Quick Earnings Update

Some good news, but some bad news too

Since the last time I wrote about earnings, a few results out have come out. This post will come them very briefly - expect this to be short and sweet.

Lenovo Group (HKG:0992) 😥

Lenovo Group Ltd announced their results late in May and results are sobering. Sales is down 13.5%, gross profit down 12.85%, Earnings Per Share (EPS) down 19.2% and Free Cash Flow (FCF) per share dropped 44%1.

The reasons aren’t difficult to comprehend:

Broadly speaking, global businesses were operating in a high inflation, high interest rate environment with exchange rate fluctuation and geopolitical tensions. For our industry, the past fiscal year also marked a turning point from a fast expansion period to a post- pandemic, post hypergrowth era.

-Yuanqing Yang, Chairman & CEO

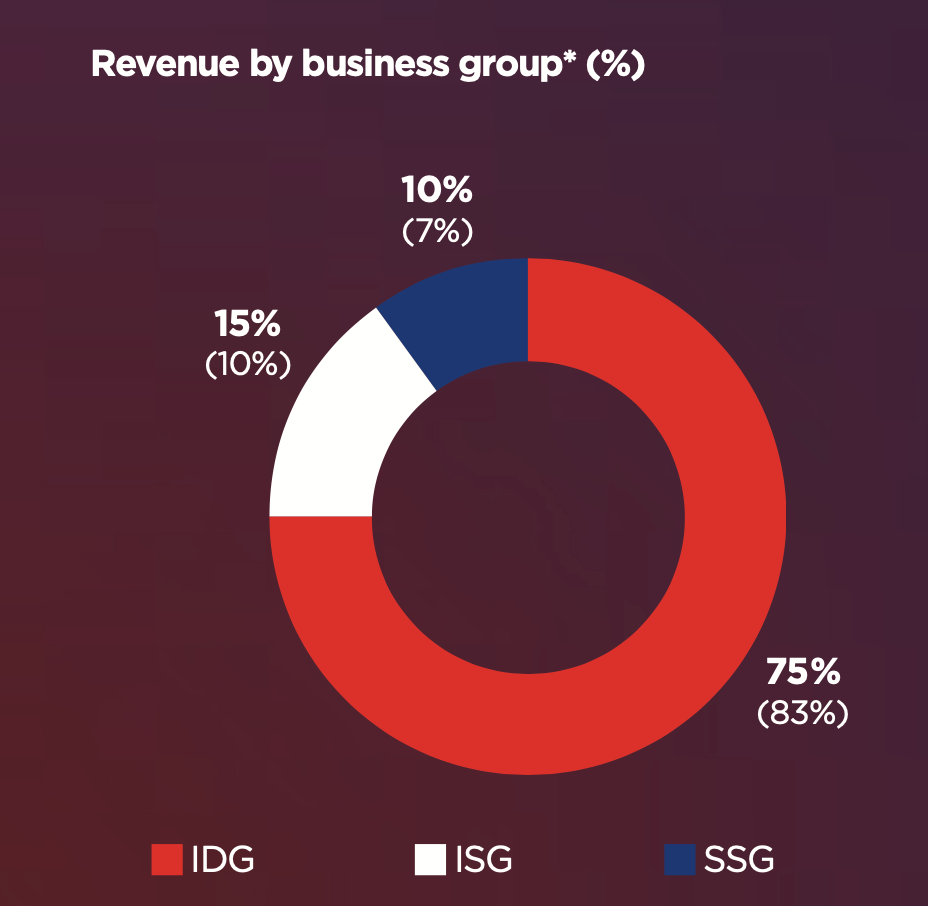

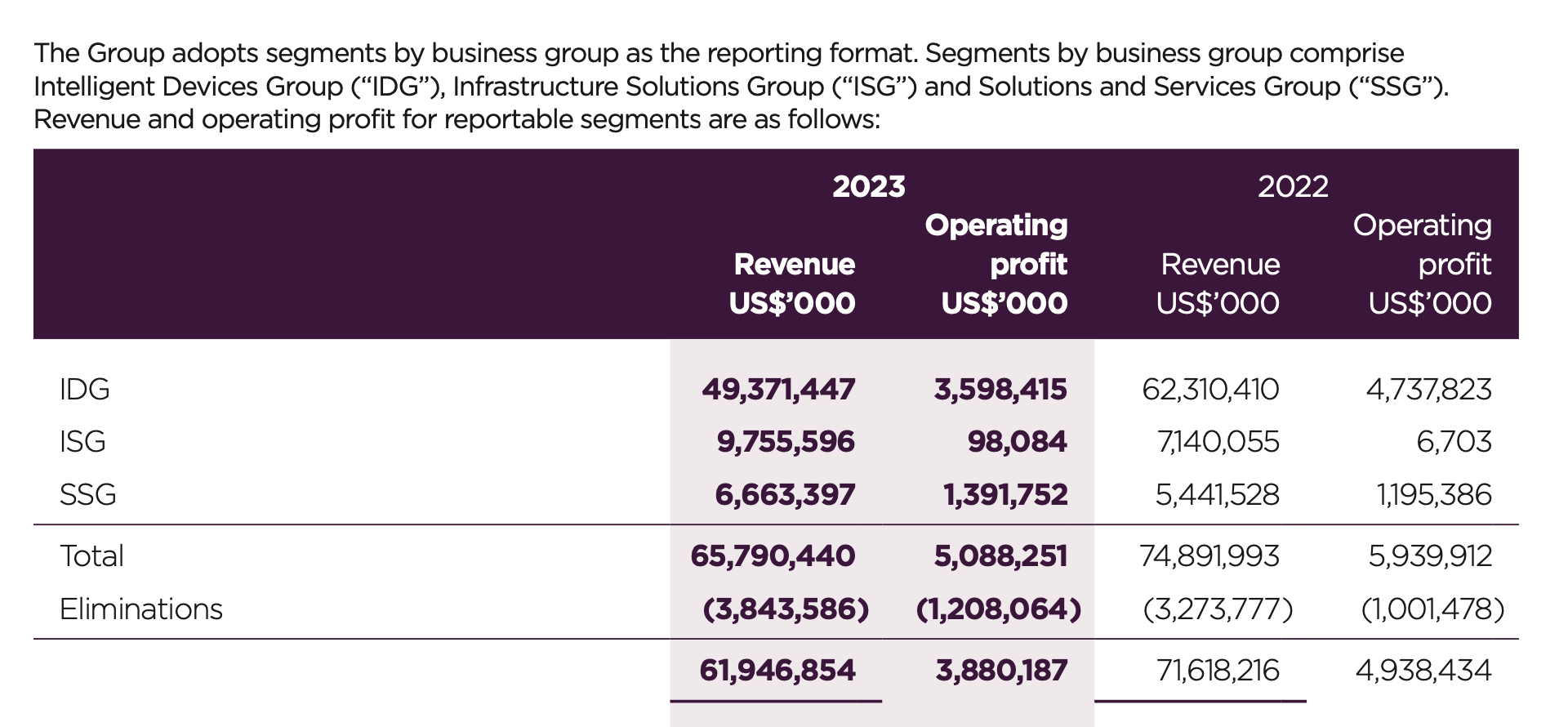

To bring us up to speed, the company’s 3 operating segments are Intelligent Devices Group (IDG), Infrastructure Solutions Group (ISG) and Solutions and Services Group (SSG).

While IDG, the group that sells devices that we are familiar with, has struggled in the last year, the other two groups are producing healthy numbers, both on revenue and profitability front:

Devices business is expected to get better as the macro-environment gets better:

We believe the PC shipment has nearly bottomed by now, based on the activation number which reflects the real demand, as well as the channel inventory level, which has almost returned to the pre-pandemic level. From this point, the PC market is about to resume its year-on-year growth, as early as the second half of 2023.

Based on the updated numbers, the relative score has declined marginally into negative territory. So the stock is now listed as a “Dilute”, but the effect is so marginal, that it is likely to bounce back into better status soon enough2. At the time of drafting this post, it is a net positive position in my portfolio and I suspect this stock will continue to be a solid allocation within my portfolio.

Alibaba Group (HKG:9988) ❤️

Alibaba Group announced their results in late-May as well and their numbers are much better than Lenovo’s. Using USD numbers (RMB numbers are much better due to favourable currency effects), sales declined by 6%, while operating profit after tax (OPAT) improved by 28%, with earnings per share (EPS) growing by 11% and Free Cash Flow improving by 33%. Overall this has been a good year.

Some highlights from their report:

Customer management [33% of group revenue] revenue decreased by 8% year-over-year, primarily due to mid-single-digit decline of online physical goods GMV generated on Taobao and Tmall, excluding unpaid orders year-over-year, which was mainly due to soft consumption demand and ongoing competition as well as supply chain and logistics disruptions due to COVID-19.

Direct sales and others revenue under China commerce retail business [32% of group revenue] in fiscal year 2023 was RMB274,954 million (US$40,037 million), an increase of 6% compared to RMB259,830 million in fiscal year 2022, primarily due to the revenue growth contributed by our Freshippo and Alibaba Health’s direct sales businesses.

Revenue from our Cloud segment [9% of group revenue], after inter-segment elimination, was RMB77,203 million (US$11,242 million) in fiscal year 2023, an increase of 4% year-over-year compared to RMB74,568 million in fiscal year 2022. Year-over-year revenue growth of our Cloud segment reflected the revenue growth from non-Internet industries driven by solid growth of revenue from financial services, automobile and retail industries, which was partially offset by the decline in revenue from customers in the Internet industry mainly driven by declining revenue from a top customer in the Internet industry phasing out using our overseas cloud services for its international business due to non-product related reasons.

Revenue from our International commerce retail business [6% of group revenue] in fiscal year 2023 was RMB49,873 million (US$7,262 million), an increase of 17% compared to RMB42,668 million in fiscal year 2022. The increase was mainly attributable to the growth in revenue generated by Trendyol and Lazada. The increase in revenue from Trendyol resulted from more efficient use of subsidies and robust year- over-year order growth.

This is a business that is doing generally well. The big update with this business is the spin-off into 6 businesses - well beyond the scope of this post. I might come back to this topic in future. Overall metrics are sound. The business continues to have a solid Relative Score and retains its “Accumulate” status. I am happy with what I see, despite a drawdown on this position at the time of writing this post.

PetMeds Express (NASDAQ:PETS) 😥😥😥

PetMeds FY 2022-23 was largely a forgettable one. Both reorder (-4.9%) and new sales (-16.2%) were down, net sales down 6.1%. Net Income dropped 99% from USD 21M to a mere USD 233K. Their presentation and their 10-K were very light on details, and I haven’t had a lot of time to research the ailments on this company. It is perhaps sufficient to say there aren’t too many good things going for it, at least in the immediate term. It is still throwing off reasonable cash with FCF/share at USD 1.1 as against USD 0.82 last year. Management is still committed to dividends at USD 1.2 per share, which I think is clearly unsustainable unless the business rerates to the positive in a big way.

The stock, like Lenovo, has technically moved into “Dilute” section, but unless Lenovo, the business seems to be much worse off in the past 12 years. Let’s wait and see. I don’t plan to add to my position for the time being.

Summary

Not a great set of results, but it is what it is. Thankfully, the combined position across the 3 stocks mentioned above is still a net positive for me. Yes you read that right!

Markets are forward looking and across these stocks, the market has a positive outlook on them, which is promising. That is obviously aligned with my own long term thinking on the stocks in my portfolio.

I will look forward to reporting better news later in the year. In the meanwhile, happy investing!

(Disclaimer: Nothing written here is a solicitation to buy the stocks mentioned. I hold position in all the stocks mentioned in this post)

FCF per share is typically noisier than other metrics. So the 44% drop should be taken with a pinch of salt. I don’t believe the business has degraded 44% in the last year, for instance.

As Relative Value is a function of price, inversely coordinated, that if the price were to drop by 1-2% which is a very normal market activity, then relative value increases. In this case, I expect the stock to vacillate between “Maintain” and “Dilute” as the stock bobs up and down.