Summary Analysis: Facilities by ADF (LON:ADF)

A Call Option on the UK’s Film Production Revival

Today’s post is about a nano-cap company - one with all of £20Mn in market cap - yep, likely cheaper than the street you live on. Nano-cap trading comes with a lot of risks, including illiquidity, lack of regular reporting, and potential governance issues. So, please don’t take a big wad of cash and pile in. Think very carefully, do your own diligence, and then think again. If you decide to enter, keep your position in check, and your order size small. If order doesn’t fill, they don’t. Don’t try to force trades in a market like AIM. (Further disclaimer at the bottom..)

With the warning out of the way, let’s get into the meat of the story.

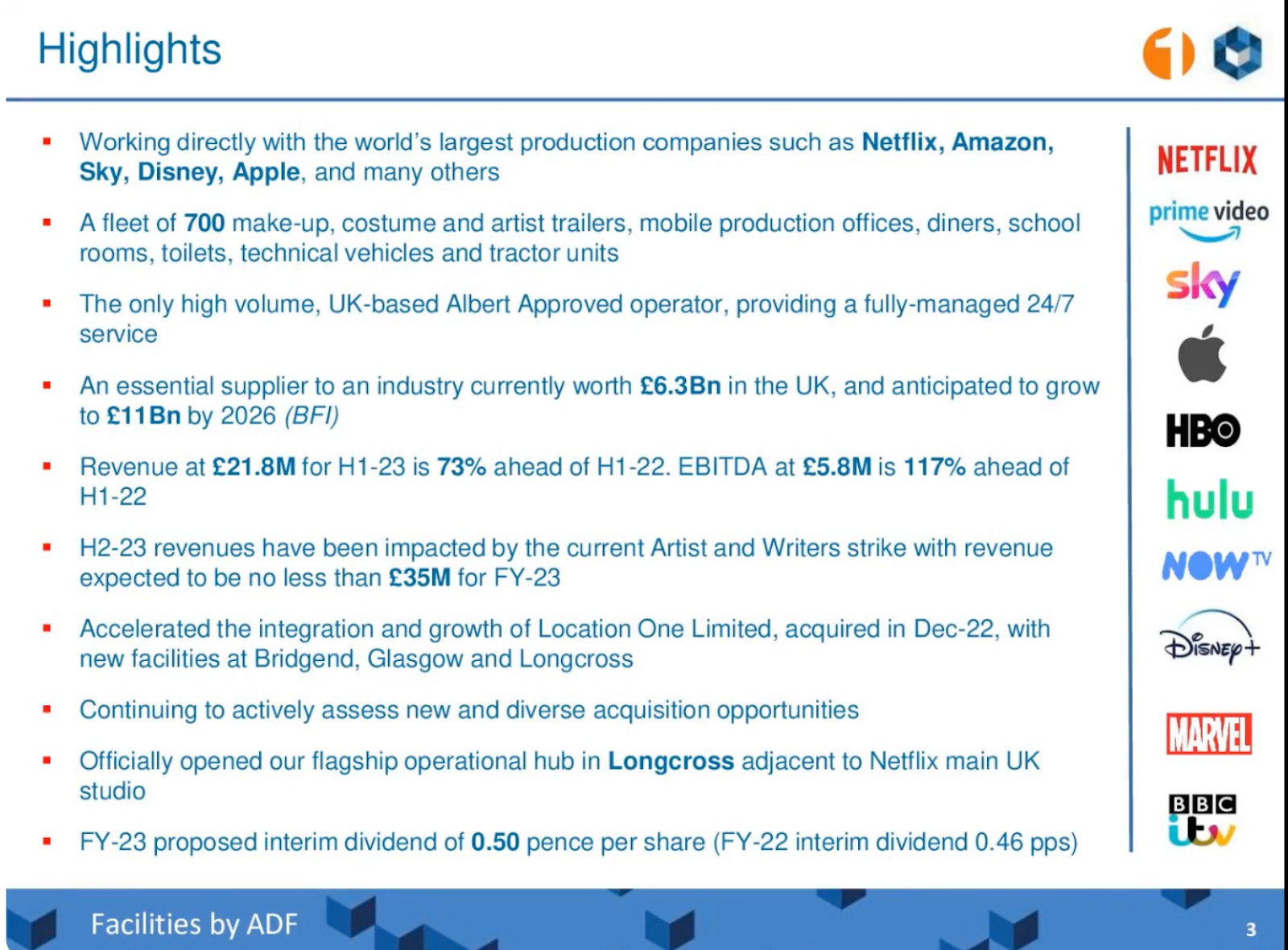

Facilities by ADF plc (LON:ADF), a nano-cap listed on AIM, may not be a household name, but behind the scenes of Britain’s biggest high-end TV and film productions, it plays a vital role in logistics support for film and TV crews. With a fleet of over 700 specialized mobile units—from artiste trailers and production offices to technical vehicles—ADF has serviced major titles including Slow Horses, Silent Witness, and Marvel’s upcoming Fantastic Four.

A Niche Business, with Dominant Market Share

ADF’s strategy is straightforward: be the one-stop-shop for production logistics. That goal has been reinforced through acquisitions like Location One and Autotrak, expanding its range to include portable roadways and location support services. As of 2023, ADF commanded roughly 27% market share in its niche, outpacing competitors like Move Makers and Translux.

Even in a traditionally lumpy industry, ADF’s fundamentals have historically looked solid. EBITDA margins exceed 20%, the business has been free cash flow (FCF) positive, and it ended 2022 with £9.5 million in cash and minimal long-term debt (mostly of the hire-purchase variety).

But like many others in the media ecosystem, ADF hit a wall in 2023.

The Hollywood Strike Fallout

The dual strike by the WGA and SAG-AFTRA in 2023 was historically significant. It was the longest writers' strike since 1988 and the first time since 1960 that both writers and actors went on strike together. This halted productions worldwide—including in the UK—and companies like ADF, which rely on international shoots, took a direct hit.

ADF’s own presentations (such as this one from mid-2023) clearly acknowledged the slowdown. While revenue and gross profit edged up around 10%, increased administrative costs eroded profitability, and earnings fell to just 0.94p per share. The company remained FCF positive, but cash reserves began to decline.

2024 saw continued pain. In H1, revenue was only £15 million, recovering slightly to £20 million in H2. For the full year, the company posted a loss of 3.2p per share. Yet again, cash flow held up relatively well. ADF has maintained a 1.4p dividend, consistent with its progressive dividend policy set at IPO, which the CEO reiterated commitment to in a recent presentation.

A Business in a Down Cycle—But Not Broken

From the outside, ADF looks like a business in distress. It is currently trading at around 18.8p per share (market cap ~£20 million), well below its 52-week high of 57p. The business is doing about £35 million in annual revenue, but earnings per share are negative. On the surface, not a slam-dunk investment case.

But dig a little deeper, and the upside narrative emerges.

This is a company that earned 2.8p per share in 2021 and doubled that to 5.4p in 2022. Book value jumped from £5.5 million to £25 million—partly due to the IPO and acquisition-driven growth. Its cost structure supports strong operating leverage, and any return to higher utilization could flow directly to the bottom line.

Forecasts suggest a potential £7.9 million profit in 2025, though I don’t buy it entirely. If that plays out, at today’s valuation, the company is trading at just 3x forward earnings. That’s cheap for a business with a leading market position, strong FCF generation, and minimal structural debt.

Even if the path there is volatile.

Insider Confidence and Activist Involvement

There are encouraging signs from stakeholders. Activist investor Rockwood Strategic has increased its stake to 4.4%, with related Harwood entities holding a further 7.6%. CEO Marsden Proctor recently bought nearly 80,000 shares at 31.6p. These moves indicate confidence in a rebound—and pressure on management to deliver one.

Dilution: A Double-Edged Sword

One concern often raised with nano-caps is dilution. ADF’s share count has increased significantly:

2021: ~46.7 million shares

2022: ~81.9 million

2023: ~85.2 million

2024: ~89.1 million

This is largely attributable to its IPO (30 million shares issued at 50p), the acquisition of Location One (3.4 million shares), and option exercises. While dilutive in the short term, these were strategic moves aimed at scaling the business. I am not too worried about it.

Risks and Realism

It’s not all blue skies ahead. Some structural risks remain:

The UK’s generous 25% tax credit for film production is subject to change—any reduction could materially impact demand.

Contract values have shown signs of declining over the past three years.

Liquidity is low—making it hard to exit quickly if the business continues to underperform.

Still, ADF’s cost discipline and focus on cash flow have provided a cushion during turbulent times.

Thinking Like an Owner

For an investor, ADF should be thought of as a long-dated call option. Not one to check daily, or even monthly. The upside - in a few years time, if international productions return in force - could be substantial: £50 million in revenue, £8–10 million in profit, and a potential re-rating to a market cap of £80–100 million. That would represent a 3x-5x return from today’s levels.

But the path there won’t be linear, and the risk of capital loss is real. Investors would be wise to take a buy-and-forget approach—checking in only during half-year results and assessing fundamental trends. Given the illiquidity, this is not a stock you trade; it’s one you patiently hold, or write off if things turn.

Bottom Line

ADF isn’t for everyone. It’s niche, volatile, and still navigating the aftermath of industry-wide disruption. But it is also a market leader in a recovering sector, with strong cash flows, activist attention, and a valuation that prices in very little optimism.

For patient investors willing to take a longer-term view, Facilities by ADF might just be one of the most asymmetric risk-reward plays on AIM right now.

Happy Investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.