Reviewing Lenovo (HKG:0992)

Steady Progress Beyond PCs

Lenovo (HKG:0992) is a stock I have owned since the inception of the Coffee Can Portfolio. When I last wrote about the company two years ago, it was in the midst of a transition from being the dominant PC seller to a becoming a broader, more diversified business.

Fast forward to today, and that transition is well underway. Lenovo has held onto its leadership in PCs while steadily building its Infrastructure Solutions Group (ISG) and Solutions & Services Group (SSG) into meaningful contributors to both revenue and profits. Despite periodic stock volatility, the fundamentals remain sound, the company continues to execute well, and the valuation still looks attractive even after the recent run up.

Let’s revisit the 5 themes I put out at my last post.

1. The health of the IDG business

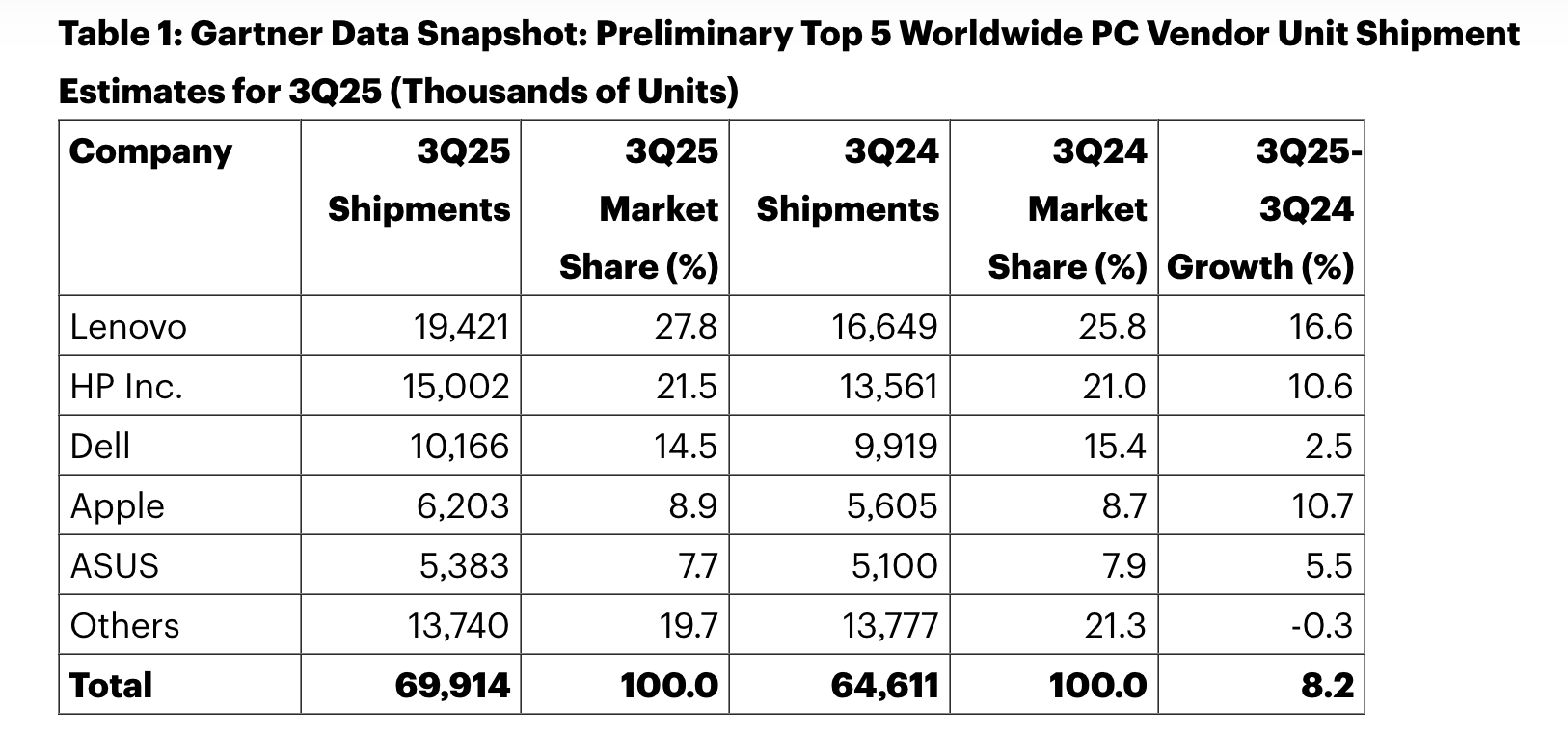

The Intelligent Devices Group (IDG) remains Lenovo’s core, but its shape has changed meaningfully. PC shipments have come off the highs of 2021–2022, when pandemic-driven demand inflated volumes, but the company has managed this normalization with discipline. Lenovo has continued to maintain its global market share in PCs - in the vicinity of 24-25%.

In fact, Gartner’s most recent data shows Lenovo gaining ground through 2025, with share climbing back toward 27–28% in the most recent quarter, driven by strength in both consumer and commercial segments.

What’s more important is that Lenovo has used its scale to sustain margins through a difficult period for the broader PC market. While overall PC revenue now accounts for 53% of total sales, down from 60% two years ago, this reduction is by design. Lenovo is deliberately leaning into higher-margin and more stable business segments, allowing the IDG business to serve as a strong cash generator rather than the sole growth engine.

2. Growth in ISG and SSG

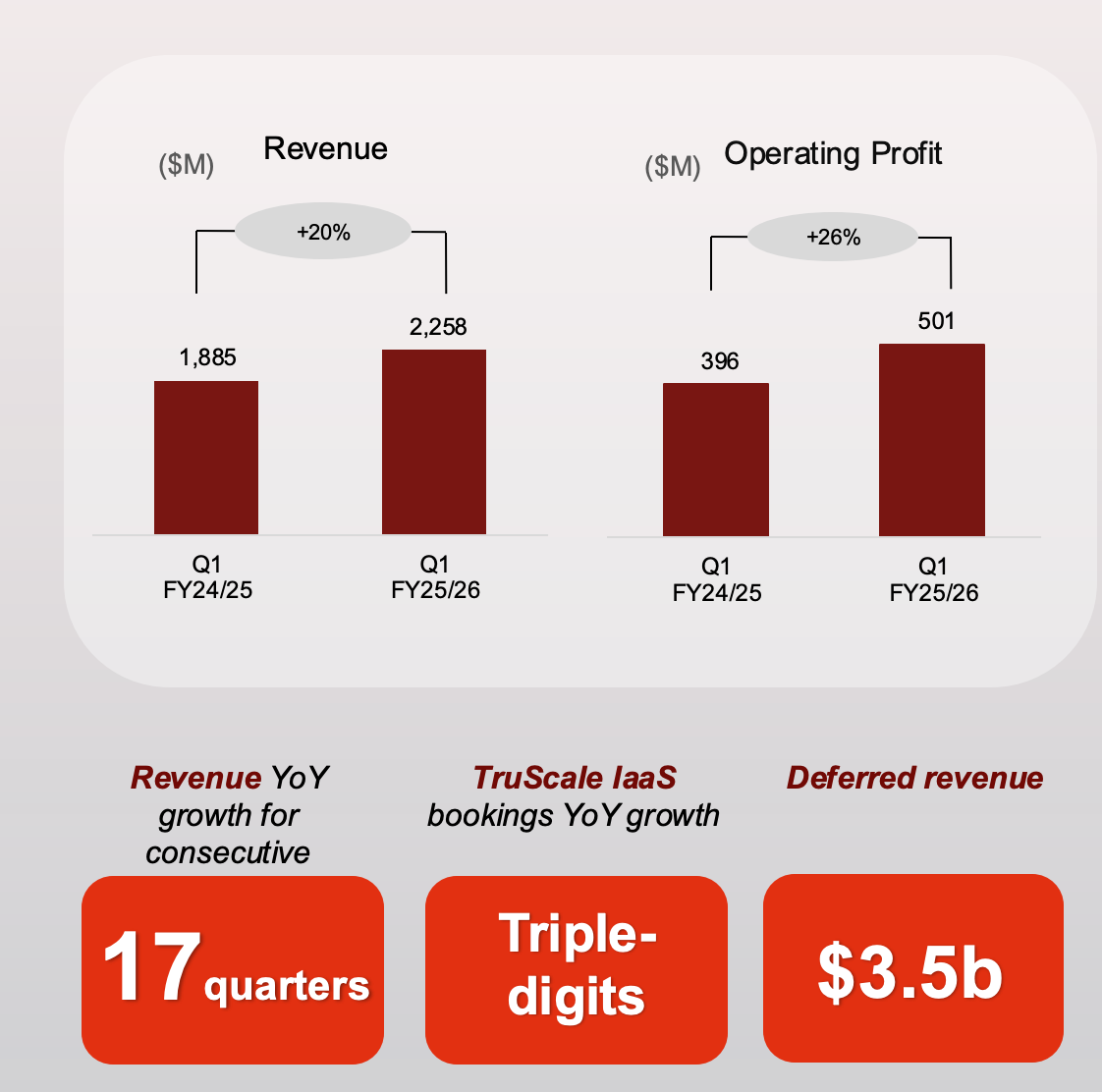

The Infrastructure Solutions Group (ISG) and Solutions & Services Group (SSG) have become the real growth story. Combined, these two divisions now contribute $22 billion in revenue and $1.7 billion in profit, compared to $15 billion in FY23. Together, they represent 32% of Lenovo’s total revenue base, reflecting a substantial shift in the company’s mix.

While margins in these segments remain below 10%, they are consistent with Lenovo’s early-stage push into enterprise and cloud infrastructure services. The company has been investing in building scale and credibility, which will take time to translate into sustained margin improvement. What’s encouraging is the pace of growth: Lenovo’s ISG revenue rose nearly 20% in FY24, and early FY26 results continue to show strong double-digit expansion.

3. A well-run company with solid financial discipline

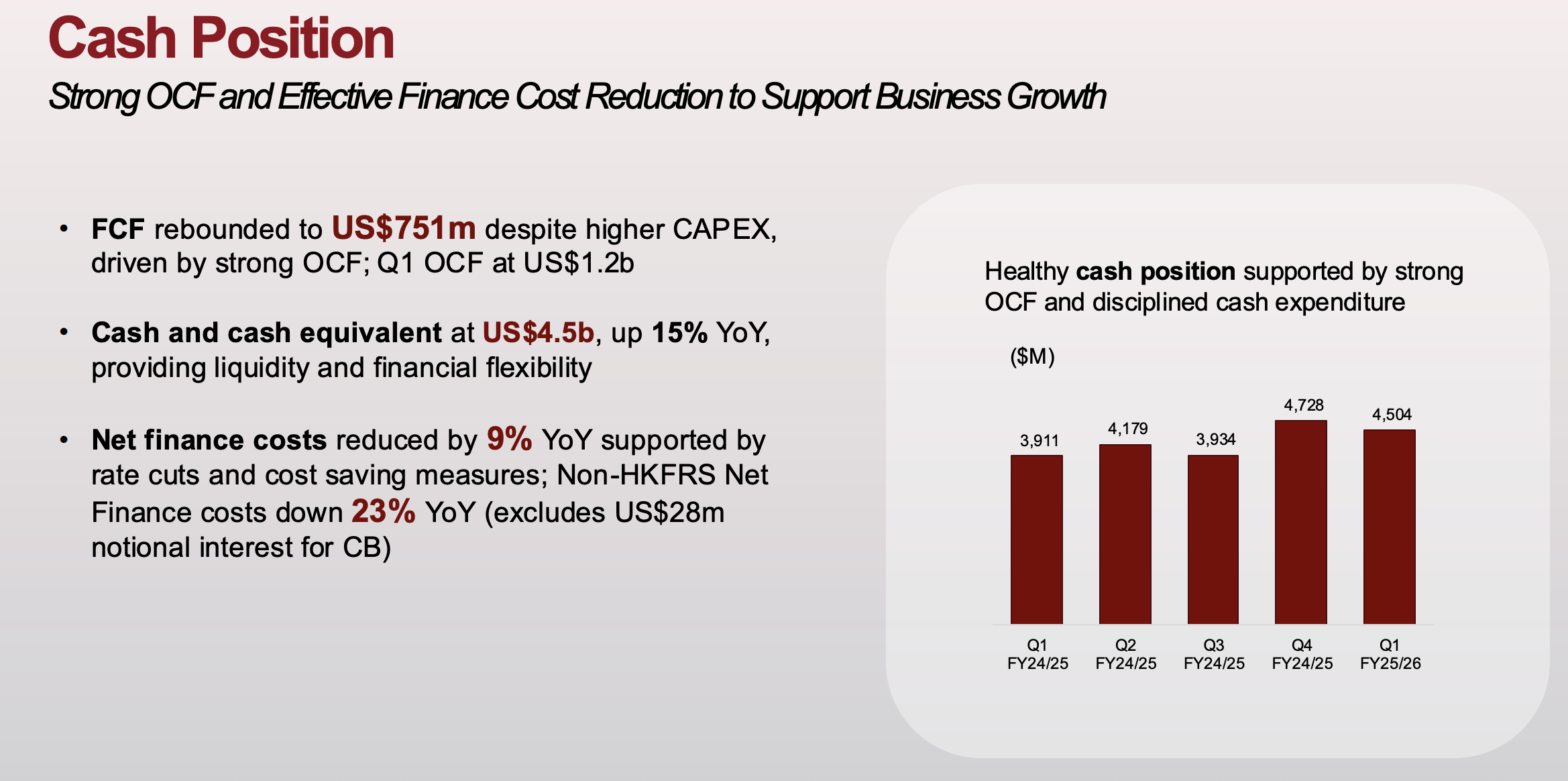

Through all this transformation, Lenovo has managed to maintain its reputation for financial discipline. The company’s operating profit after tax (OPAT) now stands at $1.4 billion, slightly below the FY21–FY23 highs but on a steady recovery path. The cash conversion cycle has lengthened modestly to two days, a natural outcome of a business mix more weighted toward ISG. Inventory is running at 53 days, which remains within a healthy range and lower than FY23 levels.

Free cash flow remains robust, allowing Lenovo to sustain its dividend payout while continuing to invest in R&D and capacity expansion. The company’s strong cash generation, disciplined working capital management, and prudent capital allocation have allowed it to steadily reward shareholders without compromising long-term growth.

4. Volatility in the stock price

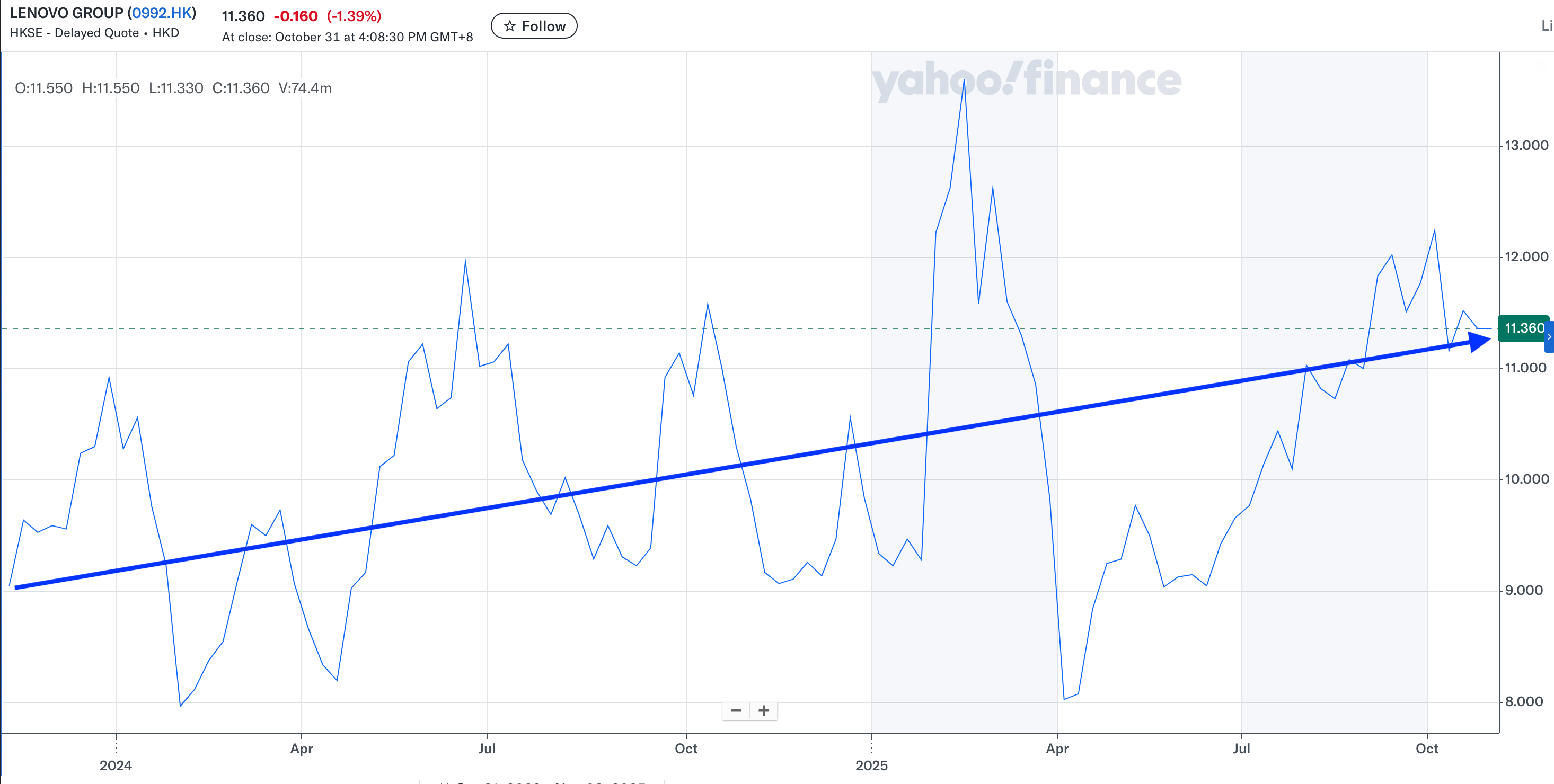

For long-term investors, Lenovo’s stock has been more volatile than its business fundamentals would suggest. The stock has traded in wide ranges over the past two years, often reacting to short-term swings in PC shipment forecasts or macro sentiment around China. Yet, through this noise, the returns have been quietly impressive.

My own holding has increased over this period, with my average cost now at HKD 8.79 (vs HKD 7.4 when I first wrote). Including HKD 0.77 in dividends and some incremental income from covered calls and put premiums, the total return has been roughly 33% over two years, translating to around a 15% annualized return. For a company with Lenovo’s stability and cash flow, that is a respectable outcome.

5. Valuation and the path forward

Even after a strong run in recent months, Lenovo’s valuation remains reasonable. Based on expected FY26 earnings of HKD 0.87 to HKD 0.90 per share, the stock trades around 12 times forward earnings. The dividend yield remains appealing, and cash generation continues to be solid.

More importantly, Lenovo’s long-term trajectory looks balanced. Revenue is tracking toward $72 billion on a trailing 12-month basis, modestly above its FY22 peak, with non-PC segments now accounting for nearly half of total revenue. That diversification has reduced cyclicality and positioned Lenovo for more stable growth.

Closing thoughts

In many ways, the Lenovo story today is one of quiet consistency. The company has navigated an industry downcycle without losing its footing, maintained leadership in its core segment, and built new growth engines in enterprise and services. It continues to execute with discipline, reward shareholders, and reinvest in the future.

The stock will likely continue to be volatile in the short term, but underneath that volatility is a business that keeps improving steadily. For patient investors, Lenovo still offers a compelling mix of quality, value, and growth. I have continued to build my position, and will carry on doing so.

Happy Investing!

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility for your actions. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.