Performance Update (Q4' 2025)

When Markets Test Patience More Than Conviction

Wishing all readers a happy and prosperous 2026.

Performance Summary

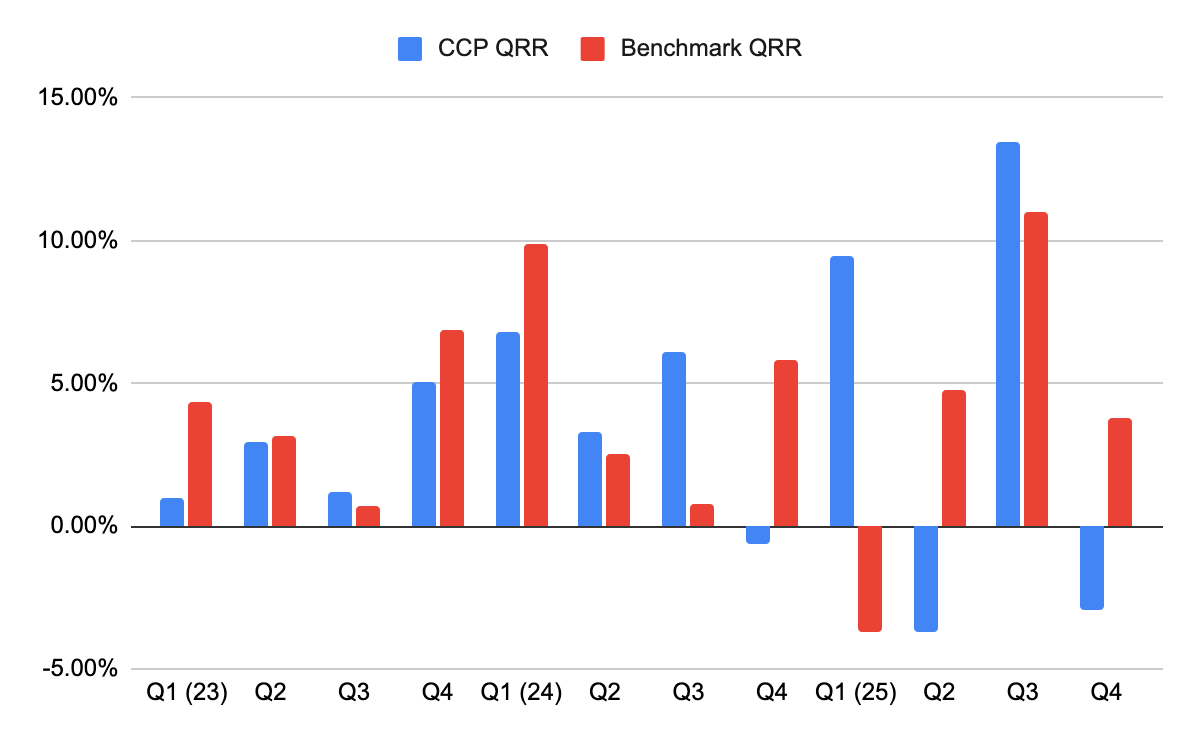

The Coffee Can Portfolio declined -2.94% in Q4 2025, while the benchmark - the Vanguard Global All Cap Fund - gained +3.78% over the same period.

Since inception, performance stands as follows:

Portfolio XIRR (GBP): 11.22%

Benchmark XIRR: 14.01%

Alpha: -2.79%

This marks the third negative quarter in the past five, and equally the third instance of benchmark underperformance in that period. While these drawdowns have been relatively mild, they have been frequent. The offsetting factor is that the remaining two quarters delivered outsized returns, limiting (though not eliminating) the cumulative lag versus the benchmark.

The relative underperformance is noticeable - but contained.

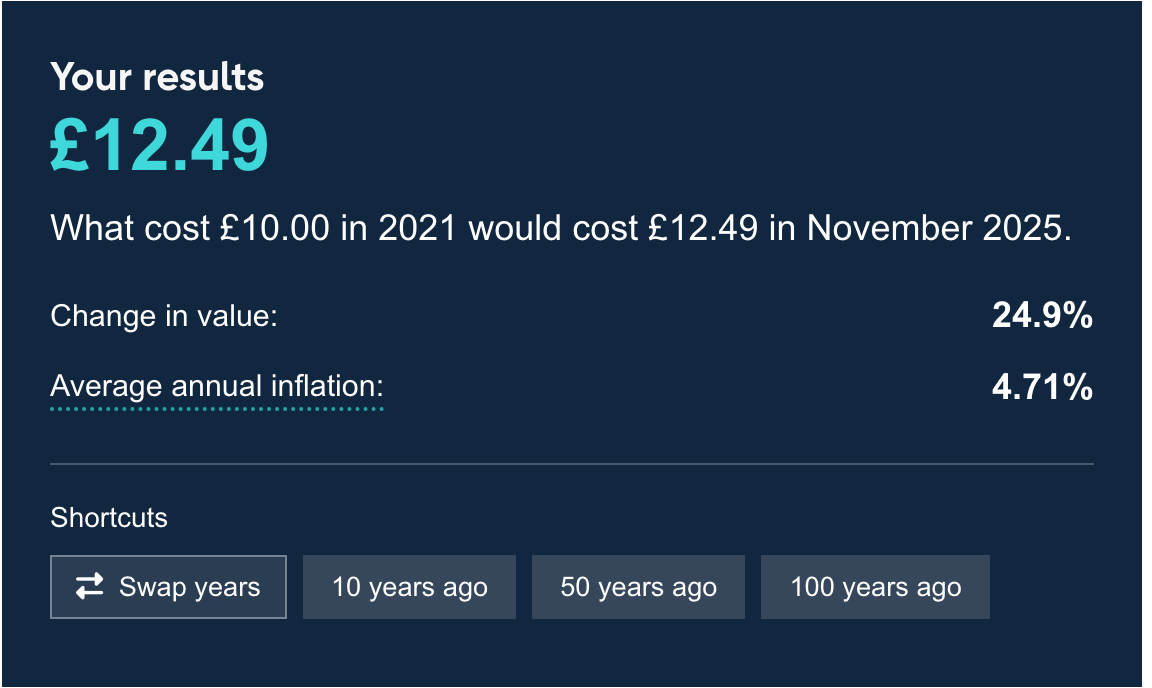

Measured against inflation, average British inflation since the inception of this blog has been ~4.71%1. Real returns stand at 6.51%.

Perspective

If this were an external fund with professional LPs, I would probably be rehearsing some uncomfortable conversations. Fortunately, the only two LPs2 are currently in Chennai, blissfully unaware, focused on local cuisine - with podi idli now firmly established as the preferred asset of the next-generation LP.

The other LP is experiencing the classic western-resident-returning-to-India gastrointestinal adjustment; mercifully, such joys & problems remains firmly outside the fund’s mandate! 😁

Consequently, the emotional impact of recent performance has been borne entirely by yours truly - who, thankfully, comes equipped with thick skin, patience, and a stubbornly long-term mindset.

Drivers of Underperformance

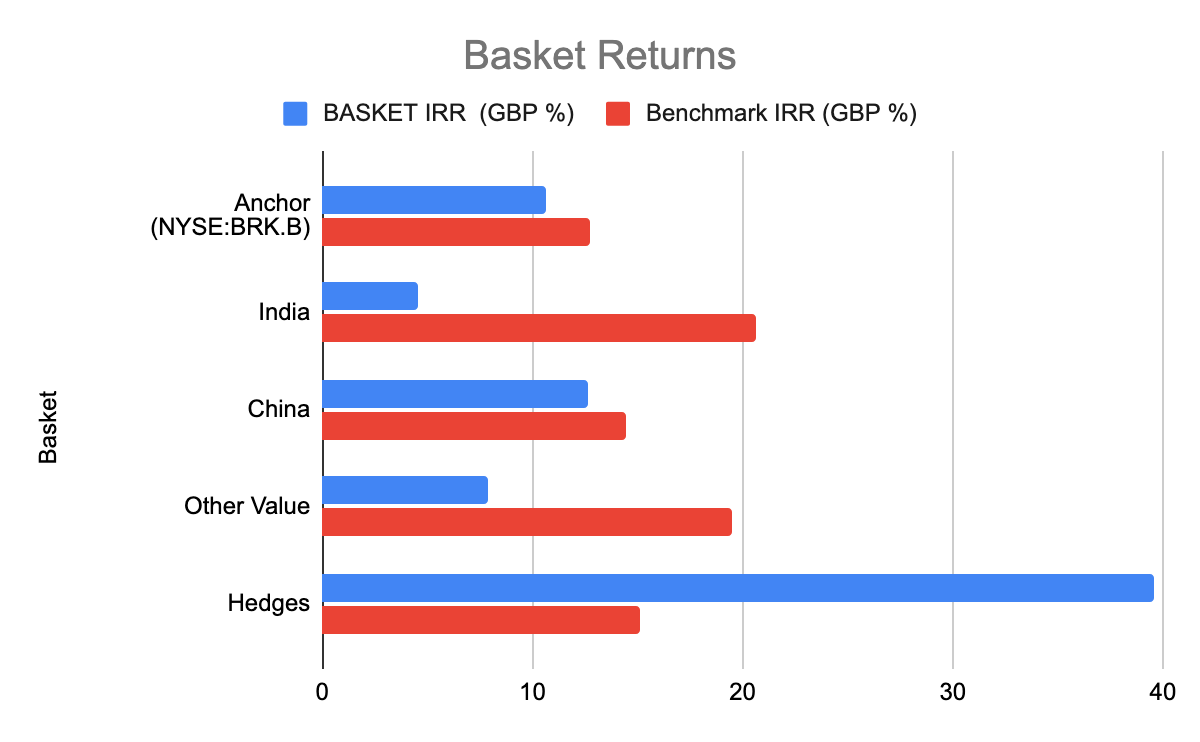

The underperformance over the past three quarters is broad-based. In short: almost everything I hold.

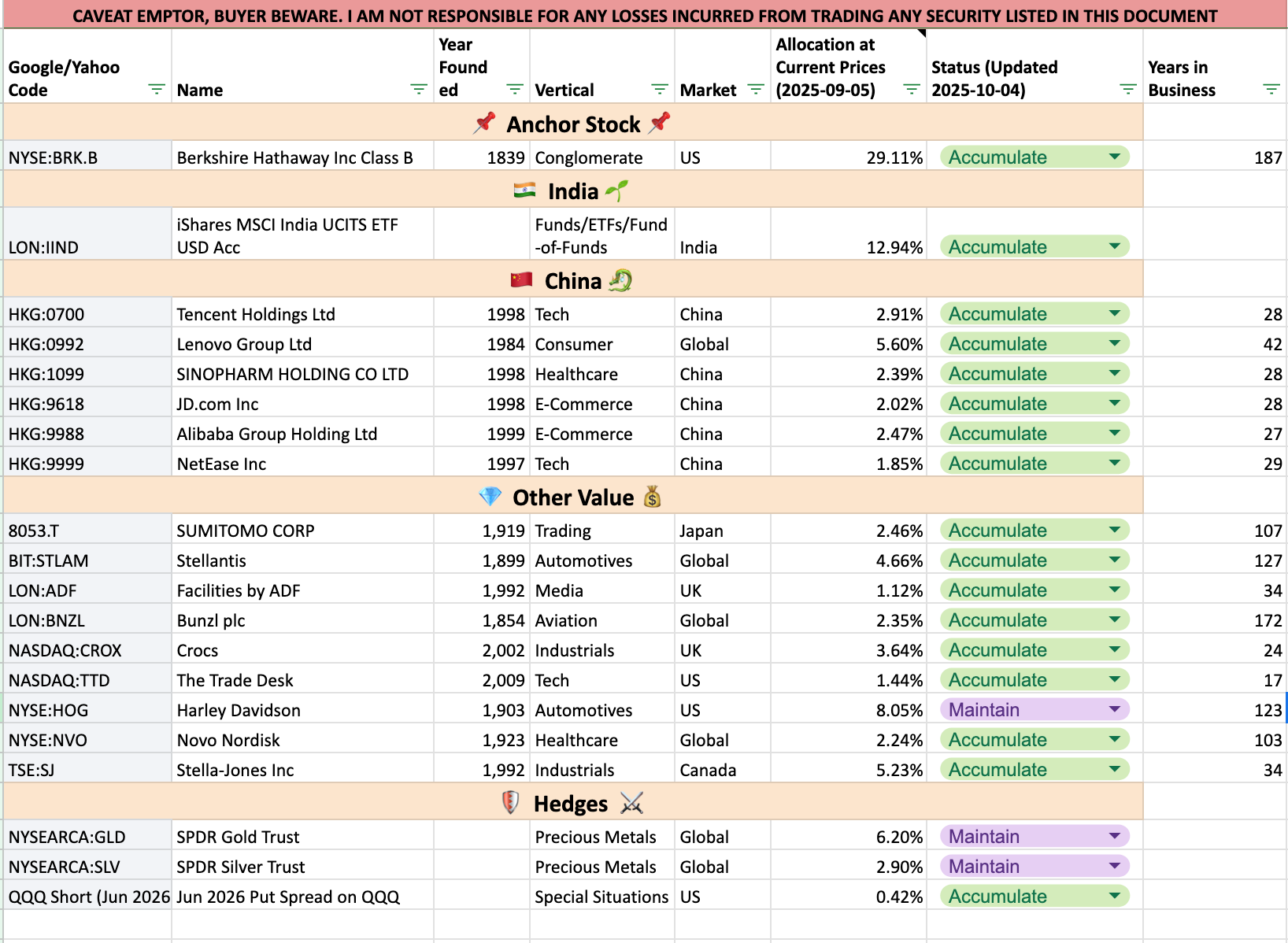

Berkshire Hathaway (NYSE:BRK.B), the portfolio’s largest holding and anchor, has underperformed meaningfully from a stock-price perspective. This has occurred despite another very strong year operationally. The business continues to compound intrinsic value; the market has simply chosen not to notice.

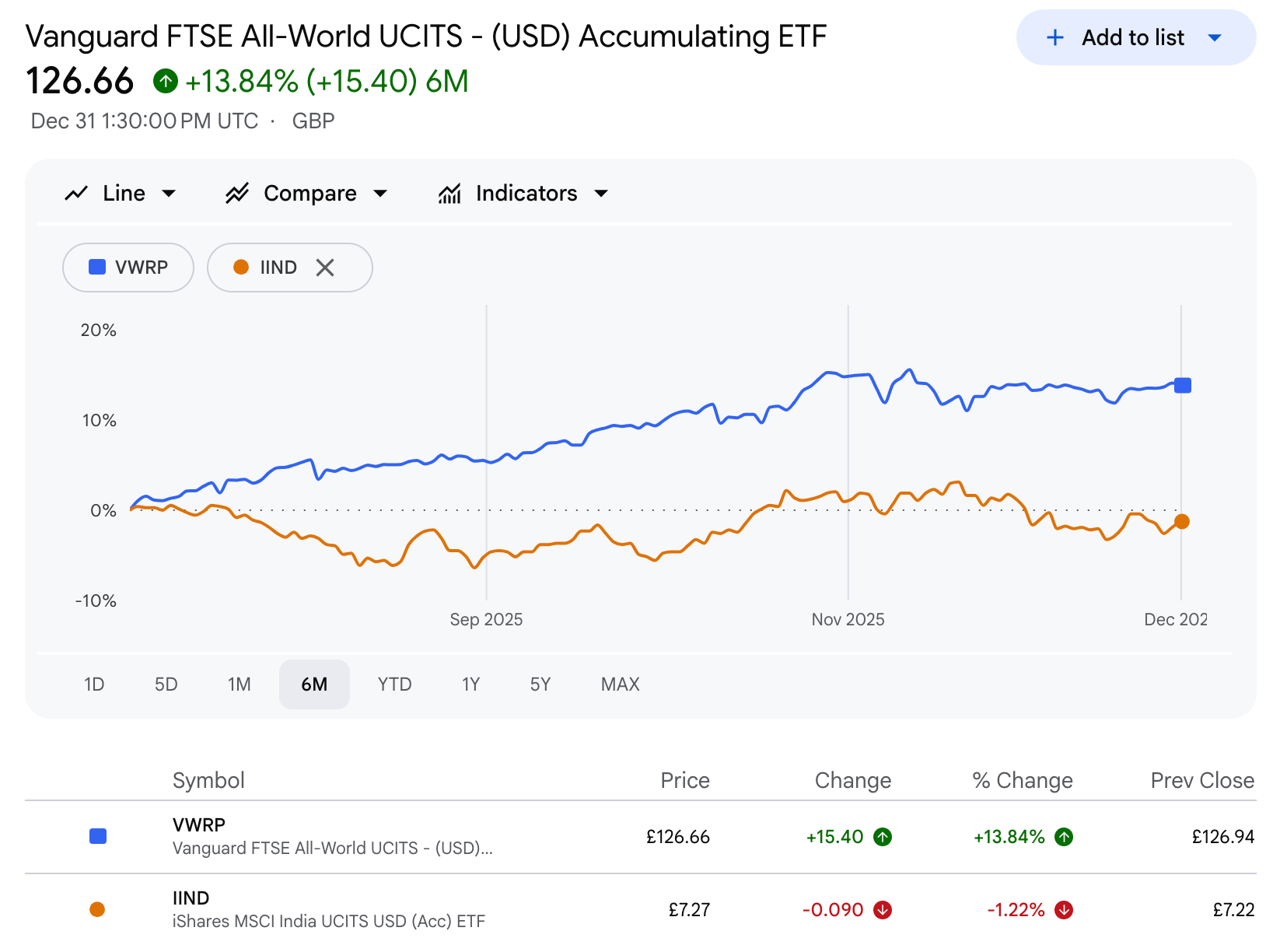

Indian equities (represented by LON:IIND) have had a weak and narrow year, with gains concentrated in a handful of large names. The broader market has gone nowhere. I added to my India exposure during the year; further thoughts on this will follow in a dedicated post.

Among 2025 stock selections - Harley-Davidson, Crocs, Novo Nordisk, The Trade Desk, and LON:ADF - all have delivered disappointing price performance with little to show by way of momentum. The lone exception was Stellantis, though credit for that idea belongs to a friend rather than yours truly, and I’ve therefore refrained from excessive commentary, though the alpha is always welcome.

Judged purely on short-term stock selection, 2025 earns a solid “F”. Fortunately, the investment horizon remains rather longer than a calendar year - and ideally so does the attention span of readers. Long term, I am optimistic about the prospects, of all the baskets and I expect some of the 2025 bets to start showing green in the coming years.

Portfolio Actions During the Period

Three portfolio changes are worth highlighting:

Exit: Anhui Conch Cement (HKG:0914)

This was a small position in a business I never knew particularly well. While it had a historically strong growth record, the company lost momentum a couple of years ago and has shown little sign of recovery. With declining revenues, limited visibility, and operating in an industry I neither understand deeply nor care about, the position no longer justified capital allocation.

Proceeds were rotated into Lenovo (HKG:0992) and JD.com (HKG:9618).Silver Hedge

A small silver (NYSEARCA:SLV) position was added via an options call spread (2027 Jan 50/75), providing portfolio diversification and a modest hedge within commodities without excessive capital commitment.Index Protection

A small short exposure was initiated through put options on QQQ (2026 Jun 590/490), following through on the “Borrowed Time, Borrowed Returns” post. I don’t expect these options to pay off - they just sit there as insurance.

I added materially to my India ETF position while my Lenovo position has swelled up due to some options that I underwrote which got assigned - I am happy to extend that counter. Portfolio as it stands today:

Valuation & Outlook

Despite the uninspiring recent performance cycle, the portfolio’s valuation remains attractive.

The equities3 component generates approximately £8.704 of earnings per £100 invested, implying a P/E of ~11.4 - which positions it relatively well for future returns. These Earnings are well diversified across geographies and industries. All holdings have long operating histories, with only The Trade Desk and Crocs being 21st-century companies. Balance sheets are generally strong, cash flows consistent, and management teams proven.

More pertinent, however, is the fact that despite the tepid performance of the portfolio on a mark-to-market basis, the businesses are mostly on the right track growing revenues and profits through out the year. If the managements continue to execute in line with their historical track records, the portfolio should remain well positioned to compound value over the long term - even if short-term patience continues to be tested.

After two years of 0 churn, the Coffee Can Portfolio saw ~24% churn (by value) in 2025. Well structured portfolios shouldn’t see much churn each year. With that view, I am very much hoping that 2026 will bring back the calm from the previous years and hopefully, some alpha too, to boot!

On that note, thank you for reading, and happy investing.

Inflation depends on what base you select, I select 2021 as it indicates the lowest base (and hence highest inflation) in recent years. The returns compared to this base are perhaps most conservative.

Just my daughter and my wife. No outside investors for me.

I am making a point to exclude the Gold and Silver positions, as well as the small hedge position. Factor that in and we are talking about a P/E of ~12.5

Berkshire throws a googly here - its reported earnings included unrealised gains due to GAAP reporting requirements, which I don’t want to include. So I take operating earnings, which comes from about a third of the enterprise value (its portfolio holdings and cash each being a third) and multiply it by 2, to allow for cash-interest and portfolio dividends to be factored in. I wrote about this valuation method in Feb’2025