Summary Analysis: Challenger Financial Ltd

In the right place long term, but facing short term challenges

Founded in 1985, Challenger Financial (ASX:CGF) is a leading provider of annuities1 in Australia, offering products that provide retirees with a guaranteed income stream for a specified period or for life. In addition to annuities, Challenger also offers other retirement income solutions, such as retirement savings accounts and investment-linked products. The company manages assets on behalf of its clients and provides investment management services through its subsidiary, Fidante Partners. While it primarily operates in Australia, it has some revenue streams through joint ventures in other geographies like Japan.

Today, the company operates in 3 segments:

Life/Annuities: This is the aforementioned annuities segment, which produces ~80% of all of the income for the group. This post will be mostly focussed on this segment.

Fund Management: This is an active fund management business, which managers different kinds of assets and runs its own fund. This earns ~20% of the income today.

Bank: This is a tiny segment borne out of acquisition of MyLifeMyFinance in 2020 and has been agreed upon to be sold to Heartland for roughly as much as they bought it for, though the division incurred minor losses for the year in operation.

As it stands, the future of the company is primarily in the Life/Annuities segment so let’s dig into that. The Life/Annuities business operates in an environment of a long term tailwind. From their report:

As Australia’s superannuation system grows, the retirement phase of superannuation is expected to increase significantly. The number of Australians over the age of 65, which is Life’s target market, is expected to increase by nearly 50% over the next 20 years. Reflecting these demographic changes, and growth in the superannuation system, the annual transfer from the savings phase of superannuation to the retirement phase was estimated to be approximately $76 billion in 2021.

The purpose of the superannuation system is to provide income in retirement to substitute or supplement the Government-funded age pension.

Australian superannuation assets are likely to grow from A$ 3.3Tn today to about A$ 9Tn in 2042 and given that Challenger is an extremely well established brand in this space, this company is well placed to take on growth in this segment.

In an annuities business, the company issues the annuity policy, upon which the company gets to hold the annuity-holder’s corpus, which it is free to invest in order to match the future payments required to fulfil the annuities’ payments need. Given that if any of the annuities holders pass away while holding the policy, the monies are for Challenger to keep. This means that it can offer better rates than the currently available debt rates, even on fixed term annuities.

Currently the company deploys some 80% of its assets in fixed income securities with the rest sprinkled over real estate, equity, infrastructure, derivatives and hedging2. In summary, the investments are conservatively matched to the outflow. In addition, the company is well capitalised, even by the statutory requirements, maintaining 1.6x the capital base required as per regulations.

Golden Days

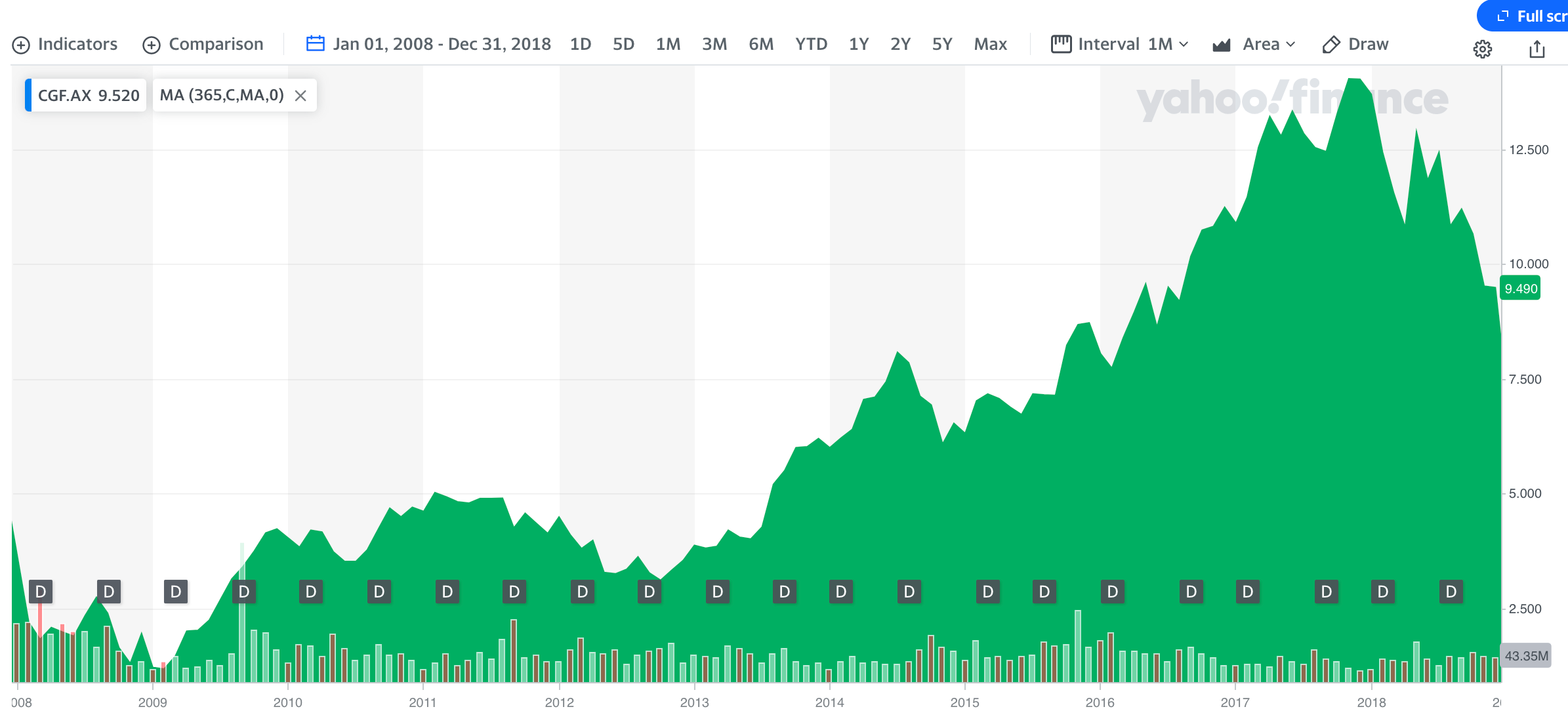

Between 2009 and 2018, the company grew its Normalised OPAT3 from A$ 218Mn to A$ 406 Mn, along the way, increasing dividends from 0.125 per share to $0.355 per share, returning a sum total of A$ 2.4 in the 10 years as fully franked4 dividend. The stock was roughly a 10 bagger along the way, growing from ~1.30 to ~13.30.

Challenges in regulatory environment

Since then the company has faced some headwinds. Specifically, a Royal Commission was set up in 2019 to look into Misconduct in the Banking, Superannuation and Financial Services Industry, the hearings and findings of which have resulted in significant structural change across the Australian wealth management and financial adviser market.

From their own annual report:

There have been a range of regulatory changes that have had a significant impact on the economics for many financial advice practices. Regulatory changes include a shift away from commissions to fee-for- service, resulting in lower revenue per client, and the best interests duty which is increasing focus on holistic advice over transaction advice. Advisers are also increasing education and compliance activities, which is reducing focus on the acquisition of new clients and servicing of their existing book.

There have been significant withdrawals of advisers from the market through the major banks generally exiting or reducing their exposure to wealth management, which is contributing to a reduction in the number of financial advisers aligned to the wealth management operations of the major banks.

There has been higher adviser turnover with advisers either migrating from licensees aligned to the major banks to independent adviser networks, switching licensees in the network, becoming self-licensed, or leaving the industry altogether.

As a result, the Australian financial advice market continues to undergo significant structural change, with adviser numbers reducing by 16% year-on-year and advisers moving from the major banks to Independent Financial Advisers (IFA) networks. At 30 June 2020, IFAs accounted for approximately 72% of the advice market, up from 60% five years ago1.

Representing the shift away from major hubs to privately owned licensees, in 2020 62% of all advisers were licensed to a privately owned licensee, up from 32% five years ago. Institutionally owned and aligned advisers, which has traditionally been the largest segment represented 38% of the total advice market, down from 63% five years ago1.

These industry changes are impacting Challenger’s annuity sales, especially term annuity sales which were well supported by advisers aligned to the major banks.

Challenger believes in the need for financial advice, particularly in the retirement phase of superannuation and is supporting advisers as they move across licensees and ensuring Challenger products are widely available on investment and administration platforms.

These changes have affected business significantly. Annuity sales tanked by more than 25 per cent in the two years to 2020, suffering multibillion-dollar outflows following the Royal Commission findings, which depleted the ranks of registered financial advisers, who are widely seen as the most effective annuities advocates.

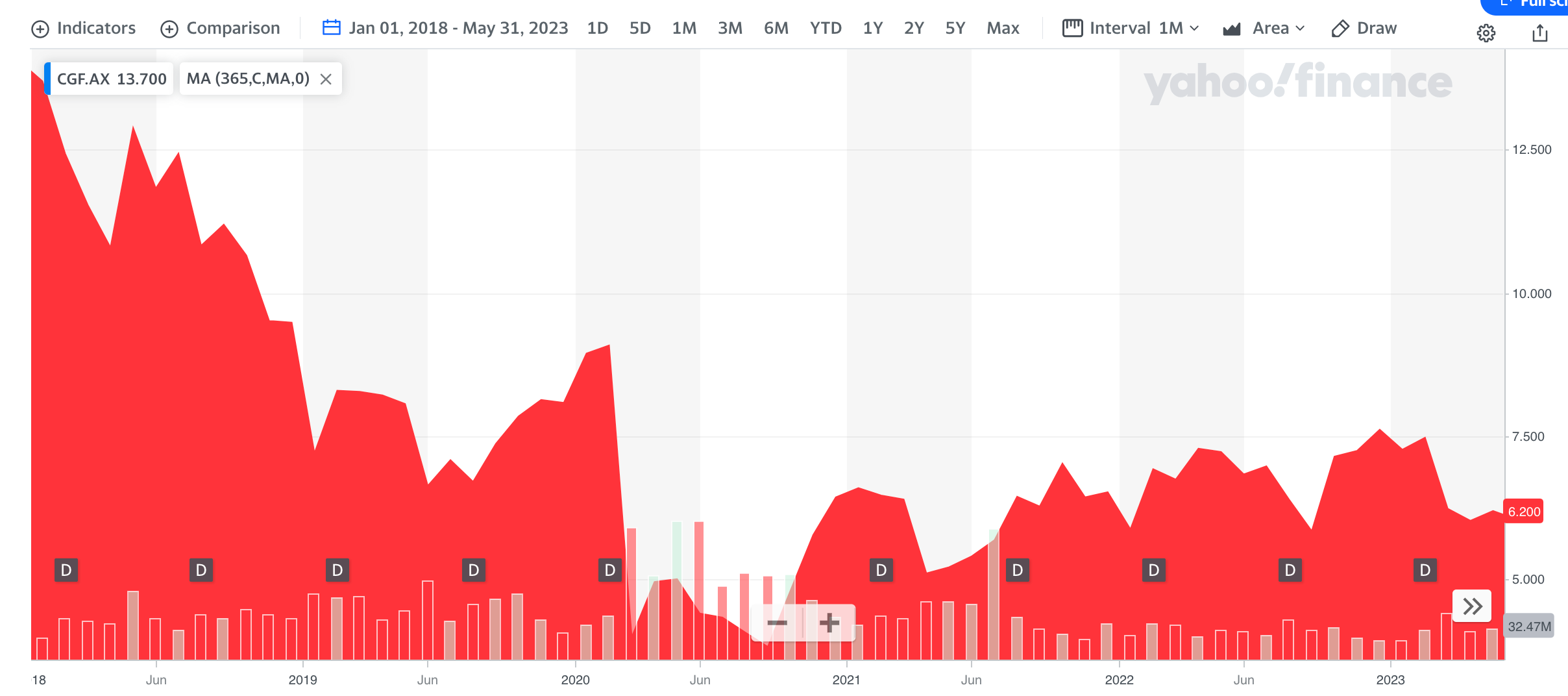

Normalised NPAT has dropped from A$ 406Mn in 2018 to A$ 278Mn in 2021 and has only recovered now in 2022, to A$ 321, essentially where it was in 2014. 15 years of growing dividends were finally cut in half in 2020 (going from $0.355 per share to $0.175 per share). Share price followed suite cut from ~$14 and change in 2018 down to $3.7 and change in Q3’ 2020, a drop of about 3/4ths of value of the company.

Last 2 years

After having a horrific few years, which have significantly challenged the business, the company is slowly picking up the pieces and putting the business back together on the path of growth. Normalised OPAT grew in 2022, and is likely to pip it again in the current year (ending June 30, 2022). Dividends have moved upwards from $0.175 to $0.23 per share last year.

Both executive and board leadership have changed hands5, with new CEO Nick Hamilton and CFO Alexandra Bell, along with new Chair, Duncan West coming in in the last 2 years. So far the new leadership seems to be in doing the right things, such as shutting down the Challenger Bank experiment (selling it to Heartland, ASX:HGH at cost) releasing excess capital of about A$ 100Mn6, rolling over debt through issuance of new subordinated notes7, and selling some real estate fund management to Elanor (ASX:ENN) in exchange for a 18.2% stake in the listed entity8, which has been favourable for us shareholders as the ENN’s shares have reacted well since.

Going Forward

While the flurry of activity is all heading in the right direction, business continues to be challenging. In their latest trading announcement, the company announced headwinds in institutional life sales (which was well over 50% of the book in previous years):

Institutional sales decreased by 50% to $1.1 billion, with institutional term annuity sales of $97 million (down 90%) due to lower reinvestment rates and Challenger Index Plus sales of $963 million (down 13%).

Institutional term annuities tend to be shorter duration than retail policies, typically 1-year. Challenger’s priority is to grow longer duration and more profitable business and has remained disciplined on institutional term annuity pricing.

The drop in institutional sales has been offset by retail sales (growing 89%) and overall life book grew in value by $1 billion, reflecting 5.5% book growth in 1H FY23.

The company states that it is “benefitting from a more favourable macroeconomic environment, with higher interest rates helping to accelerate annuity sales and expand margins”9.

I expect the company to see continued headwinds in Institutional sales, though Challenger has proved to be a good operator of B2B relationships in the past, while it will still continue to be able to gain business through retail route.

The company however finds itself in the tailwind of a growing market, with a product well suited for a vast majority of customers, with the product becoming relatively more valuable in the past 2 years (due to better annuity rates, which are joint at the hip with interest rates). The challenge remains the distribution channel, but nothing mentioned in the Royal Commission findings are outlandish, and in fact countries like the UK already have similar regulations and life has moved on. Australia will continue to lose advisors till it hits equilibrium after which the channel should stabilise and revenues should grow.

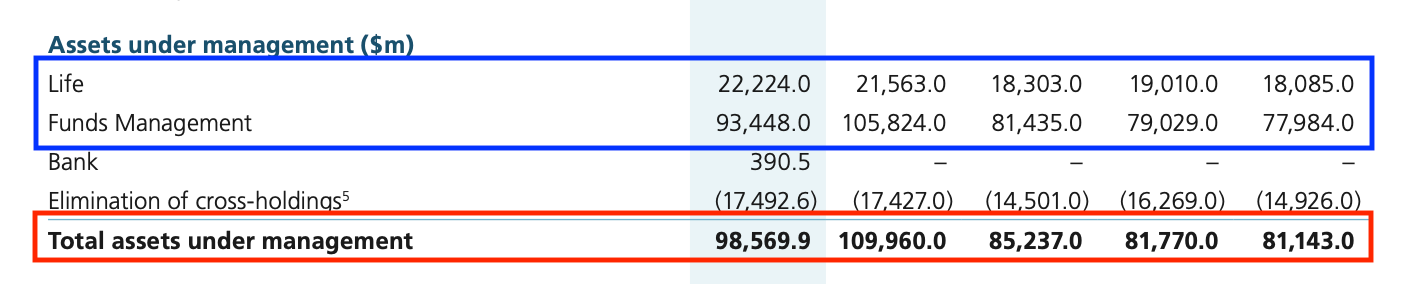

If you need evidence for this, it is to look at the assets under management for both Life/Annuities as well as Fund Management both of which, despite all the challenges facing distribution, are still growing over the past years, as well as total assets under management (which is a combination of corpus from Life/Annuities and Fund Management, marked in red, though there is a drop in 2022.

The superannuation corpus in Australia is expected to compound at 5% per year for the next 20 years, but annuities should likely grow by a higher rate, simply because they are more appealing now in a higher interest rate environment than they have been in the past 15 years, and in turn, Challenger should be able to eke out margins compounding at a good clip - in the ~8-12% per year range, which would still be lower than 2009-2018, when it compounded at 15% per annum.

Needless to say, this is a company that is generally well run, well funded, produces profit, allocates capital well, and in no risk of a total failure. It has a brand new leadership that seems to be making the right decisions in general. So, even though the company may not be growing in the recent past as much as we would like, it has the wherewithal to persevere through the phase and then start growing.

Valuation

At A$ 6.06, Challenger Financial trades at roughly 14x 3-year average of normalised OPAT per share (A$ 0.4355), or at roughly 3.8% dividend yield today. It is not blindingly cheap, but neither is it too costly.

I am personally underwater on this investment with an average holding price of $6.65 (after offsetting dividends received), with an IRR loss of 11.75%. Obviously, this is not ideal.

However, leaving aside the past, if the company can get back to its growth path, and start generating profits compounding at 8% or so, while paying out a similar payout ratio as today in dividends, and the stock continues to trade at about 4% dividend yield (none of this is unreasonable), I should still be able to get an IRR return of 9%+, even if I don’t average my costs out. If it so pans out, I should be a happy man.

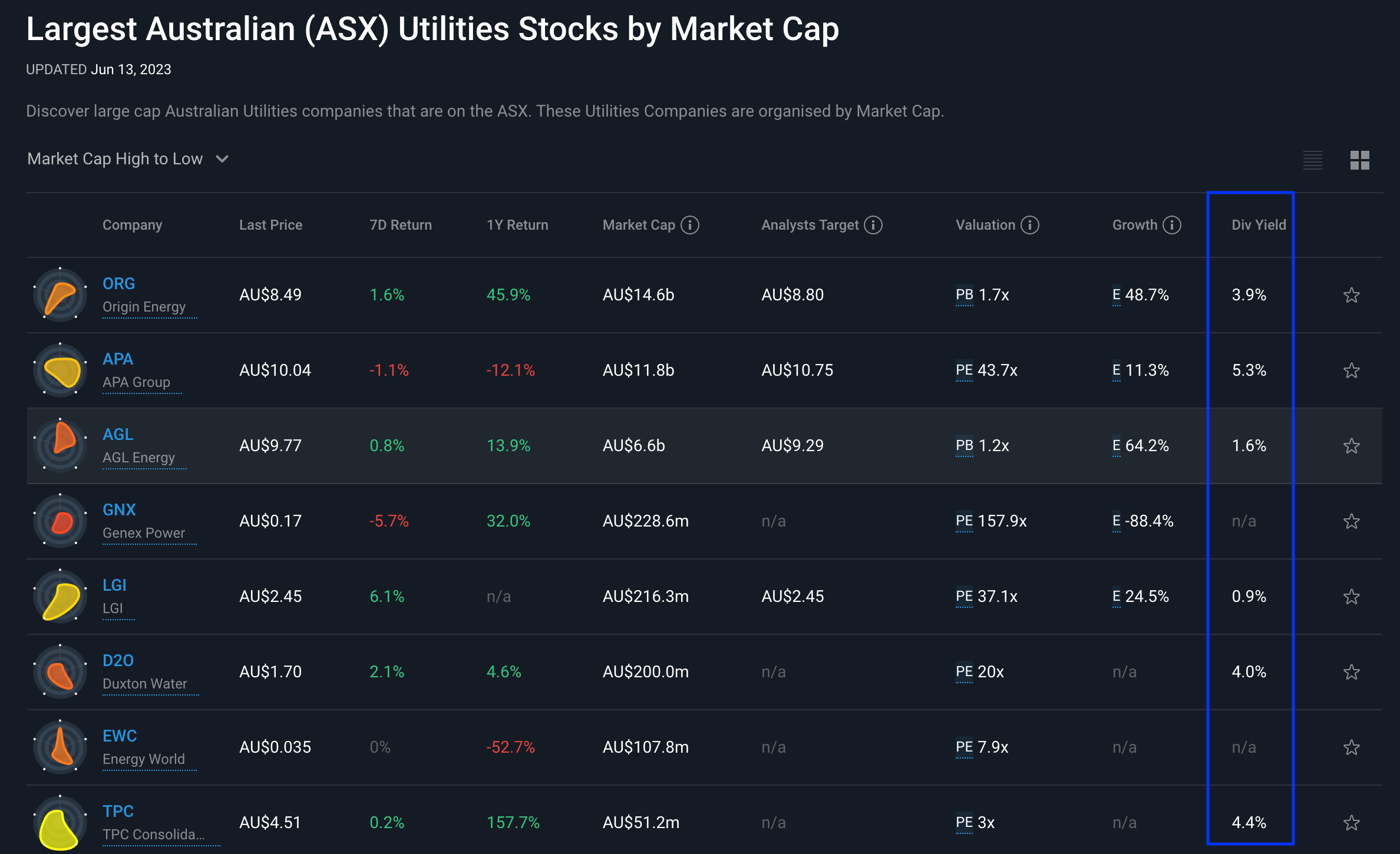

Thinking differently, if the company fails to get back to growth, then the company should likely trade similar to how a utility does, which in Australia trades at roughly 3.9%-5.3% yield range. If the company fails to grow, and just about holds on to its current Normalised OPAT levels and pays out a dividend at current rates, then the downside to the stock is significantly protected, as it already trades at about 4% yield. (Utilities typically pay out a higher ratio of their dividends, roughly 60-80%, while Challenger pays out at 50%, so there is some more buffer built here.)

Turnarounds

Ideally I don’t want to be involved in turnaround story, which Challenger clearly is as of today. However, when faced with drawdowns, it is important to introspect where you find yourself to decide whether or not it make sense to stay invested in a stock. If the story is entirely one of hopelessness, I would just not bother adding to my position and let it dilute out. However, I am nowhere close to that decision with respect to Challenger Financial, with a prospective story similar to Fresenius, where upon studying the facts, I am satisfied that there is hope of future returns.

Summary

Challenger Financial is a well run company with a consistent track record of profit generation, and a past record of consistent growth, that has been rocked by regulatory challenges. The company is rebuilding itself in the new environment, but the vitals are stable and the company is well placed to persevere through this phase back to growth. At current pricing, you are getting a reasonably defensive price point, for the optionality of gaining on the upside if growth takes off, and you are getting a 4% fully franked dividend yield to hold this position.

At this current price, I will likely add to this position in small quantities from time to time. As and when annuities sales start to consistently grow, I might take a larger stake, but for the time being, it is time to carefully proceed.

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

Annuities are financial products that are designed to provide a steady income stream in exchange for an upfront payment or a series of payments. Read more here.

I haven’t looked through this in detail, but I believe this is largely due to regulatory environment. I don’t think they have the choice of being in 100% equities, for instance, even if they wanted.

Given this company’s nature, statutory Operating Profit After Taxes (OPAT) which is what I use generally, can be very noisy, due to the fact that investment outcomes have to be booked on the P&L. Instead, for companies like this, using Normalised OPAT (NPAT in short) is a more useful metric to look at - it is a reflection of the core business health in this case. Similarly, Free Cashflow (FCF) for this company is tough to get at from a normal review of the cash flow statement. FCF is overstated by the normal formula of Operating Cashflow - Net Changes in PPE, but taking all investment cashflows into consideration can throw FCF off too much. For all practical purposes, I look at overall capital adequacy to make sure the company is in good health, which Challenger consistently seems to be in.

Australian companies can “frank” their dividend so the receiver of the dividend don’t have to pay any more taxes on it. Typically, for foreign investors, franked dividends mean no withholding taxes in Australia.

Previous leadership, both at executive and board levels, were very long lasting (18 years and 19 years respectively, if I am not wrong). So, Challenger is conservative when it comes to assignments and support for leadership, which generally bodes well for investors.