Some thoughts on Meta

Great results, spectacular stock pop, and yet SBC angle is worrying

Meta recently reported its results and a trillion dollar company, with thousands of well-heeled investors and analysts always looking at the stock and the estimates and such, popped by a 20% upon results!

Interestingly, the company only produced a profit of $39.1Bn for 2023, which is lower than the $39.37 from 2021, so the results are not even an all time high for this company, and yet the stock is now about 25% higher than its previous round of all time high, established in Aug 2021, of $380. Against the backdrop of a 5% risk free return todays (vs 1% then), that’s an astonishing story of the stock both on the way down and on the way up - Good for Meta shareholders!

I have a small amount of shares, bought outside of my Coffee Can Portfolio, purchased at an average price of $150ish, which have trebled in less than 2 years. Happy me!! The question then comes - what to do with these shares? Hold them, sell them, buy more?

Valuation

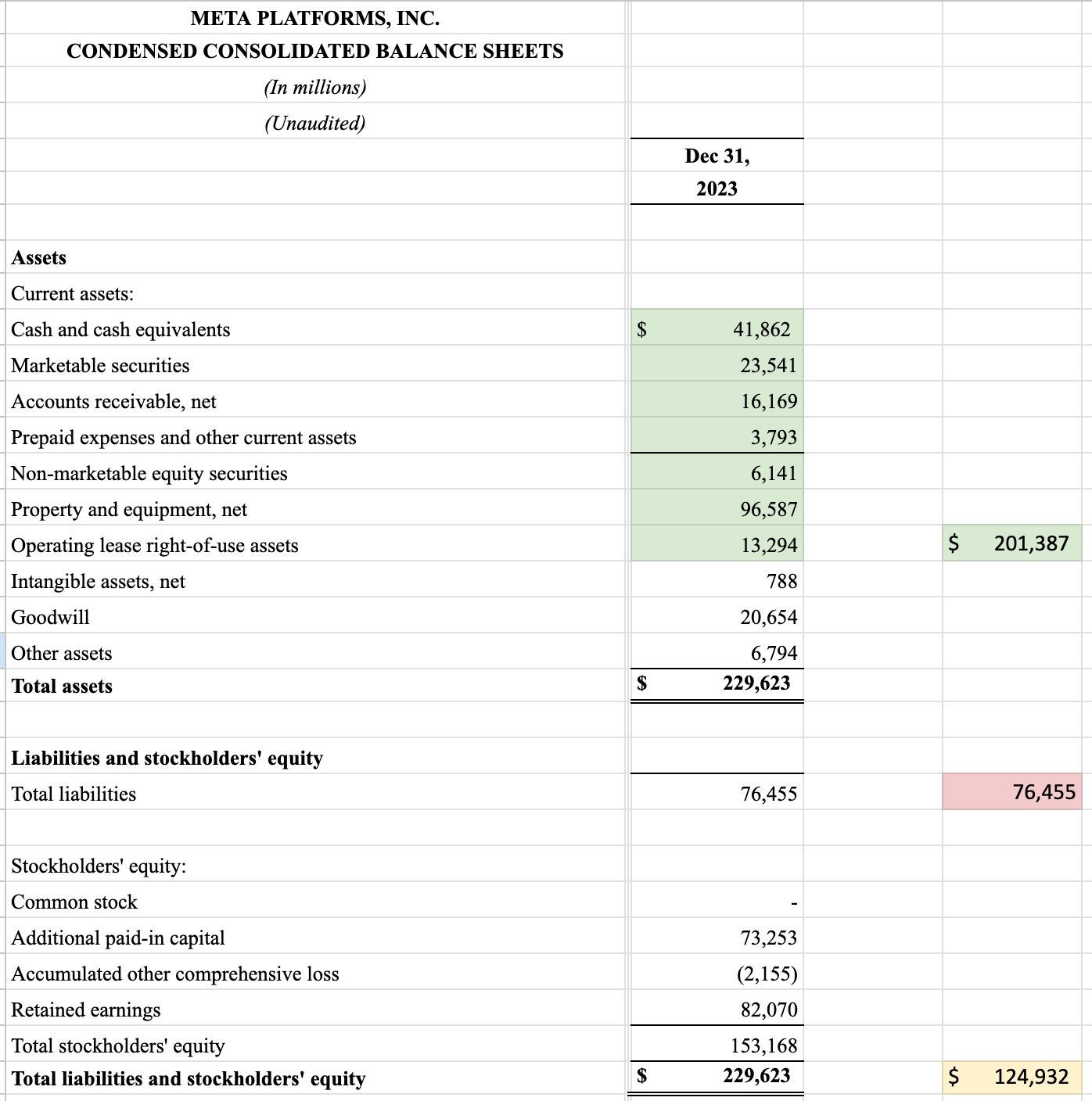

Prima facie, the stock trades at about 31x earnings. A quick look at the balance sheet tells me that net of liabilities and intangible assets & goodwill, the company has assets of ~$125Bn. While not all of it should be considered as cash in the bank, let’s accord the company full value of this amount. That alone is about $47.50 per share. Net of this, the company’s price today is 28.6x earnings.

Cut it either way, the stock is expensive - the market expects the company to keep growing its profits in the future. It is not a screaming buy for me, so adding to the position is ruled out. I wished I had a bigger position (> 100 shares), then I could probably reduce my exposure by selling a Call option contract. So, really it is either hold or sell for me.

The SBC angle

(prescript: I have written about Stock Based Compensation, SBC, previously on this blog. It might be worth a quick read before reading this section.)

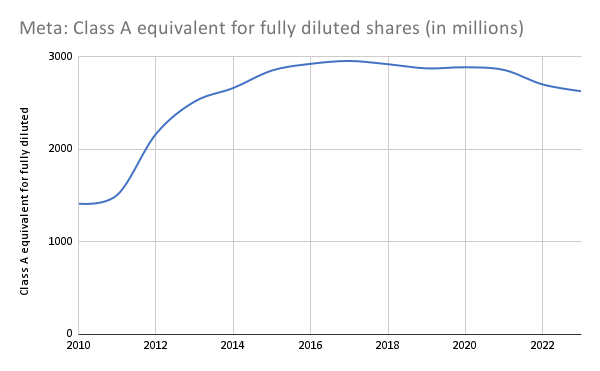

Meta went public in 2012. On Dec 31, 2012, there were 2,166Mn shares of then Facebook shares outstanding, and $11,755Mn (or $11.75Bn) in book value, equalling $5.42 in book value per share.

On Dec 31, 2023, exactly 11 years later, the company had 2,629Mn shares outstanding. This is some 21.3% dilution of stocks in the intervening period. This seems bad at face value, but there is more to it.

: https://t.co/foAQggS1cn\" / X")

Of the 473Mn shares of net dilution in the 11 yr period, some 213Mn shares went to acquisitions, 201Mn of which went to fund the WhatsApp acquisition in 2014. Instagram was acquired in 2012 - the dilution happened before the time period we are considering (2013-01-01 - 2023-12-31).

The remaining 262Mn net shares of dilution all went to employee stock based compensation. In fact the actual dilution was more than that - some 637Mn, but some of the dilution was withheld due to tax accrued, and some of it was bought back through repurchases.

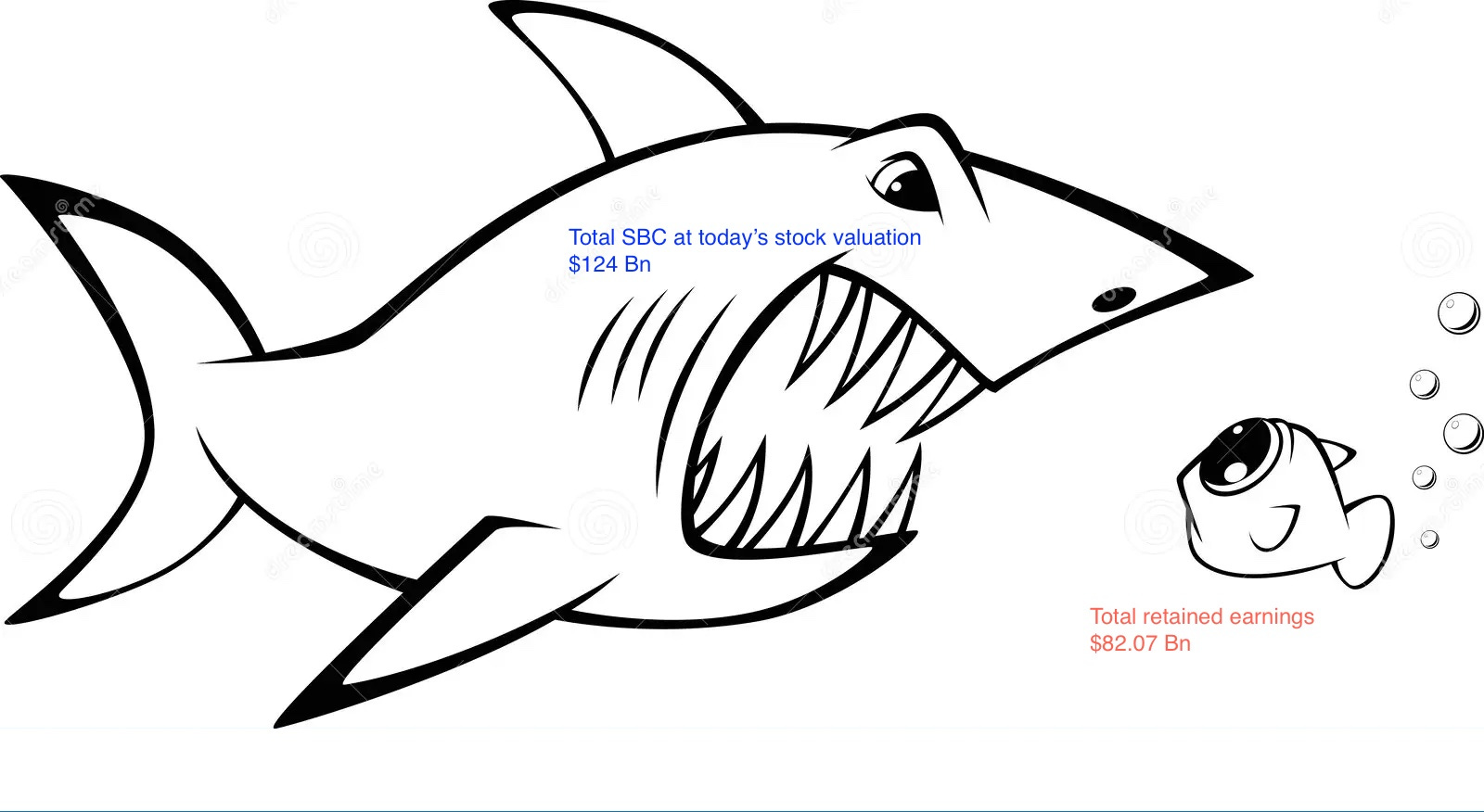

This 262Mn net dilution at today's stock price of $475 is roughly $124Bn in value. This is greater than the retained earnings of company on Dec 31, 2023, some $ 82.07Bn. Put another way, if the company had to dial back its dilution to where it was in 2012, it just can't. It has given out more in stocks than it has retained as earnings in its lifetime of operations, both as private and as a public listed company!

But hasn't the allocation of stocks to all these employees been a net-addition to non-employee shareholders? i.e. without these employees, we wouldn't be here, right? Yes, that’s for sure, but non-employee shareholders pay a huge price. For instance if employees are so core to the production of profits, then there are other structures like partnership which might be better suited than being a public listed company, but I digress.

Book value of the company has grown from $5.4 per share to $58.3 per share in the same 11 year period, or about $48.9 per share. In the same time period, the company in fact earned a total of $73.2 in diluted EPS.

So, the non-employee shareholders are only getting 66%1 of the value generated by the company. The rest 34% have been wholly consumed by dilution. Given that the WhatsApp acquisition is considered value accretive for the company, the 34% leakage is purely to SBC.

But that's not the whole story! The $73.2 in diluted EPS is already subdued due to the fact that the denominator has been expanded to include the dilutions. If we were to back that out, we observe something more interesting.

If we backed out SBC, buybacks, but leave acquisitions related dilutions, current stock count will be closer to 2,379m shares, EPS over the 10 years would be $80.9. So, in fact, the net book value addition of $48.9 is a mere 60% of the total value generated by the company.

So, 40% of the company's value addition has gone towards stock dilutions. This is on top of every staff related costs that we have already accrued in the P&L over the years. Value generation for non-employee shareholders has been rather dismal.

The leakage of investor value doesn't cease here. Between 2020-2022, average stock dilution was 45m shares, but in 2023, it has shot up to 65m shares. It is possible that the company had to dole out a lot more shares in 2022-2023 to account for the fact that the share price was low and all refreshers and new offers (which were admittedly quite few) had to be inflated to account for lower price.

Put another way, in 2023 alone, the company produced $39.1Bn of profits, but the stock dilution of 65Mn shares at current price alone is $30.9Bn. So, in essence, the company would have made a lot lot less if the company had to pay cash in lieu of its stock based compensation.

Philosophy

While it seems I make what seems to be a radical suggestion that Meta is somehow a poorly run company, reality is far from it. I think Facebook is an excellently well run company2. It has learnt how to use SBC and other compensation perks to engage high levels of employee engagement and retention, both of which goes towards building strong products. Being an engineering leader myself at another tech company, that is currently private and hence with no option of stock based compensation for its own employees, I am well aware of the positive effect SBC can have at building a well functioning tech company.

Put another way, at a company like Meta, engineers are the equivalent of the capital expenditures at other companies. If you think of a traditional manufacturing company, they have to build factories and warehouses and such, and then maintain them each year. In a company like Meta, engineers are necessary component of maintaining the intellectual assets that form the basis of the cash generation engine.

My grudge isn’t so much against the SBC itself. It is with the way these things are accounted for in the current accounting system. I get the argument that the company needs all these well compensated engineers to produce these profits, but using SBC makes it very difficult to understand the true value generated by the company for outside shareholders. Once you peel back the layers of the onion, you realise it is not as rosy as the prima facie numbers suggest.

Summary

For all the wonderful cash generating abilities of Meta Inc, 40% of the value accrued has been given away to employees and only 60% to external shareholders. While it doesn’t faze the average investors, it is best for retail investors like us to be factoring this when we decide to buy/hold/sell the shares.

On my end, I am torn between my “buy and not sell”, i.e. Coffee Can Style of investing, and what I see as a company that operates starkly in contrast with what I like in the companies I hold, i.e. accretive value for shareholders, which makes me want to sell. While I ponder that, happy investing to you all!

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility for your actions. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

Used to be 70% at the end of 2022. Now it is 66%. The value generated for outside investors has *gone down* in the last one year.

If that wasn’t the case I wouldn’t have ventured into the stock, even if it was relatively good value when I did.