Summary Analysis: Stella-Jones

Disciplined execution of a mundane business

Stella-Jones (TSE:SJ) is presently the best performing stock in my Coffee Can Portfolio. I recently wrote about one of the worst performing ones, so time to talk about rosier enterprises.

Founded in 1992 by Brian McManus, Stella-Jones Inc. is a Canadian company that specializes in the production and marketing of pressure-treated wood products, which is wood that has been treated to resist decay, insects, and other environmental factors. The company's core products include railway ties, utility poles, and residential lumber. Stella-Jones operates solely in Canada and the United States.

While it is a leader in this particular space, it is still a relatively small company, crossing C$3Bn in revenues for the first time in 2022. However, where it excels is in operating this niche space very well. The company has a strong balance sheet, allocates capital well, and does the myriad other things about running a business well enough to earn my respect.

About the Business

There are 4 major business segments:

Utility Poles (~40% of 2022 book, 5 year CAGR of 10.6%)

Stella-Jones supplies major electrical utilities and telecommunication companies with wood utility poles across North America. The Company’s customer base typically prefers treated wood poles because of their durability, cost effectiveness and the safety it offers their line workers during maintenance work. Treated wood poles have the potential to last 40 to 50 years, or longer, and have a relatively low cost of purchase, installation and maintenance.1

Railway Ties (~25% of 2022 book, 5 year CAGR of <1%)

Stella-Jones supplies North America’s Class 1, short line and commercial railroad operators with railway ties and timbers. Demand for railway ties is comprised primarily of upgrade and maintenance requirements, with occasional activity in new track development. Stella-Jones has the capacity to supply over 10 million pressure-treated wooden crossties to its customers each year, helping keep North America’s railway infrastructure on track.2

Residential Lumber (~25% of 2022 book, 5 year CAGR of 9.4%)

Stella-Jones manufactures and distributes premium quality lumber and accessories to Canadian and American retailers for outdoor applications. This primarily consists of pressure treated consumer lumber for use in patios, decks, fences and other outdoor applications, as well as the distribution of wood and wood-alternative accessories.3

Other revenue (Industrial Products; Logs and Lumber) (~10% of 2022 book, 5 yr CAGR of 5.28%)

Stella-Jones provides pressure-treated wood products to the industrial, marine and civic sectors for outdoor applications, including railway bridges and crossings, marine and foundation pilings, and construction timbers, offered in a variety of select wood species and preservatives. Stella-Jones also manufactures the wood preservative, creosote, for use in its wood treating activities, as well as other coal tar-based products such as roof pitch and road tar, which are sold to third party customers.

The logs & lumber product category is used to optimize procurement. It comprises the sale of logs harvested in the course of the Company’s procurement process, which are determined to be unsuitable for use as utility poles. Additionally, while procuring sufficient competitively priced residential lumber volume, Stella-Jones engages in reselling excess lumber into local home-building markets. It does not generate any significant margin and is fairly tied to the price of lumber.4

Putting it together

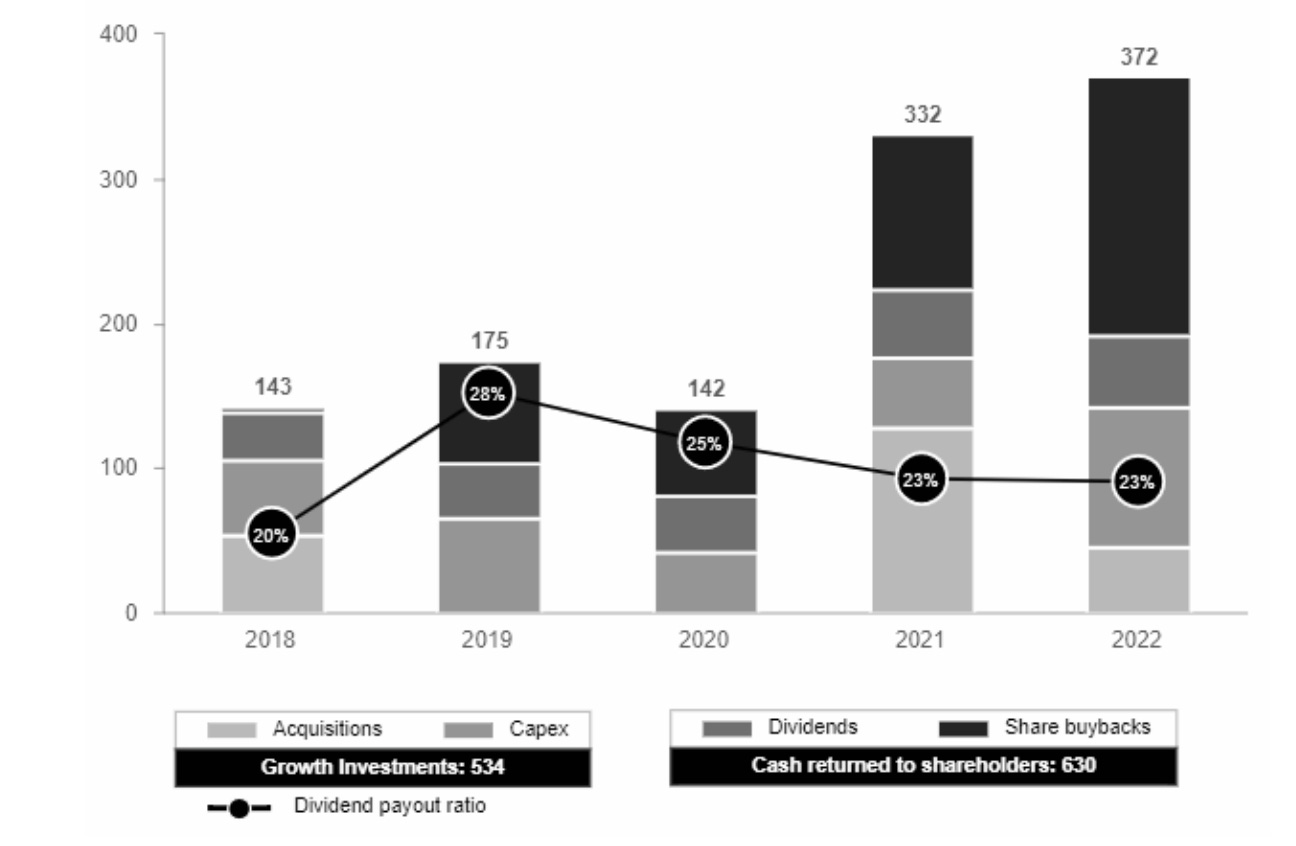

In effect, this is a rather mundane business in a niche field. Parts of the business have good revenue growth potential while others don’t. Put together however, the company deftly adds to its revenue capacity through acquisitions, as well as expanding capex investments on a consistent basis.

From their report:

Stella-Jones actively pursues infrastructure-related and other strategic opportunities that leverage its extensive network, customer base and fibre sourcing, while also contributing to its ability to generate a consistent cash flow. The Company has an established track record of successfully executing a strategy of consolidation in the pressure-treated wood products industry, having completed more than 20 acquisitions since 2003.

In the future, there will be decent growth through maintenance of railway ties, expansion of the electric network in North America as well as broadband and digital network growth, all of which consume Stella-Jones products.

The company has a disciplined track record of capital management exhausting all the avenues of prudent allocation, i.e. investments in internal business, acquisitions, dividends *and* buybacks.

Stella-Jones has an enviable track record of increasing dividends since 2004, up from C2¢ 2 decades ago to C80¢ today, compounding at ~18% per year over this period.

When management have engaged in buybacks, it has done so at average prices of $44.14 and $38.58 in 2021 and 2022 respectively, well below the $50-$70 range the stock has traded this year, which means continuing shareholders are benefitting from the buyback, which is a huge positive! It has retired some 7.5M shares in these two years, which accounts for ~12% of the 66M outstanding shares at the end of 2020.

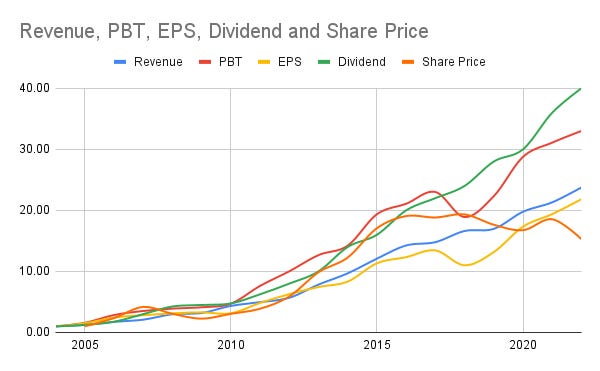

In terms of metrics, every part of this business has looked to move to the up and to the right in the past 20 years.

This is a business that converts the profits into FCF at a pretty healthy rate consistently. Given that the management is very good at converting these cashflows into something useful for us shareholders (through the accretive buybacks and consistent dividend policy), the cashflow is being put to good use.

Competition

A casual glance at some of the competitors, i.e. Canfor, Interfor and West Fraser Timber, tells me that none boasts of as good a consistent business performance as Stella-Jones does, and while the latter 2 are distinctively cheaper than Stella-Jones, I am happy with the choice I have made. Price is what you pay, and value is what you get.

Outperformance

While this has been a staid, but a solid business disciplined at compounding business outcomes, the relative outperformance of this stock in my portfolio in the past 2-3 years has largely been a stroke of luck. The stock entered an average price of $40s way back in 2015 and bobbled between $40 and $50 for a good 7 years before breaking out in the past year or so. Investors who got in in early 2015 were perhaps just holding on to the stock for the dividend yield and some puny capital gains.

Given that the management has pursued stock buybacks aggressively, providing an additional buyer for the stock, the recent inflection of the stock from $40s into the $60s is wholly justified. Even at these levels, the stock is only at a 16x p/e multiple, and a 10x p/fcf multiple. So as an investor, I am happy to accumulate stock even with the recent run-up.

Companies that are well run and growing in industries like this have been targets of conglomerates & PE takeovers in the recent years, specially when interest rates were low and investors searched for yield-generation type of investments. This is a C$3Bn market-cap company, and hence not likely to be in the radar of big guns like Brookefield or Berkshire, but it may be targeted by PE looking for bolt on acquisitions. All we can hope for in that scenario is to be taken out at a healthy premium to where it trades today,

Risk

In terms of core business risk, I am less worried. In terms of stock risk, the obvious one is that if the company ceases to do buybacks, then it is possible that this is a quickly forgotten stock and will likely sink back to low $50s. While management has made it explicit that they are going to continue to engage in buybacks, this is a distinct risk we carry as investors. If the core business continues to do well, I see no reason not to accumulate it in the long term, even if the stock rerates due to the lack of buybacks.

Final thoughts

Stella-Jones is a good business to be owning and while there has been some recent tailwinds that have allowed the stock to inflect, there is some suspicion on whether those factors are ephemeral or not. I will continue to accumulate the stock in lots as I have money to spare.

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

Content of this paragraph comes directly from latest annual report.

Content of this paragraph comes directly from latest annual report.

Content of this paragraph comes directly from latest annual report.

Content of the above 2 paragraphs come directly from latest annual report.