ups on Domino’s and Stella-Jones), I will pick up PetMeds for this post, one of the worst performing stocks in the portfolio at the moment.

PetMed Express, Inc., commonly known as "PetMeds," is an American company that operates as an online pet pharmacy. It is one of the largest and most well-known pet pharmacy retailers in the United States. The company specialises in the sale of prescription and non-prescription medications, as well as other pet supplies and products, for dogs, cats, and other animals. PetMed Express, Inc. was founded in 1996. The company went public and conducted its initial public offering (IPO) on April 14, 2000.

Stock Price, Trades & News | GuruFocus")

The Pet care and Pet supplies industry is a surprisingly large one, with pet food alone accounting for about USD $53Bn in the United States and estimated to be $73Bn by 2028, growing ~9% year-on-year. Vast majority of this spend is still offline with a mere 13.2% being spent online on pet foods in 2022. Some 28% of this is spent on pet healthcare, or about $14Bn per year.

This is also a fairly crowded market, with Amazon (AMZN) and Walmart (WMT) taking the top-end of the opportunity, along with Chewy (CHWY), Petco (WOOF), Hill’s Pet Nutrition (owned by Colgate Palmolive / CL), and a host of other unlisted companies. However, the apples to apples comparison with PetMed Express is harder to come by. Compared to, say, Chewy, which is a large general-purpose pet supplies operator, PetMeds focuses only on online medicines for pets. This means that comparing PetMed with the larger general purpose operators in the petcare industry, for better or for worse, is slightly incorrect. Let’s keep that in mind while going through the rest of the analysis.

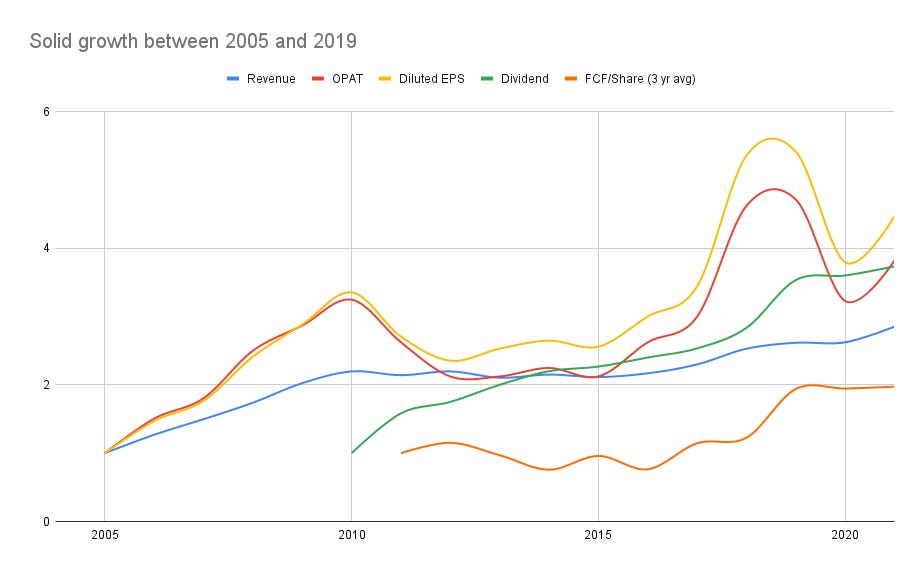

Between 2005 and 2021, this was a reasonably good business, growing revenue (5.5%) and OPAT (6.40%), while paying back vast majority (~2/3rds) of free cash flow as dividends, and reducing its share count slightly1 (reducing by 1.3% per year). So, even if the company was not trailblazing in any manner, it was a reasonably consistent well run enterprise, maintaining shareholders returns as a priority.

2019 was the peak year for this company generating $1.84 per share, free cash flow of $2.17 per share, paying out $1.06 in dividend (with a healthy payout ratio of 58%), with all other metrics growing consistently for a few recent years.

Since then the business has hit a rough patch. It boils down to increased competition, specially from Chewy, that has been aggressive at expanding across the petcare industry, and given that Chewy has substantially higher number of touch points with their customers (for needs across the pet care spectrum), it is natural that they were placed best to usurp on PetMeds’ market share. Chewy has been a best-in-brand online pet care vendor, gobbling up marketshare, producing impressive growth numbers and eventually printing very good profit numbers (or the first time in 2022 after a few loss making years. From PetMeds’ own annual report:

Sales for fiscal year 2022 were impacted by a much more competitive environment, and a crowded advertising market which had substantially higher advertising costs compared to the same period in the prior year.

PetMeds is trying to play catch up, releasing AutoShip feature in July 2021, the kind of feature-set Chewy built its expanding revenue with. AutoShip represented as much as 49% of net sales in most recent quarter. However, it is likely too small an upgrade to counter what is otherwise a very daunting competitor. As a consumer, it might be worthwhile for me to go from a general purpose grocer like Amazon to a niche platform like Chewy for my pet needs, but needing to go to PetMeds just for pet medication poses a higher hurdle to be cleared.

2 years back, the company has recruited Matt Hulett to run the company, not extending the stint of Menderes Akdag, previous CEO. However, the results of this are yet to be seen in the numbers.

Given the rapid growth of Chewy and the reducing marketshare of PetMeds, it is likely that PetMeds either

consolidate other smaller players and gain volume (and likely pricing and tech power) to counter Chewy,

get acquired by a larger player for its customer base and know-how in the pet medication space OR

is on a structural decline from here on, ending in a likely bankruptcy or a fire sale in a few years time.

In recent months, it seems that PetMeds is taking first route by completing the purchase of PetCare Rx, a leading online supplier of pet medications, foods, and supplies, for $36.0 million in cash. It has also entered into a contract with Pumpkin Insurance Services to provide pet insurance services through a new subsidiary, PetMeds Insurance Services, expecting to begin operations in the next 12 months. The company also made a small $5M investment in Vetster, a pets telemedicine company, but at this point it seems more like a venture investment than something that will move the top line any time soon.

The company is continuing to maintain its dividend, but I believe it is only a matter of time before it is cut, unless the business inflects significantly for the better.

In summary, this is a company that had a relatively rosy past, but are facing increased competition. It is trying to make small investments in consolidating smaller competitors and making moves in strategic partnerships. It is not yet clear to me, however, that the company will make a comeback to growth years. It might be a time to wait and see.

On my end, it is marked for “Dilution”, so I don’t expect to be adding much to my position. I plan to see some signs of the business improving before I add to my position in any notable manner.

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

Company reduced 6.2 million shares outstanding by putting in $81.3M over the years, averaging $13.15, which despite the recent reversal in the stock price is a pretty good outcome for shareholders thus far.