The Lenovo Saga: Riding the Cycle

The trade that worked exactly as it was supposed to

My Lenovo (HKG:0992) journey began back in 2022, quietly and modestly. My position was so small at the time that it barely registered. Then came the summer of 2023, and with it, a sobering set of results: sales and profits both down, inflation having taken a visible toll on demand. I pulled back on accumulating and decided to watch and wait.

At the time, my thinking was grounded in the numbers:

After forex conversions, that works out to be ~10.5% earnings yield and ~10.7% FCF yield.

And the broader picture was one of a business in a trough, not a terminal decline:

Remember that the business is currently declining in revenue (24% YoY) and EPS (-64%). In the worst case, EPS could be as low as 0.0572 but as the business improves, analysts estimate that the EPS in 2023/24 will be closer to 0.0905 or closer to 7.5% earnings yield or 13.3X P/E. These same analysts expect the EPS to improve to USD 0.1575 by 2025-26, which if it happens, would put today’s purchases in the “win” category. Not blindingly cheap but not excessively expensive.

That measured optimism proved well-placed. Looking back, perhaps the most prescient thing I ever titled a post was “Buying in the Lull” written in April of last year. Three words from it aged particularly well:

But the cycle is turning.

And turn it did. By the time I was covering Lenovo again in Nov 2025, the evidence was unmistakable:

This is a post-cycle upswing year for Lenovo. The company has already reported more profit in the first three quarters of 2024-25 than in the full prior financial year. If it finishes at around HKD 1.05 EPS, and with the stock at HKD 7.95, we’re looking at a 7-8x P/E, well below its historical 9-15x range.

By then, I was not just writing about conviction, I was acting on it. Puts were getting exercised, and rather than exit, I held everything. The position swelled. By the time of my last portfolio update, Lenovo had grown to 5.6% of all positions, roughly a third of my China basket, and my third largest single stock position overall.

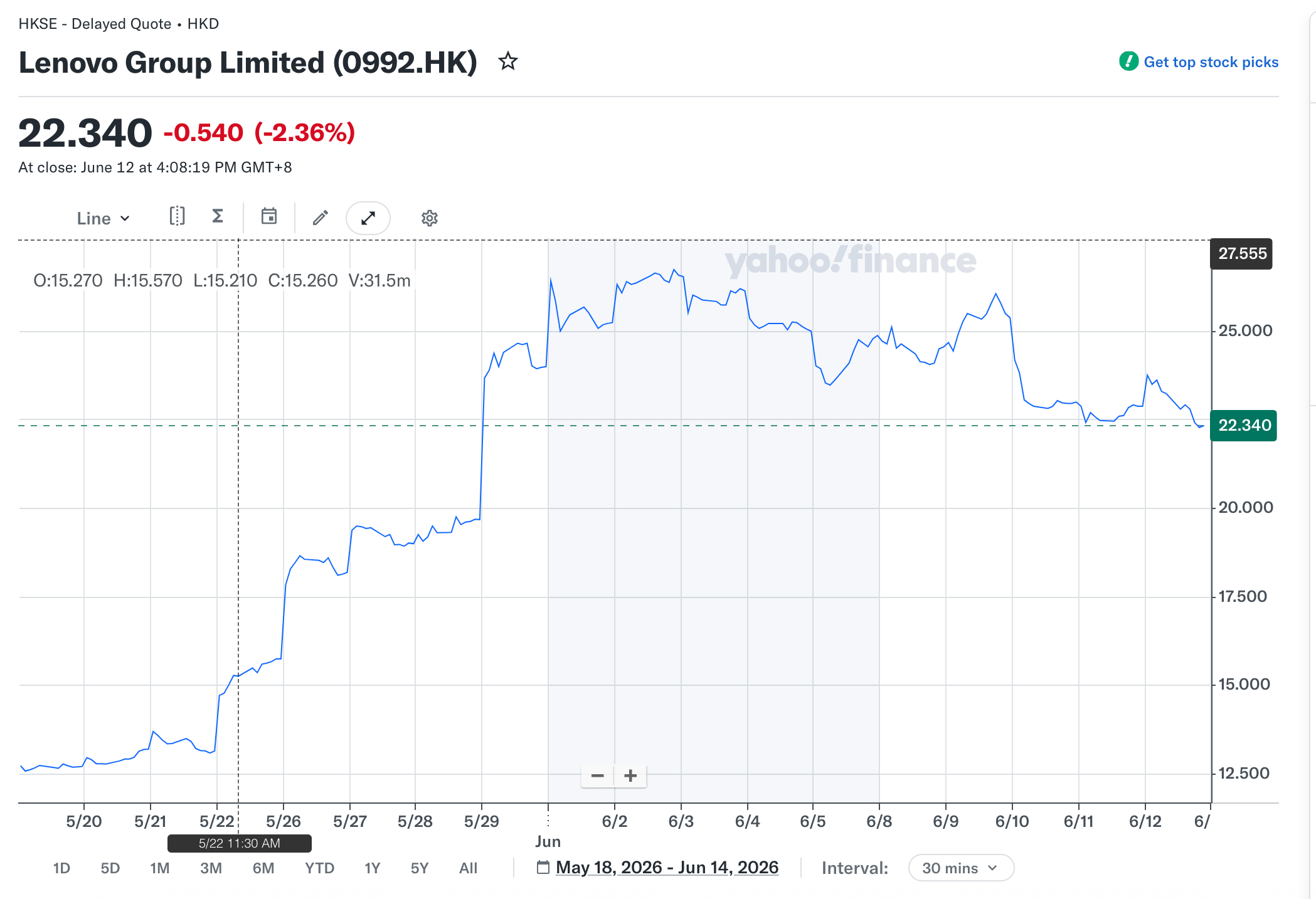

Then came the latest results and oh boy, weren’t they awesome!. Revenue up 27% year-on-year, profits up around 10%, and crucially, the growth was being driven by AI. Once a company delivers blockbuster numbers and hitches itself to the defining narrative of the moment, there is very little holding the stock back. It doubled, and then kept going. At its peak, Lenovo was trading at 20x earnings and around 15x free cash flow.

Here is where temperament matters as much as analysis. I am genuinely optimistic about quality businesses when they are sitting at the bottom of their cycle, battered by external forces and priced to reflect maximum pessimism.

But I am equally skeptical when those same businesses have frothy valuations. AI-related revenue had grown 84% year-on-year and now accounted for a third of total revenue, up from a sixth just a year earlier. That kind of growth attracts a very different kind of investor, at a very different kind of price.

I have seen this movie before. The sitting-through-the-cycle experience is a painful one for a concentrated investor. What you gain on the way up, the subsequent down-cycle has a way of quietly erasing. Stella Jones, BRK.B, Alibaba, Tencent, JD.com: all of them are sitting on significantly lower valuations today than they were at some point in the last 18 months. I was not going to let that happen again.

At the same time, I was not willing to walk away entirely. Stocks follow a power law. A handful of winners drive almost all the upside. For a portfolio carrying meaningful negative alpha and limited AI exposure, the current tailwind, a winner like this is not just welcome, it is necessary. Selling the whole thing felt like leaving too much on the table if the momentum had further to run.

So I split the difference. I placed stop-loss orders roughly 6 to 10% below the prevailing price, covering around 80% of the position, and let it ride. The momentum eventually ran out. The stock peaked just above HKD 27, rolled back to 25, and my stop-loss triggered.

Let’s be clear here though, I don’t think this stock is egregiously overpriced or anything. In fact I will likely continue to build on my position defensively, most likely through some combination of writing out of the money PUTs and some CALL Spreads. It is just that taking money off and keeping some dry powder ready made far more sense at the moment.

Having said that, this ranks among the cleanest wins I have had in some time. A large position in an undervalued company, followed by results that genuinely surprised, followed by the market paying attention: that is the entire thesis in action. In fact this is the same thesis that’s worked for me with Gold, Crocs and now Lenovo. Buy cheap and wait for it to pay off.

Yes, the recent cycle has produced fewer wins than I would have liked, and the positions that are not winning are largely just sitting still, making for a quieter ride than I prefer. But I would rather be patient and concentrated, waiting for moments like this one, than scattered across a portfolio of mediocrity.

And the key detail, the one that made all the difference: it was not just that the inflection happened. It was that the inflection happened after the position had grown large enough to matter. I will take those wins when they come. Onwards and upwards.

Happy Investing!

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility for your actions. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.