Fresenius Corporation: A Review of Opportunity

A bit of special situation, a pinch of value, and a play on healthcare growth

Founded in 1912, Fresenius (ETR:FRE) is a German healthcare company that provides products and services for dialysis, hospitals, and outpatient medical care in 150 countries. Fresenius operates in four business segments (ownership in brackets): Fresenius Medical Care (32%), Fresenius Kabi (100%), Fresenius Helios (100%), and Fresenius Vamed (77%).

Among the two wholly owned subsidiaries, Fresenius Kabi is a global leader in the production of intravenously administered generic drugs, clinical nutrition products, and medical devices, while Fresenius Helios is Europe's largest private hospital operator, with more than 100 hospitals and clinics in Germany, Spain, and Latin America.

Among those without full ownership, Fresenius Medical Care is the world's leading provider of dialysis products and services, serving over 345,000 patients worldwide, while Fresenius Vamed provides services for the planning, construction, and management of healthcare facilities.

Fresenius Medical Care is in fact listed on its own through tickers in Germany and the US - ETR:FME/NYSE:FMS (shortened to FME/FMS elsewhere in this post). However, this set up is based on AG & Co. KGaA structure, essentially a partnership limited by shares (KGaA), whose general partner is a stock corporation (AG), which is Fresenius Corporation in our case. From Wikipedia on AG&Co KGaA Structure:

This legal form is often chosen for listed family companies or companies with an influential major shareholder whose family or major shareholders want to sell shares in their company but retain control of the company.

Essentially, even though Fresenius Corporation is not a majority owner, it still operates the FME/FMS business through strategic control. Other FME/FMS investors currently have little say in how the subsidiary business is run.

With a proposed change this year, Fresenius Corporation plans to convert the legal structure to German Stock Corporation after which FME/FMS will have significant autonomy in its operation, granting all FME/FMS shareholders equal voting rights, while also freeing up Fresenius Corporation to focus on other businesses, and paving the way for divesting its holding in FME/FMS. We will come back to why this might be an interesting development in this story.

As it stands then, 44% of Fresenius Corporation’s revenue comes from Europe, and North America represents another 40%, so Fresenius primarily represents a play on western world healthcare. In terms of segments, Fresenius Medical Care (FME/FMS), the 32% owned business that provides dialysis care, represents 47% of the revenue, with another 29% coming from Fresenius Helios, the hospitals operation business.

Latest Results

Before the 2022 results, this was a relatively staid business, growing revenues 8.67% and EPS by 10% over the 15 previous years, supporting an ever increasing dividend, which itself was growing at 11% CAGR, all along with a healthy balance sheet. In fact if you look at revenue growth, Fresenius is doing better than competitors DaVita, HCA and Baxter, when compared on long term basis.

It had a brief spurt where its price went up somewhat exponentially, but even ignoring that, the corporation has had the respect of the markets trading between 17x and 20x trailing earnings. This phase is when I got involved in the business.

A few weeks back Fresenius Corporation dropped its 2022 results - the company grew its revenue to €40.8B, up 9% from €37.5B from last year. However, net income attributable to Fresenius shareholders declined to €1.37B from €1.82B last year. If you exclude special items (and I will come to it in a bit), net income attributable to shareholders declined to €1.73B from €1.87B last year.

From the management’s own commentary:

Fresenius’ business was negatively impacted by the difficult macroeconomic environment in 2022. This included increased uncertainties, inflation-related cost increases, staff shortages, supply chain disruptions, the continued impact of the COVID-19 pandemic, and increased energy costs. This had a direct impact on customer and patient behaviour.

Cost of materials rose from €8.8B (23.5% of revenue) in 2021 to €10.2B (25% of revenue) in 2022. This bump in costs of materials has pushed up Cost of Goods Sold (CoGS) from 72.52% to 73.7%. Personnel costs on the other hand have risen from €15.6B (41.6% of revenue) in 2021 to €17.4B (42.5% of revenue) in 2022. As you can imagine, if two of your biggest costs, input materials and personnel costs go up, then it is but natural that the net income line is going to be challenged massively. In fact the entire drop in net income can be explained just by these two line items on the P&L.

Fresenius Corporation’s headaches at the moment are quite widespread, as costs are increasing in all segments, specifically at Fresenius Vamed which showed a massive decline in EBIT from €67M in 2021 to €1M in 2022. However, Vamed is a relatively small part of the corporation and the wholly owned subsidiaries - Fresenius Kabi and Fresenius Helios showing either steady or growing PBTs of 0% & 5% respectively, so aren’t contributing to the declining income.

That brings us back to FME/FMS, which is becoming a bigger drag on Fresenius Corporation’s results than the other businesses. FME/FMS’s net income declined by some €296M, contributing to some 66% in the overall decline despite the fact that FME/FMS is only 47% of the revenue at the group level. Its share of group profit reduced from 53% to 49%, due to this degradation in the business. FME/FMS has been hit by US staff shortages and cost inflations this year, and it gave a lower guidance twice in the last year, also contributing to declining guidance at the group level.

Cost Control

In the short run, expect nothing to change and the business to continue to be challenged. From the management:

Fresenius also expects general cost inflation and labor shortages to have a significantly more negative impact on its business than in 2022, due to the fact that these pressures did not materialize until the second half of 2022. Accordingly, Fresenius anticipates stronger headwinds in 2023 than in the previous year.

In fact the company is now guiding for a “Broadly flat to high-single-digit decline” which means we should expect another year of challenging PBT numbers. What’s more worrying is that the CoGS line item has been steadily rising from 67.7% in 2016 to the 2022 number of 73.7%. So, unless the curve on this is bent, overall picture won’t improve.

Management knows this and is embarking on structural improvements to cost which are expected to yield results in the next 3-5 years.

Structural productivity improvements are expected to offset market headwinds and to create financial flexibility for future growth investments in the coming years. The new target is to achieve annual structural cost savings of around €1 billion at EBIT level from the fiscal year 2025 onwards. To achieve the targeted cost savings, one-time costs of around €700 to €750 million are expected at EBIT level, of which around 2 / 3 will be incurred in the year.

and

Thanks to our cost and efficiency program we have already realized €152 million in savings after taxes and non-controlling interests in fiscal year 2022, offset by €260 million in one-time costs. In line with previous practice, these expenses are classified as special items.

These costs related to the cost and efficiency program are the special items I sought to set aside when discussing net income earlier in the post. The above cost control measures should be taken in context. The biggest cost control opportunities for Fresenius Corporation comes at the FME/FMS subsidiary:

Ambitious financial targets require a high degree of cost discipline. We have increased our annual savings target by approximately one billion euros as of 2025, of which a large part is attributable to Fresenius Medical Care.

It is important to keep an eye on whether these improvements continue as promised in the future or not. I would like to keep an eye on personnel costs and CoGS as a percentage of revenue as the two most important metrics, improvement of which will significantly improve the profitability outlook of Fresenius Corporation.

FME/FMS Spinoff

Fresenius Corporation today controls 32% of the €12.5B market capped FME/FMS subsidiary, which means roughly €4B of the Corporation’s market cap value is attributed to the subsidiary. The rest of the business, which produced about €1.5-€1.6B of net income and facing less headwinds in terms of costs, is valued at roughly €10B, some 8x earnings, and some 0.5x revenue.

Assuming that the Corporation completes the legal structure changes in the next 12 months or so as promised, while continuing on its goal to improve costs structures at the FME/FMS subsidiary, it is very likely that we will be left with the opportunity of extracting €6B or more in a strategic divestment in a 3-5 year trameframe. The upside will come both from improved net income, as well as the likely premium to be achieved by selling to a strategic owner.

Tailwinds in Healthcare

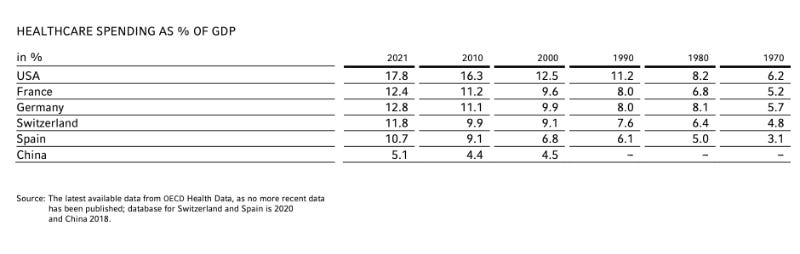

As mentioned earlier, this company is a play on global healthcare trends. Healthcare spending as a percentage of GDP has been growing in every single region, every decade. There is a secular trend towards significant investments in extending the longevity of an ageing population and improvements in the financing structures of healthcare1 means that it is likely to be a tailwind, at least in some regions for a few more decades.

As demographic changes pose fundamental challenges to societies worldwide, with people living longer and the pace of population ageing increasing significantly, Fresenius, with their healthcare products and services for critically and chronically ill individuals, stands to gain from this trend.

In line with that opportunity, revenue has grown 8.9% p.a. over the past 15 years as well as in 2022, which is a very good trend. As mentioned before, long term revenue growth is outperforming those of competitors DaVita, HCA and Baxter. However, EPS growth is trailing behind, only growing by 7% p.a, again attributable to the shrinking PBT margins in the company, which we discussed above.

Valuation

The company trades today at somewhere around 10-11x trailing P/E. Traditionally this business trades between 17x and 20x, only dropping around the 9-11x in the past two years, and for very good reasons, as mentioned above.

With a cleaner balance sheet and a lighter, predictable income statement, post FME/FMS divestment, and improved cost structure, the rest of the business is likely to rerate to at least 14-15x earnings, which is the norm for other healthcare companies, both facilities management ones as well as pharmaceutical ones, listed in Europe. Those listed in the US command an even better average of 17-20x. Note that the 14-15x is still less than the historical average for this company in the past, so I am being significantly conservative here.

On a Sum of Parts basis, the corporation could be valued at as much as €25-€30B in value, post-2025 if the two important catalysts prove to be true, which is roughly 2x where we are at the moment.

Alternative Valuation

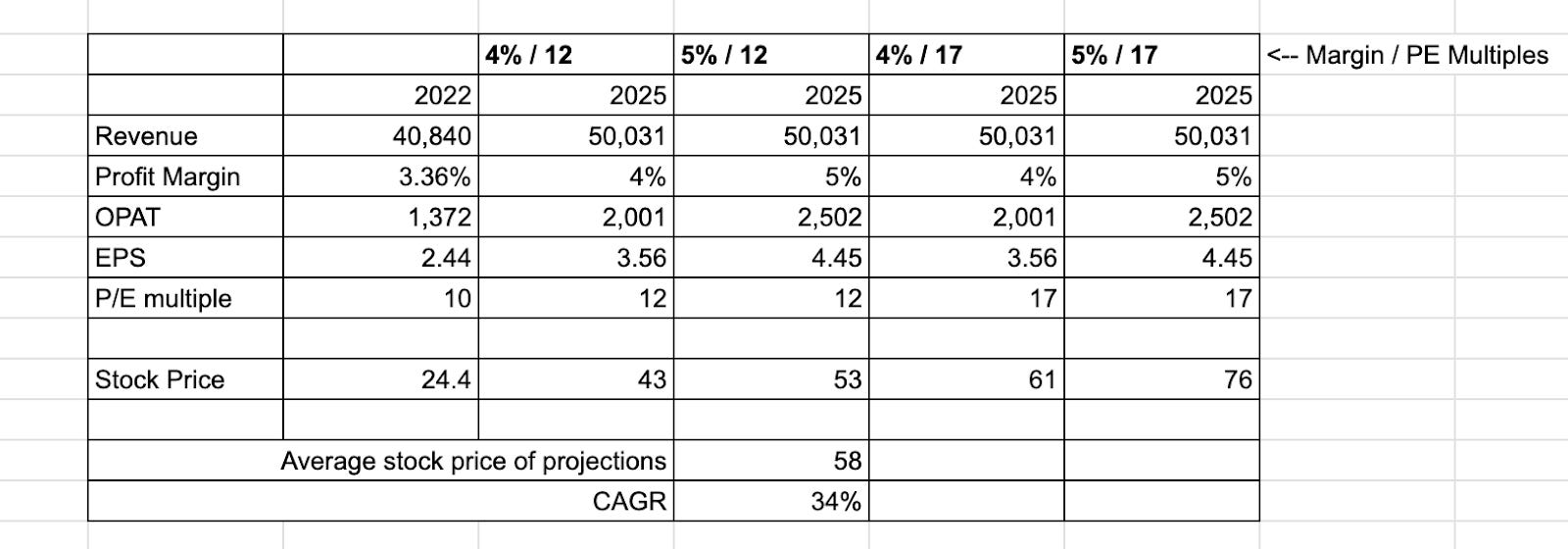

Another way to look at this opportunity is to play this purely on the cost structure improvements and leave out the FME/FMS spinout altogether. Looking 3 years out, here are a few projections on the company’s metrics. I have reduced revenue growth to a modest 7% (vs 8.9% today) for this exercise, and play on both profit margins and PE multiple. 5% profit margin, for instance, is the 10% running average for this business, while 17x PE is at the lower range for the business from before 2022. So, these expectations aren’t outlandish, if the business indeed turns a corner.

If you look at the rightmost column, the OPAT improvement in 2025 is roughly €1.2B, in line with the savings the cost efficiency programs are supposed to bring in by 2025, so again, not out of reason.

At €58 a share, this business will be valued at ~ €30B market cap, which is another way to get to a similar valuation as the one placed above.

Risks

Both the Fresenius Corporation and FME/FMS have very new CEOs - Michael Sen and Helen Giza, taking on their roles in Oct and Dec of 2022 respectively. While both had short tenures within the Fresenius family before their current assignments, they are still quite new to the top role and are now taking on important cost control and legal structure projects. The success of these projects under new management is always a risky endeavour.

The second big risk is that the process of restructuring gets far more complicated along the way, takes longer and is jettisoned either due to costs, or possibly due to change in command. Combined with a relatively new management, that risk is ever present.

As it stands, I am finding it interesting enough to partake in it, but readers should consider these risks while evaluating a position.

Summary

The way I see this company is simple - it is a good play on healthcare with a growing revenue line. It has a cost & structure problem, but management is aware and taking steps to fix it. If the program to fix these comes off, then the company will re rate significantly, due to improved PBT, cleaner balance sheet and a possible expansion on the multiples.

Given the cheap enough price, and the allocation in my portfolio being small (ranging between 1.25%-1.4%), and given that I am getting paid a 3-4% dividend yield to hold my position on a possible improvement to the margins, I am happy to collect up small lots of the shares every few months and observe if there is an inflexion.

Indeed, the Value/Special-Situations aspect of this opportunity is interesting enough that I might consider taking a larger position outside of my coffee can portfolio, with a view of holding it for a shorter time frame (3 years or thereabouts) with a view of getting paid through a possible rerate of this business.

Essentially healthcare insurance subscription and coverage will grow with time in regions where these numbers are still quite low.