Berkshire 2023 Review

Another solid year

Berkshire delivered its annual report last weekend, and Warren Buffett wrote a short but effectively Chairman’s letter to go with it. In the past few years, Warren’s letters (all in PDF here) have become shorter and more to the point. The trend continued with this year’s letter. (ps: I last wrote about Berkshire here.)

Berkshire is the largest single stock holding for my family, it is the largest holding (17.11%) in my Coffee Can Portfolio, and if my current assessments are right, likely to be the holding I sell the last. When you get a good tailwind, fly as long as possible with it.

Quick Recap

For the uninitiated in the company, Berkshire Hathaway (or Berkshire in short) is a conglomerate that is largely comprised of 3 sets of assets -

A set of insurance operations

A set of wholly owned non-insurance subsidiaries that range from energy to railroads to timeshare aeroplanes to manufacturing

A collection of marketable securities - essentially shares of other public listed companies, including Apple, Coca Cola, American Express and so on

In the world of insurance, premiums are collected first and paid out upon a claim later. This money, collected first, but waiting to be paid out, is called “float”. 2

Investing this float for a profitable long term investment income allows the company to earn both on the core insurance (called “Underwriting Profit”) and on the investment front (called “Insurance Investment Gain”). Berkshire has consistently focussed on maximising both - its insurance subsidiaries regularly produce underwriting profits (some $5 Bn in 2023) as well as Insurance Investment Gain (some $9.5 Bn.) It is float that is the primary source of the collection of the marketable securities that it holds and this collection is likely to grow with time.

Berkshire’s unique corporate structure encompasses the positive traits found in many asset classes - it is a bit of an ETF, it is a bit of a Private Equity Firm, it is a bit of a 60-40 fund (as it holds a lot of treasuries too), and it charges no fees for running this show, as it is structured legally as a normal operating public listed company.

For more, please read my Berkshire post from last year.

The letter

A quick summary of the interesting bits from the letter first.

Warren has written a full page homage to Charlie Munger, who recently passed away at the age of 99, and it is unsurprisingly poignant, but effective.

In the physical world, great buildings are linked to their architect while those who had poured the concrete or installed the windows are soon forgotten. Berkshire has become a great company. Though I have long been in charge of the construction crew; Charlie should forever be credited with being the architect. - Warren Buffett (Pg 2)

Warren wrote yet another very diplomatic critic of the accounting change that forces their investment mark-to-market changes to be attributed to their P&L, something he has been consistently, and rightly, harping on about since the introduction of the standard in 20181. If you are unaware of this issue, please go read Warren’s letters from 2018 - you will be a more informed investor.

Warren seems bullish on his Occidental Petroleum investment, where Berkshire’s interests are 27.8% of the company through shares and warrants.

Under Vicki Hollub’s leadership, Occidental is doing the right things for both its country and its owners. No one knows what oil prices will do over the next month, year, or decade. But Vicki does know how to separate oil from rock, and that’s an uncommon talent, valuable to her shareholders and to her country.

Warren writes about a page and half on the challenges faced at BNSF and is concerned about the capital it has been consuming and how the margins on that are challenging. He leaves the issues on an optimistic note, but it is easy to read the summary.

Though BNSF carries more freight and spends more on capital expenditures than any of the five other major North American railroads, its profit margins have slipped relative to all five since our purchase. I believe that our vast service territory is second to none and that therefore our margin comparisons can and should improve.

On a similar note, he is unhappy about the state of energy business in America and the negative turn on the regulatory terms.

When the dust settles, America’s power needs and the consequent capital expenditure will be staggering. I did not anticipate or even consider the adverse developments in regulatory returns and, along with Berkshire’s two partners at BHE, I made a costly mistake in not doing so.

We will talk about numbers later, but insurance continued to do well, producing $15 Bn in profits, as against $6.4 Bn previous year.

The Numbers ❤️❤️❤️

Operating income2: $27.6 billion for 2021; $30.9 billion for 2022 and $37.4 billion for 2023.

Free Cash Flow of ~ $30 Bn in 2023

Total investment holdings of securities and treasuries add up to $561 Bn (up from $473 Bn last year)

Number of B-Shares has declined from 1.468 Bn to 1.310 Bn due to stock repurchases (with 4th quarter average being $347.16 per share and the ones before, presumably lower3).

At year end 2023, Berkshire’s market cap was $784 Bn. After taking out the investment holdings of $561 Bn, the remainder of the operating businesses are valued at $223 Bn, and those businesses collectively earning circa $17 Bn4, making the core businesses 13x earnings, or about 7.5x FCF.

This business continues to excel and available at a reasonable price for ongoing investments.

The comparison

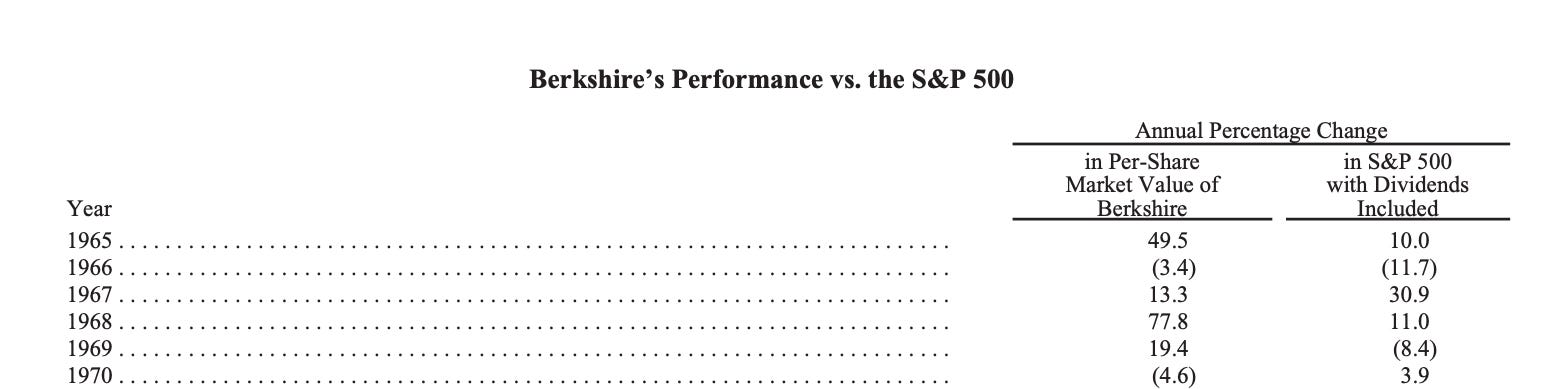

Every year, Berkshire publishes a comparison of Berkshire’s performance vs the S&P 500 in a table that looks like:

ending with

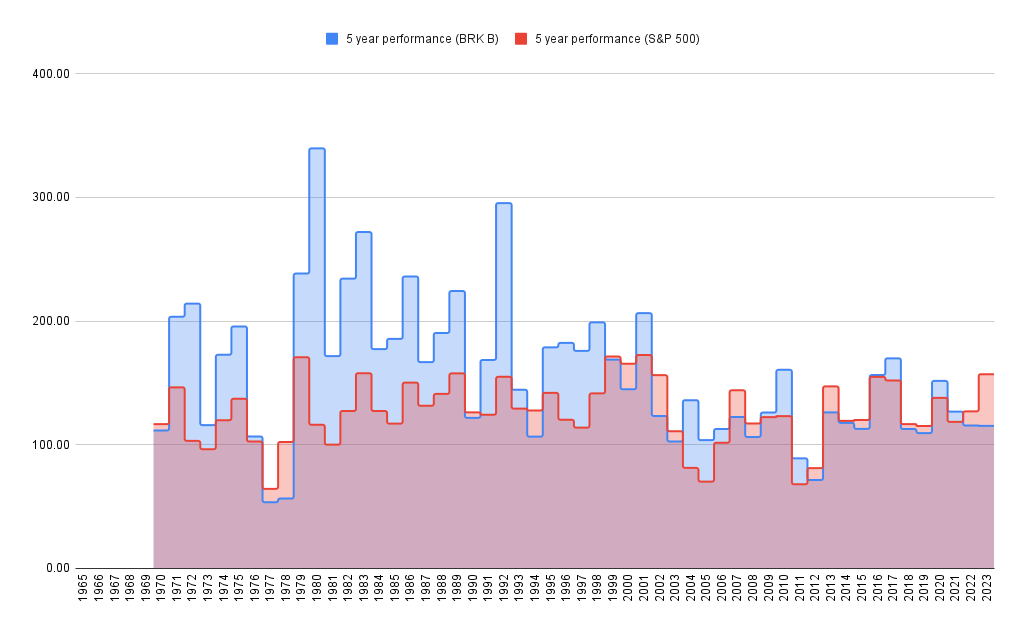

I took all of this data and compiled what transpired over rolling 5 & 10 year periods.

It is clear that Berkshire’s ability to outperform the S&P 500 on a consistent basis has eroded in recent years, but it continues to hold on to its own in some years, specially in the years S&P 500 tends to see reversals. In the last 2 years, for instance, Berkshire has outperformed S&P 500, even after S&P 500’s recent bull run.

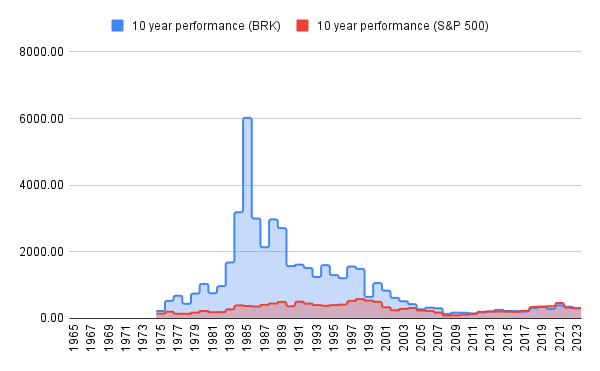

On a 10 year basis, S&P 500 doesn’t seem to compete for most of Berkshire’s history.

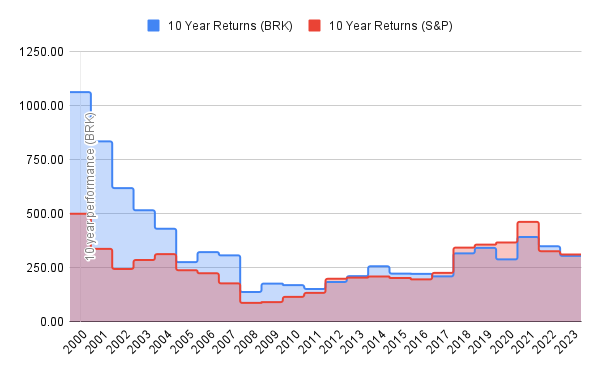

Perhaps we need to zoom into the most recent years. From the turn of the millennium, a 10 year period has only produced 7 wins for S&P 500 vs 17 wins for Berkshire. When Berkshire outperforms, it stands out by a margin, but when S&P 500 does so, it barely clears the Berkshire hurdle.

Summary

In Berkshire’s history, 2023 will be a year remembered for the loss of Charlie Munger. Beyond that, 2023 marks another year for

the continuously cash generating..

well-run machine that Berkshire is..

spitting out cash from core businesses..

investing that cash both in securities and in treasuries on our behalf..

acting as a better custodian for our fiduciary interests than I could personally be..

while reducing its own share count, hence increasing the ownership interest for continuing shareholders like my family..

and doing so in way that its long term performance is comparable to S&P 500 over long periods of time.

I will take more of it. Thank you.

As always, happy investing!!

Disclaimer: I hold positions in some of the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

This makes so many analyses difficult. I was recently playing around with SimFin data and identifying which companies had high ROCE or FCF on capital employed (FCFOCE as I labelled it.) Berkshire was an exceptional to my analysis because its “Income from continuing operations” gyrate so much due to the addition of Investment Mark-2-Market into the P&L.

One of my problems with using screeners is that such nuances are lost and it is likely you will miss out on a great company like Berkshire by being strictly algorithmic, unless you apply a series of exceptions, which makes it more subjective and less algorithmic, defeating the primary thesis.

This includes dividend from investments but not mark-to-market capital gains. This is a truer measure of the economic value of the company.

Almost all recent repurchases have been net accretive to continuing shareholders. This pattern is not guaranteed to happen in the future, but the consistently with which it is net accretive, is a positive sign for long term continuing shareholders like us.

I am excluding Investment income under sub-head of Insurance, given that that amount is produced by investments, which has been taken out in valuing the core businesses.