Summary Analysis: Domino's from Australia

A reasonable company in drawdown due to high expectations

One of the worst performing stocks in my portfolio is Domino’s Pizza Enterprises Ltd (ASX:DMP). I hold this stock at an averaged price of AUD 62.5, whereas it trades for ~AUD 45 at the time of writing. Even after factoring in the small amount of dividend I have got, it is still an IRR loss of 34% on AUD terms, and a loss of 41.7% on GBP terms, the currency I use for all other calculations on this substack. It is time to review this investment and what’s gone here and what to do about it.

Not to be confused with the US listed Domino’s Pizza Inc (NYSE:DPZ), the Domino’s I hold is the franchisor of the brand as well as the largest pizza chain in Australia and New Zealand and operates as a master franchisee for the Domino's Pizza brand in these regions, as well as in several other countries including Japan, Germany, France, Belgium, Netherlands, Denmark1, and Luxembourg. The company owns and operates a network of Domino's Pizza stores, and it also acts as a franchisor, granting franchise rights to independent business owners. The company we are interested in is listed in the Australian Stock Exchange as ASX:DMP.

Domino's Pizza Enterprises Limited (ASX:DMP) was founded in 19832. The company was established in Brisbane, Australia, by brothers Tom and James Monaghan. They initially purchased the rights to the Domino's Pizza brand for Australia and opened the first store in Hamilton, Queensland. Over the years, Domino's Pizza Enterprises expanded its operations and became the largest pizza chain in Australia and New Zealand, as well as a master franchisee for the Domino's Pizza brand in various other countries3.

The Glory Years

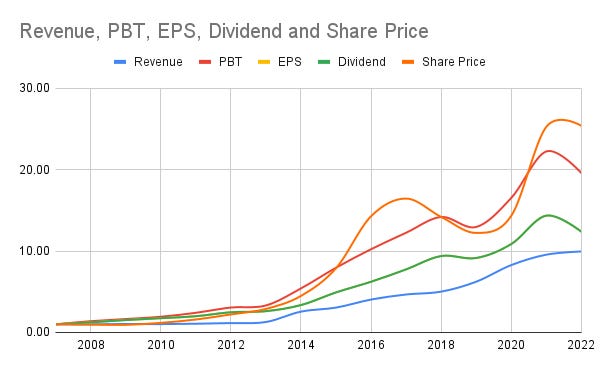

Between 2007 and 2022, the company was on an absolute tear, pulling along magical metrics. Everything you can imagine was compounding at a double digit percentage per annum.

Revenue 16.55% PBT 21.93% EPS 18.25% Dividend 18.25% Share Price 24.06% The company achieved this through a combination of (a) increasing store count by opening new owned and operated (O&O) stores, as well as franchising new outlets and (b) growing the sales of existing locations.

This is precisely when I was tempted to buy into this stock.

Headwinds

The last 12 months or so have been challenging for this business. In a half year update earlier in the year, the company announced that their first half metrics went backward. Not only has growth stalled, but revenue reversed by 4% and EPS by a whopping 21%! 😥

The reasons aren’t too complicated. In the same update, the company laid out the fundamentals of the reversal - as inflation has risen and price has been passed on, customer count and orders have declined and that has had widespread effects on the numbers. Dividend has also been cut. So the wheels have come off the growth engine in this company, over the past 12 months.

To be clear, this is not a bad company. It is still a perfectly good company, producing a product that market devours large slices of, well run organisation, with a healthy margin extraction, and a profitable bottom line, with toppings of cashflow to go on the side. So what went wrong?

What went wrong?

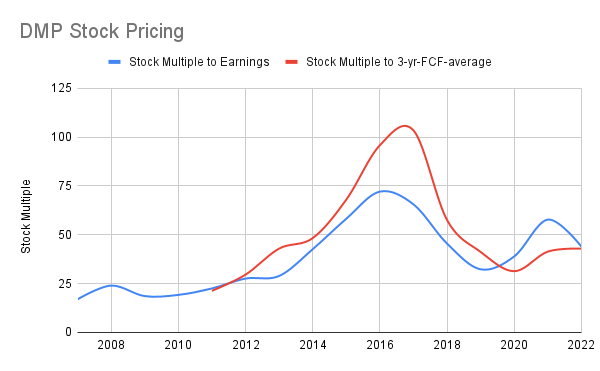

The market and investors, like me, got carried away with the growth of this company and assumed that this will go on forever. Share price grew at a much faster (24% p.a.) rate than EPS (18%) and by the end of the run, the stock was trading at price to earnings multiples that looks more like a growing tech stock than a consumer company that sells pizzas at the end of the day. At those multiples, there is no margin of safety.

People will surely continue to want to eat pizza, but they aren’t likely to consume it at an exponentially growing rate each year, especially in developed markets where Domino’s largely operates. In fact I would argue that even the stock’s current multiple, after the drawdown this year, is perhaps still too high and this stock should trade at no better than roughly 20-25x P/E or 20x P/FCF, or about AUD 35 per share, about ~20% lower than where it trades today, given that the bad news is out and about.

This is a general problem with stocks that are priced for great achievements. So long as the company continues on its growth path, the pricing and the shareholder returns look good. When moderation eventually follows, bag-holders are left wondering what went wrong. What goes wrong, however, is a repeated case of investors jumping in expecting perfection and the company turning out to be good enough, but not perfect.

Ups and downs are normal in business and in fact, this is not the first time I have written about turnaround situations (see my write up Fresenius and Challenger Financial), but this one is a tougher turnaround sell for me, primarily because of how costly the entry point was.

The future outlook

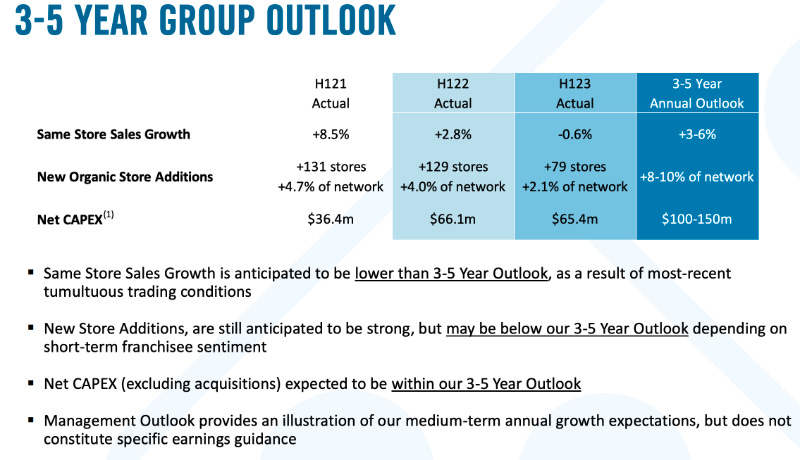

Management admits that same store sales growth is anticipated to be lower than previously announced 3-5 year outlook (i.e. lower than 3%). Management is also guiding for a slower growth in new store additions. Given these two parameters, the fact that the company will still incur Capital Expenditures (CapEx) of AUD 100M per year, is concerning, because as investors we will be getting less bang for the buck.

Company is taking some measures - such as closing down Denmark operations, and other cost cutting initiatives. It is likely to improve need for CapEx, and Cashflow is expected to bounce back to about $2.10 for FY’23, but earnings are likely still to be cut by about a fifth.

None of this bodes well for us investors.

Some Projections

Given the lower bound of Same Store Sales growth of 3% and lower bound of Organic Store Additions of 8%, the 3-5 year outlook would have roughly trended at ~11%. Let’s take that as a medium growth rate. Let’s then assume that the company does poorer than that in the medium term outlook and only does a 8% growth. We can also project what might happen if the company gets back to its historical growth rate of 18%. All growth are applied on Earnings per share (EPS), while dividend payout is kept at 70% which is the historic lower bound for this stock.

Low Growth Rate (8%)

Of course this is hypothetical and the numbers are all assumptive, but it is somewhat depressing that a company that grows its earnings by 8% a year for 5-6 years might still end up only giving you just about your money back. That’s the incredible result of the folly of paying too much for a stock!! The end P/E assumption of 18x is purely a conservative estimate. It is possible that the P/E could be wildly off at that point of time.

Medium Growth Rate (11%)

High Growth Rate (18%)

As we can see, it will take the company going through another exceptional growth phase for us to obtain good returns.

To be fair, we also should consider the possibility that the company may do things that are outside of their current playbook. Some possibilities include:

Divest away non-profitable, non-growing segments of the business and return capital to shareholders through dividends or buybacks

Diversify into other forms of fast foods, with the possibility of hitting new growth areas, possible organically, or possibly through acquisitions.

Cuts out dividend altogether, retires debt and uses the cash to go into either retiring stock or going into aggressive acquisition mode, with a view of changing the composition of revenue in the medium term.

On the other hand, the company could continue to perform poorly for another year or two, stock price gets cut in half and a Private Equity (PE) firm swoops in take the firm private for a discount, leaving us all with permanent loss of capital.

The AUD 4B question4 then is where would the company fall? At the moment, my sentiments are not too much on the optimistic side.

What do I plan to do?

Nothing much for the time being. It is a wait and watch situation. True to coffee can investing philosophy, I don't plan to sell any of my stock. However, I am not enthusiastic enough about the future prospects to add to my position. In any case, I am planning to go through the annual report when it comes out in late August and see what management has to say.

It is also worth mentioning that there are other stocks in my portfolio, such as JD.com (HKG:9618), Amazon(AMZN), Costco (COST), Microsoft (MSFT) and Mastercard (MA), all of whom are similarly priced - i.e. on the costly end, with an aspiration of growth perfection. It might be time to keep a closer eye on those too.

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

At a mere 40 years age, DMP is ranked the 32nd oldest in a portfolio of 50. The portfolio is of median age 58 and average age 74. Companies that get older tend to go on and on, an attribute highly desirable in a long term portfolio.

This paragraph was written by ChatGPT.

Approximate current market cap of the company.