Summary Analysis: Iress (ASX:IRE)

Tough turnaround ahead

I wrote about Iress as an earnings update in August of 2023. I left that note saying “At some other point of time, I hope to do a deeper dive on the travails of this business”, so here I am with some extra thoughts. As a quick recap, it is a dog in my portfolio, with a current IRR of -16%1.

completes share buyback; shares up | Kalkine Media")

Iress Limited (ASX: IRE) is an Australian-based software company that provides technology solutions for financial markets and wealth management. Iress develops and offers a range of software products and services tailored to the needs of financial professionals, including trading and market data systems, financial planning tools, and wealth management software.

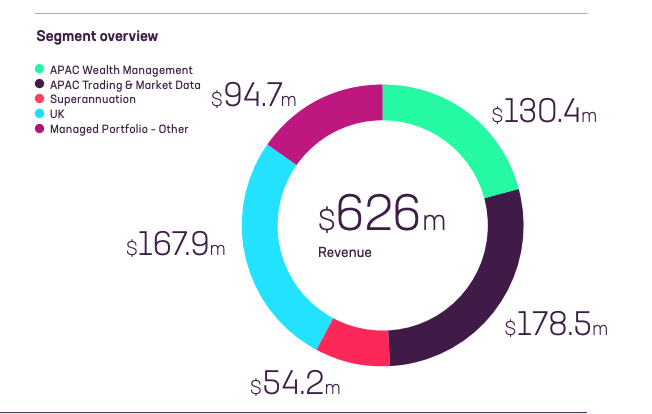

Founded in 1993, and publicly listed on the ASX in 2000, it today has a market cap of about AUD 1.49 Bn, and is a constituent of the ASX:200, the leading index in Australia. It operates in 5 different segment, all carrying material revenue weights.

For a period, this company looked like a good buy. Since 2010, the company has been gradually growing its revenue from AUD 179 Mn in 2010 to some AUD 625 Mn in 20232, which is a annualised growth rate of 9.76%. As with any company with growing revenues, it is clear that there are customers out there who like what Iress produce and are willing to pay good money for it. Moreover, Iress’ typical customers are financial houses and there is some stickiness to the revenue.

In the 11 years from 2010 to 2022 (both years inclusive), Iress has been steadily generating both profits ($4.31 per share) and Free Cash Flow ($6.28 per share) and returning cash to shareholders ($5.54 per share).

Along these years, you could buy this share for anything between 11x - 17x FCF. When I was adding this stock to the Coffee Can Portfolio, I don’t think I was totally out of line, though I have to admit that there were risk factors that I have identified retrospectively, that should have probably given me reason for pause.

2023

Let’s first consider the 2023 results3 before we look at the red flags.

The company declared a statutory loss of AUD 132 Mn in 2023. The latest loss, though, must be taken in context. The company has written down some goodwill.

(I am not trained in Accounting Philosophy, but goodwill seems like boondoggle to me. Or as ChatGPT told me - “Goodwill in accounting is like a unicorn in your financial statements – it sounds magical, everyone talks about it, but good luck finding any concrete evidence it actually exists!”)

From their latest annual report:

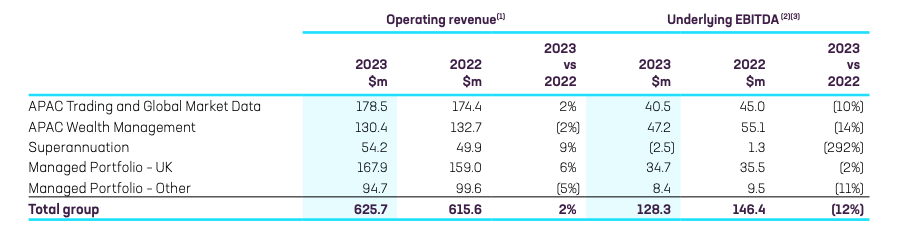

Underlying EBITDA, Iress’ current headline measure of performance, came in at the top end of the revised guidance set out at the half year but was 12% down on FY22 at $128.3m. This was primarily a cost story where inflationary pressures were a key factor in higher salaries and third-party input costs. In response, Iress undertook significant restructuring initiatives, to trim its cost base.

Iress reported a statutory net loss after tax of $137.5m, in large part due to non-cash impairments and accelerated amortisation of intangible assets which included the $130.2m write down on the carrying value of UK goodwill. Non-operating and significant items also increased to $57.8m, largely related to transformation activities.

If I understand correctly, they are saying we are marking down some book value (earlier ascribed to accounting balderdash) to its true value now at the cost of an impairment, and doing a bunch of restructuring that’s costing us AUD 58 Mn in real money. I am cautiously willing to give the management a bit of credit on these two, but only just. If we back those things out, Iress would have generated a profit of AUD 62 Mn4 in OPAT. We will come back to this number in a bit, so just hold on it for the time being.

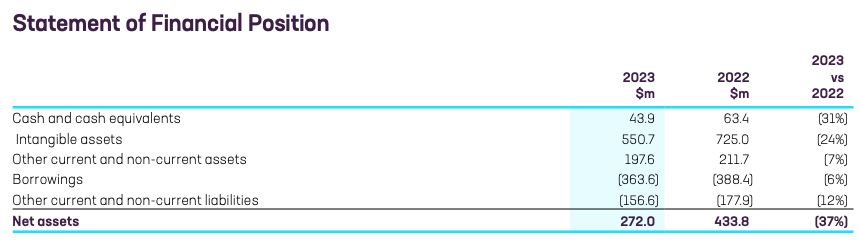

Balance sheet is looking worse than it did a year ago.

2023 wasn’t bad in just segment, but growth has stalled to near-0 across the board - look at comparative revenues and look at the EBITDA numbers in the rightmost column - it is a sea of red!

Management change

Long term CEO Andrew Walsh left in July 2022 and has been replaced by Marcus Price. I have no evidence of this, but I feel that Walsh’s departure may not have been entirely voluntary and likely taken by the Board as the performance of the company was already in decline and visible to them.

Marcus price seems to have the right ideas, as can be gleaned from this article, it seems he is focussing on:

Breaking the business into 2 buckets: “Core” and “managed for value”

Core will contain Wealth Management, Trading and Markets, and SuperAnnuation, which combined generated AUD 363 Mn in revenue and AUD 90.2 Mn in EBITDA in 2023, or EBITDA margin of 25%.

The “managed for value” business generated AUD 262 Mn in revenue, generating AUD 45 Mn in EBIDTA in 2023, or margin of 17%.

Get the core businesses to follow rule of 40 (revenue growth + profit margin >= 40).

The general idea is to reinvest in the Core business, which is presumably more valuable and long term value generating, while the second basket will either be used purely for cash flow, or divested away if possible.

This is all great talk, but I am not entirely convinced, as the core baskets also do not seem to be growing presently, and some of their segments are going backwards in profitability measures. Getting any segment of your business to follow rule of 40 is incredibly hard as evidenced in the plethora of companies that aspire to, but fail to do so.

"Turning a company around is like trying to U-turn an aircraft carrier – it takes time, a lot of maneuvering, and there's always the risk of hitting an iceberg. Just hope the iceberg is made of profits!"

Missed Red Flags

Let’s come back to the red flags I talked about in a previous section.

When I bought the stock, I got enamoured by the headline numbers - revenue growth, FCF generation, dividend payouts etc, which are all signs of a good business. However, there were a few things I missed out:

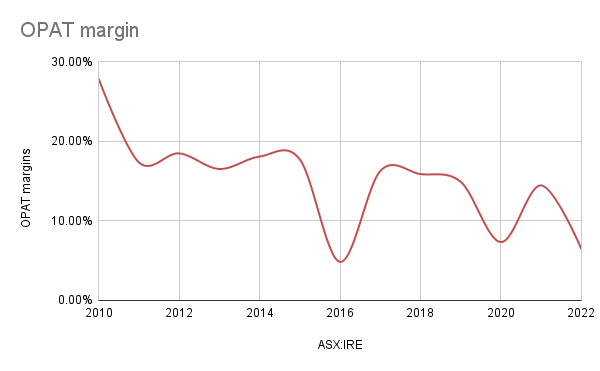

Profit Margin: OPAT margins for this company has been all over the place. In 2010 it was as high as 27.92%, which immediately dropped to the range of 16.5%-18.5% for the nest 5 years, but since then it has been on a secular decline. In fact profit margin in 2023, even after adjusting for one-off expenses, is just under 10%.

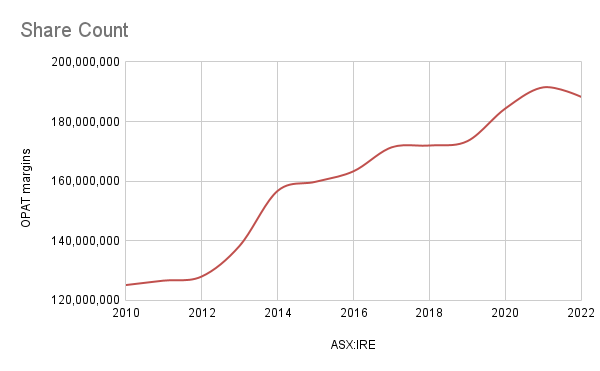

Growth in Stock Count: The outstanding share count of the company has been on a steady upward trajectory, going from 125 Mn in 2010 to 191 Mn in 2021, where it peaked and has since slightly declined back to to 185 Mn. From what I see, all of this can be attributed to stocks issued to employees. This is a very similar pattern to what has been happening at Meta, except that the quality of the business and its ability to generate cash is far more inferior than at Meta.

The Takeover Attempt

In 2021, Swedish PE form EQT attempted to take this company private for a price of $15.91 per share, which eventually fell through. This was around the time the company was generating about AUD 0.50 per share in FCF, which means that EQT was willing to pay about 32x FCF, which would have been a fantastic exit for this business, but that ship has obviously sailed.

Summary

To summarise, Iress is a software company in the financial market space, producing software that has good adoption, and a growing revenue, but the company has failed to produce a steady profit margin, is going through a restructuring under a new CEO, while it is forced to cut dividends, and conserve precious cash on its book.

Turnarounds are generally hard, and tough to pull off. However this company also has a strong DNA and culture of producing good results for a long period of time (2010-2022). The way I see it is that if Marcus Price & team were to succeed, then I can definitely see a thriving company with a strong core business that is both growing and producing good prints. As long term investors, in what are generally high quality companies, we have to (a) live with temporary blips in the journey and (b) worst case, live with some being failures, but we have to let the story unfold to see. The best coffee can outcomes are surprises to the upside.

I am carrying this stock at $9.2 per share (net of dividends received). In true Coffee Can Investing style, I don’t plan to sell any, but I also don’t see how I am going to expand on my holdings. Thankfully it is just about 0.9% of my holdings and I am happy to just let my holdings be till I see an improvement in the business.

As always, Happy Investing!

In GBP terms. In AUD terms, it is -11% IRR.

This company, like all other Aussie companies declare their annual results on a July to June basis, so 2023 must be read as “end of June 2023”.

This company, like all other Aussie companies declare their annual results on a July to June basis, so 2023 must be read as “end of June 2023”.

If indeed we were to take this at face value, and we mustn’t, this 62M will also attract an incremental corporate tax, and hence this should be revised down to something like $58Mn or so.