More updates from Down Under (ASX:IRE & ASX:DMP)

Both results are down & under

Survey on next stage of the substack

Thank you for the love and support you have show to the Coffee Can Investor substack. It has been many months of regular writing for me and I have loved every minute of it so far & I hope I have not wasted too much of your time in doing so. Now seems like a good time to gauge from current readers on what you like reading today on the website. I am also trying to assess if newer streams of content (like a podcast or more coffee can portfolios) might be of interest. Please take 2 minutes of your time to respond to a survey please.

It was a gut wrenching week to follow updates from down under. Two of the Coffee Can Portfolio stocks announced results, and both disappointed in different ways. Time to take a quick look.

Iress (ASX:IRE) 😥 😥 😥

First up was Iress, which announced their mid-term results last week. Normally I don’t follow mid-year results and I would safely ignored it, had it not been my brokerage account showing an absolute dropping off the cliff of this stock, which forced me to take a peek.

The cratering of the stock largely comes from what has been a very disappointing update where the business announced flattish revenue growth, a 55% drop in EBIT, and a massive 557% drop in OPAT. You read that right! The business went from producing A$24M as OPAT in first half of 2022 to now producing a *loss* of A$140M. The management has decided to suspend its dividend, which shouldn’t come as a shock, given the otherwise horrible results.

At some other point of time, I hope to do a deeper dive on the travails of this business, but suffice to say, I don’t expect this stock to recover any time soon and I don’t expect to make good my money either. It is now my second worst performing stock. I don’t have anything redeeming to say at the moment, and needless to add, I will not be adding to my position until I see something positive in the business. Never throw good money after bad!

Domino’s Australia (ASX:DMP) 😥

I wrote about Dominos’ woes in an earlier post. At that time, I had pencilled in some expectations for the full year results based on their first half report, which wasn’t rosy in the first place, with proportional expectations of the second half. This week they announced their full year results. The results are a mixed bag.

Revenue came in at A$2.35Bn, which was slightly better than last year, but all the other metrics, specifically profitability is way down, coming in at A$0.76 per share, which is at the same level as profits in 2015. A 8-year reversal in a compounding story is never ideal. Dividend for the full year to drop to $1.1, and marks the second consecutive annual drop.

Glancing through the annual report, their woes are basically split across a couple of dimensions - pricing and growth.

Pricing

Suppliers have invoked force majeure and increased ingredients costs, despite long term contracts. In turn, Domino’s attempted raising prices, but users have pushed back by decreasing volumes purchased. In effect, the business is trying to find the sweet spot to counter both transitory and structural inflations faced in the QSR business.

Growth

Long term growth is largely affected by the fact that current franchisees, who are often the de-facto growth engines for this company, are reeling under decrease in profitability (related to pricing above), and are unwilling to invest in newer stores. This means that the long term store growth guidance of 8-10% is not feasible. This year, the business did 6.1% store growth1, and it seems expecting 6-7% growth is far more realistic than 8-10%.

I expect the company to eventually get pricing right, and margins will no doubt improve, hopefully making last year’s $0.76 EPS an anomaly. It is not unreasonable to expect profits to snap back to a more digestible $1.7-$2 per share range in the next 2-3 years, which is where the business was ~12 months back. Growth, however, is a tougher story to predict and harder still to be optimistic about.

Market’s take

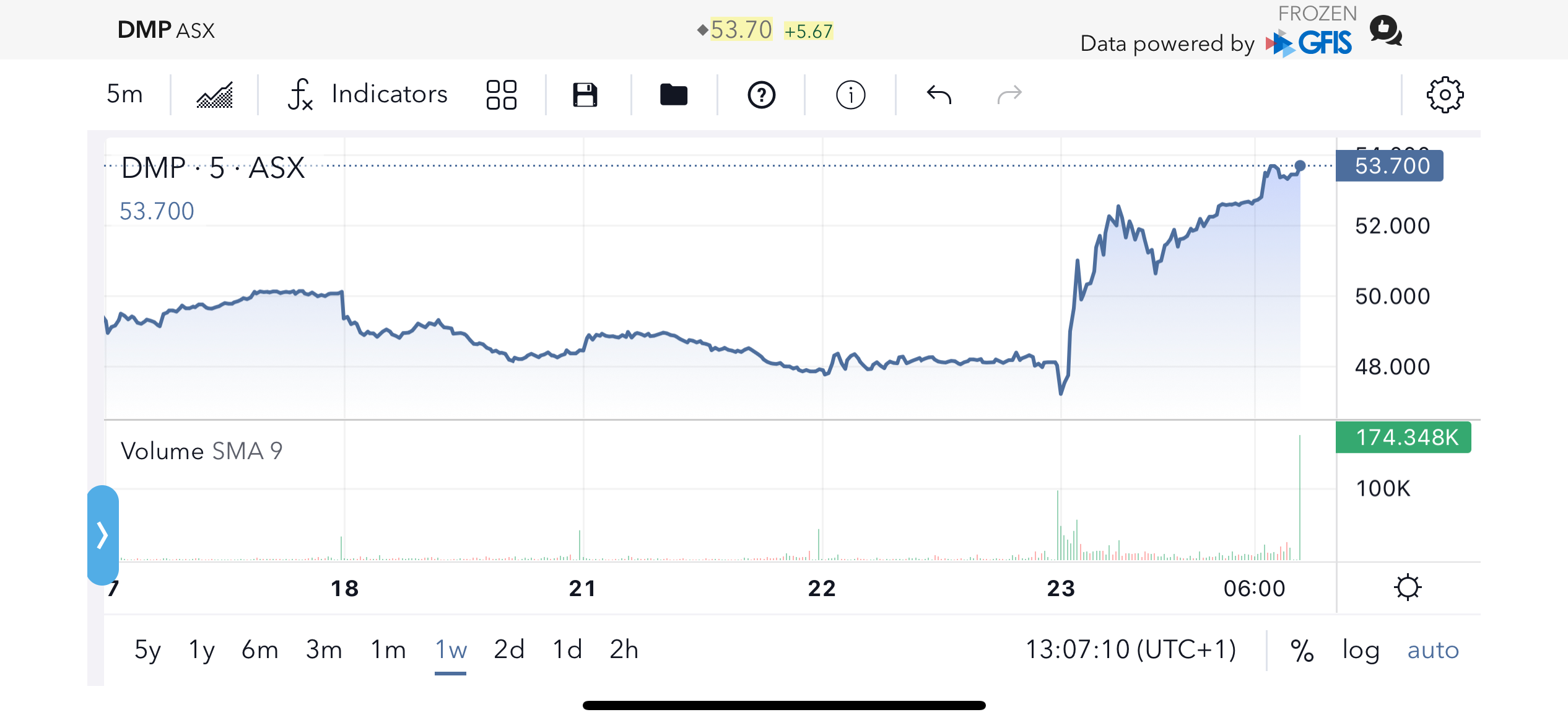

Given the results were underwhelming for me even after I had factored in pessimistic outlook after half term results, I would have expected the stock to go southwards. I was dead wrong! The stock snapped back right up, climbing some 10% in response to this ticker update. Clearly, market attributes a lot more optimism than I do. Let’s hope the market is right in this case.

The stock continues to be super-costly by most metrics and I don’t see any reason to materially add to my position. I will continue to add to my position is very small measures here and there, but that’s about it. I expect the proportion of holdings to dilute over time. I can review matters as the company provides updates, hopefully all for the better.

Not great news from down under, but that’s part of parcel of being an investor. Onwards and Upwards! Happy Investing!

While the business exited Danish market as promised, they have acquired Domino’s operations in Malaysia, Singapore and Cambodia, which adds 287 stores with immediate effect.