Holding Steady: A Mid-Year Look at the Portfolio

A new stock joins the mix, but the focus remains on long-term, low-churn investing.

As we close out the second quarter of 2025, it’s time for a quick check-in on the Coffee Can Portfolio - what’s changed, how it’s performing, and what to expect in the months ahead.

🧺 Portfolio Changes

There’s been just one new addition this quarter: Facilities by ADF (LON:ADF), the UK’s leading provider of serviced production facilities for the film and TV industry. I recently wrote about the opportunity and have since initiated a small position—less than 1% of the portfolio.

While Q2 itself was relatively quiet, 2025 has seen more portfolio activity than I would normally prefer. The Coffee Can approach is designed to minimize churn, and I don’t take portfolio changes lightly. That said, most of the trimming and repositioning happened in Q1, and Q2 has been more about deliberate, high-conviction additions that I intend to hold for the long run.

⏳ Why Fewer Changes Going Forward?

I expect the rate of portfolio activity to slow down significantly in the months ahead. Two reasons:

New job, less time: I’ve recently started a new role that’s both exciting and demanding. With onboarding, new relationships, and family commitments all needing attention, I have less bandwidth to actively scout for new ideas. That’s okay—the portfolio is designed to be low maintenance.

More conviction, more inertia: The Q1 changes were made to concentrate the portfolio and raise the bar for inclusion. I’m now at a place where I’m happy with what I hold. Unless I find something truly compelling and have a reason to exit an existing position, additions will be rare and spaced out.

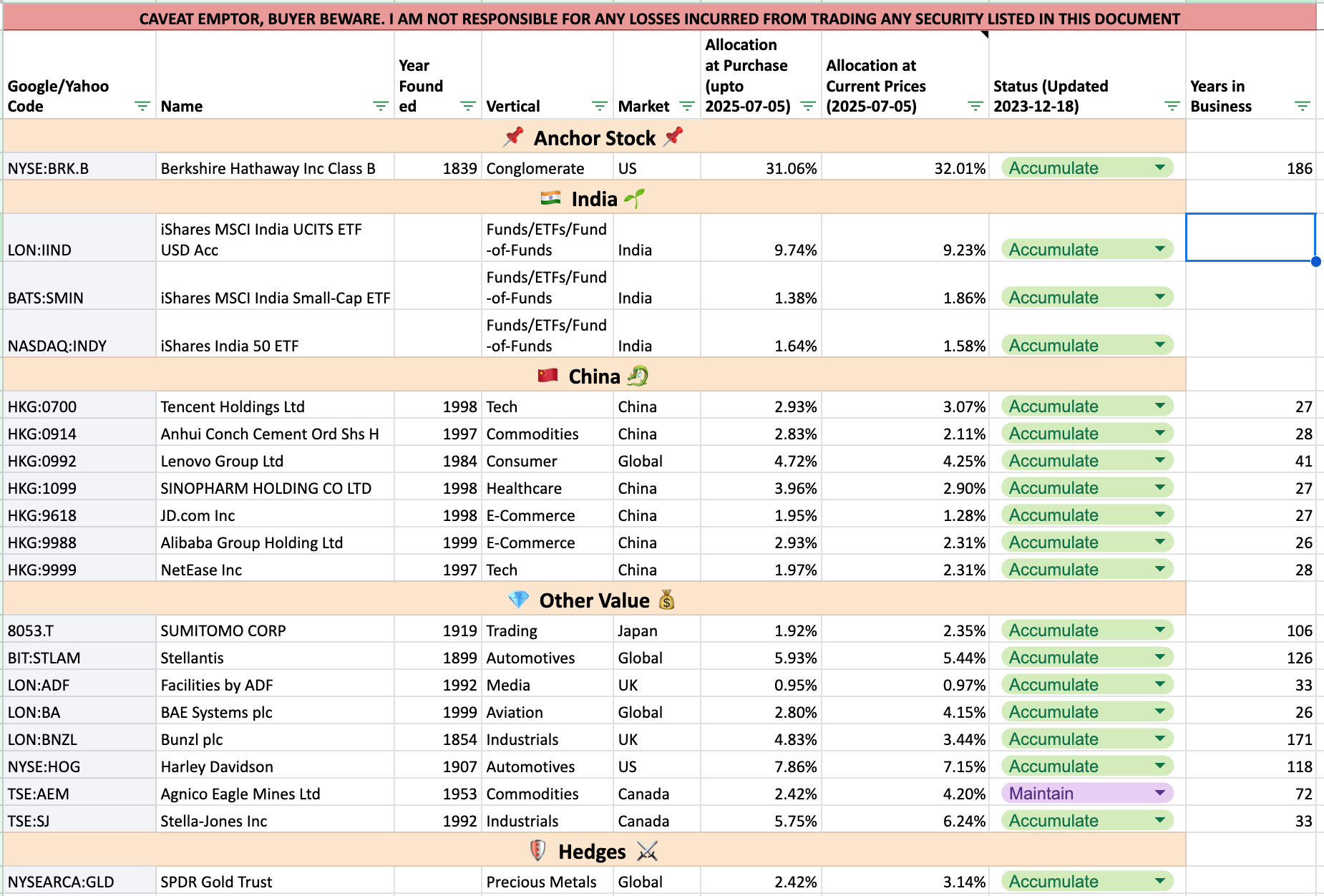

🧾 Current Portfolio Snapshot

The portfolio now looks like this:

Median company age: 89 years (down from 106 pre-Q2)

Sector & geography: Well diversified

Dividends: Roughly half the positions pay dividends; overall yield is in the 2–2.5% range

Valuation: Low P/E ratios; no high-flying tech stocks

In short, it’s a defensive portfolio, built to weather storms. I believe that makes it especially suitable for volatile or downturn-prone markets.

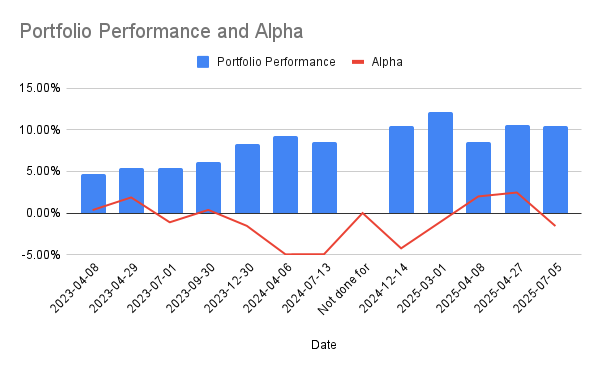

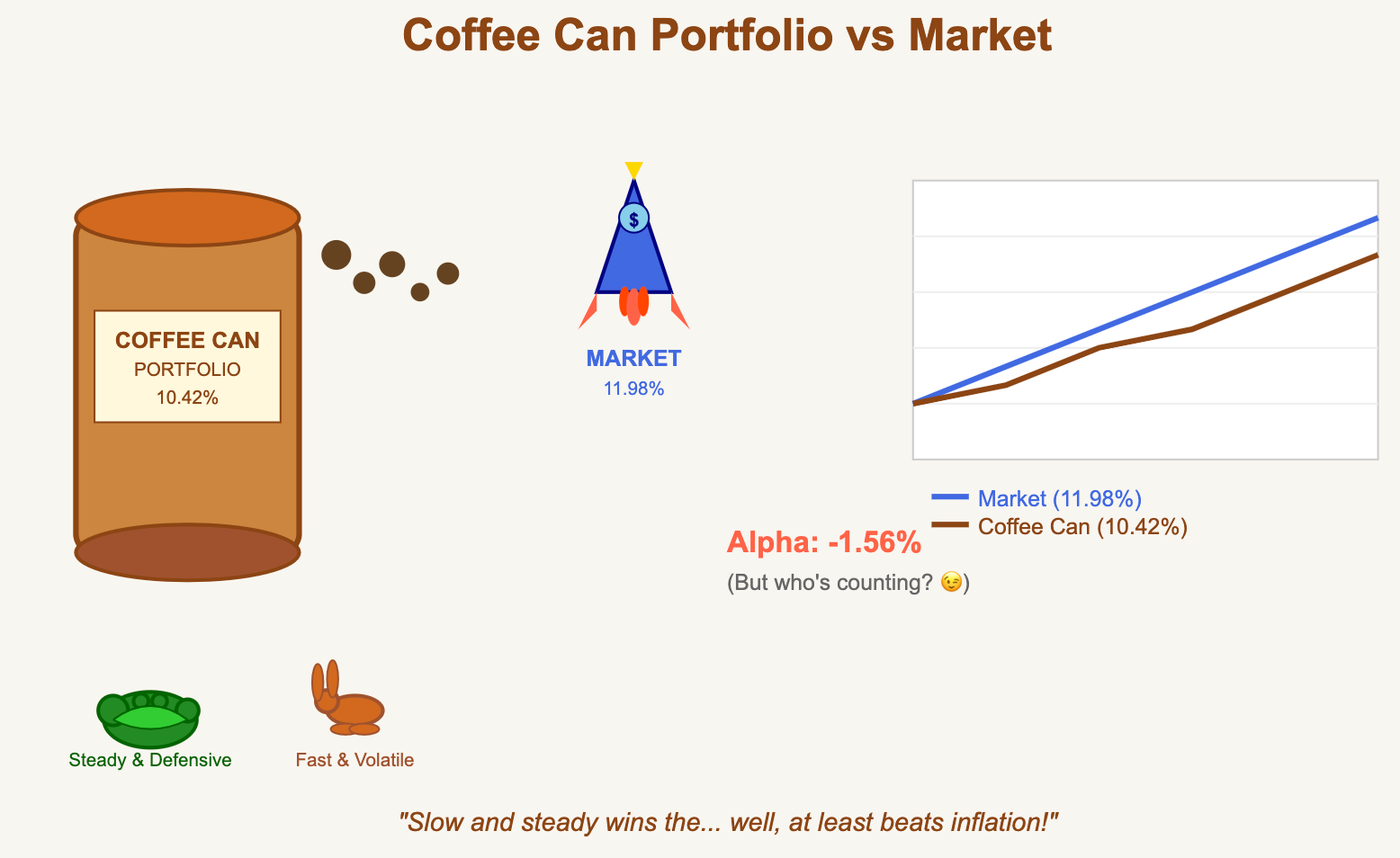

📉 Performance Overview

The flip side of playing defense is that when markets surge, the Coffee Can Portfolio often lags. That has been true for much of its history. Over time, it has danced in and out of alpha—spending more time under than over.

As things stand today today:

Total return since inception: 10.42% (p.a. on CAGR basis)

Benchmark return (same period): 11.98% (p.a. on CAGR basis)

Alpha: -1.56% (p.a. on CAGR basis)

That’s not ideal, but not alarming either. Getting a 10%+ return when inflation over the past 5 years has been <5% is a reasonable way of building real wealth. And even if the alpha has been in and out of positive territory, the returns from the portfolio seem to be settling into a rhythm indicating lower volatility.

What’s dragging performance?

Berkshire Hathaway, which is over 30% of the portfolio, had a tough Q2, dropping 10%

Chinese holdings continued to underperform

Still, a negative alpha when your portfolio is filled with quality companies trading at cheap valuations isn’t necessarily a bad place to be. If the past is any guide, this setup is more likely to yield positive surprises than disappointments.

🧘 Final Thoughts

2025 has already brought more changes than I’d like, but the portfolio is now leaner, more focused, and built for the long term. The heavy lifting is largely done. From here, I expect to return to the slower, steadier rhythm that the Coffee Can ethos demands.

As always, thanks for reading—and happy investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

Insightful analysis. I'm curious—what's your reasoning behind choosing ETFs for your India exposure, while opting for individual stocks in your China and global allocations?