Summary Analysis: Brickworks Ltd (ASX:BKW)

An interesting collection of Aussie assets under one roof, with margin of safety

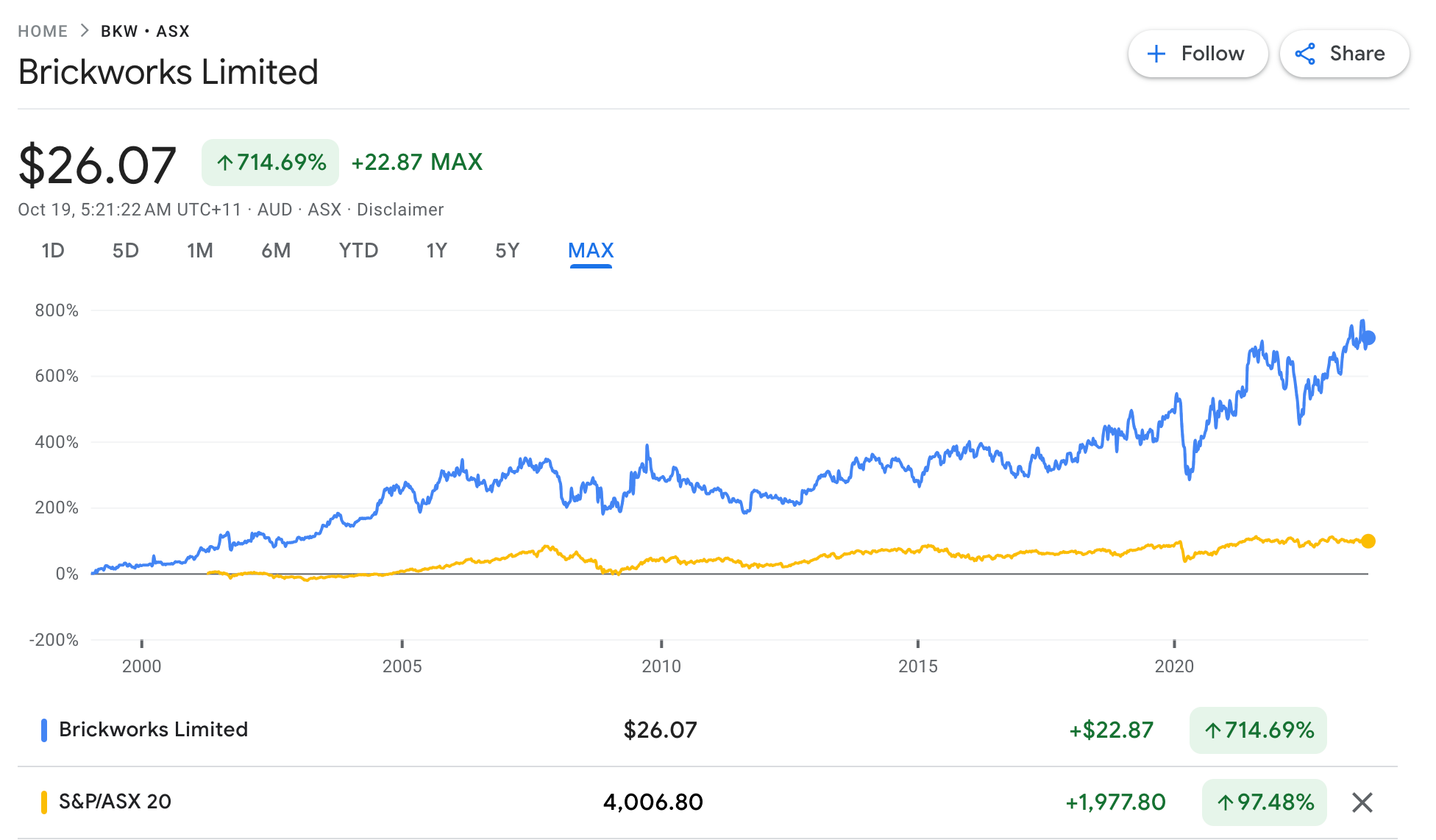

I haven’t written about a company in the portfolio since PetMed Express in early September. Getting company analyses back on track, I am going to cover Brickworks Limited (ASX:BKW) today. Within my portfolio, Brickworks has so far generated a handsome return of 19.7% (AUD basis) / 14.79% (GBP basis) on an annualised basis, currently ranking among the 6th in total returns in my portfolio and has handsomely beaten the market returns over the past multiple years. It is worth taking a look at what the magic is about.

Brickworks is an Australian listed company founded in 1934 to manufacture and supply bricks. It has grown to become a prominent player in the Australian building and construction industry. Brickworks today is a very different company with only a minuscule portion of its value derived from the core business of selling bricks. Through a large cross-holding position in Washington H Soul Pattinson “WHSP” (ASX:SOL) and joint venture holdings in Australian real estate, the company presently serves as a holding company representing interests similar to an Aussie index fund and I would argue a slightly better representation than just loading up on ASX:200. Let’s review the key business segments of this company.

Building Products (Australia + North America)

Let’s get the core business out of the way first - bricks and building products - the smallest part of the company. It generates an EBIT of $66M1 across Australia and US, with Australia bringing in close to 80% of the profits, while the US is where the biggest growth opportunity exists. The company has some strengths here, for instance a superior manufacturing scale and resulting cost advantage, however the brick is facing some headwinds within the construction industry, due to poorer energy efficiency. It is a low margin business with a high cost of capital. Make what you will, but there isn’t anything exciting here2.

This segment of the business will continue to generate some modest results, but I am not holding my breath. In a Sum-of-the-parts (SOTP) calculation, my guess is that this segment will be valued at roughly 5x earnings3. So, chalk it up to $330M.

Property

The company has built out a segment of redeveloping, managing, selling and renting land that is surplus to the core business (i.e. Building Products 👆). This activity is a one-time transfer of assets and capital out of the core buildings business and into the Property segment in order generate cashflow out of otherwise dormant assets. Vast majority of this land sits in the fringes of Sydney and Brisbane, which means rents are not super premium, but they do provide a decent stream of income.

The assets are split across two property trusts - Industrial JV Trust, a 50-50 Joint Venture between Brickworks and Goodman (ASX:GMG), and a much smaller Brickworks Manufacturing Trust. The larger Industrial JV assets holds some $5.8B net worth of property, yielding about $178M per year, or about 3.07% gross yields. However, some $900M of it is undeveloped land, so real yield is closer to 3.63%. To complete the picture, the trusts also hold about $1.2B of loans, serviced at 4.9%, which means, net rental income, after adjusting for interest is closer to 2.6%. This is obviously not a massive yield but it is what it is.

The company routinely updates fair market value of their real estate and adds between $100M-$200M or about 2.5%-5% of NAV in revaluation upside per year, which doesn’t seem to be excessive to me. Leases are signed for long term use with the Weighted Average Lease Expiry (WALE) close to 8 years - there is little or no uncertainty on the cash flows expected from this segment in the medium term, which is good for us.

While the net value of these assets, as carried on the books is ~$2.3B (after taking out the 50% of the partner’s holding in the JV and adjusting for debt), given the low yields on the property, I am inclined to carry this at a much lower value. Let’s chalk this up to $1.5B.

EBIT of this segment over the past 3 years has been $252M, $643M and $506M. At those EBITs, the carrying value we are assigning is in the range of 2.5x-6x, a very conservative band. Cut it whichever way, $1.5B for this segment seems very defensible.

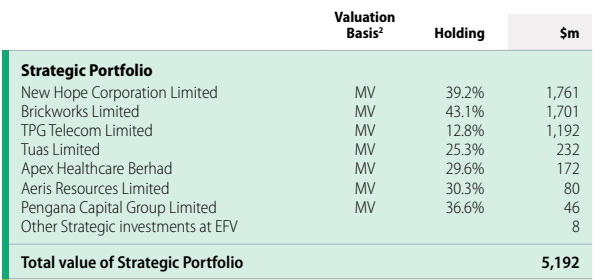

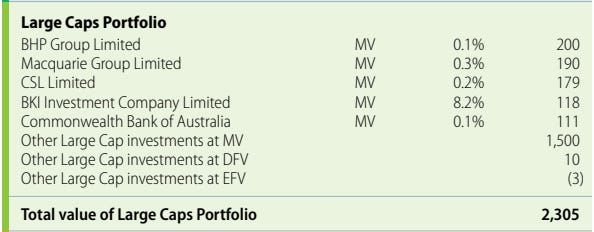

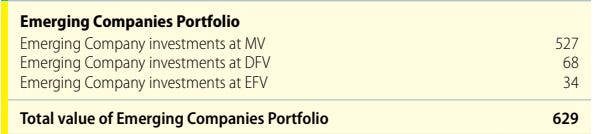

Investments / a.k.a Cross-Holdings

Brickworks holds 94.3M shares in Washington H Saul Pattinson company, shortened to WHSP, but listed on the ASX as SOL. WHSP/ASX:SOL is an investment company that holds a bevy of investments across multiple asset classes - Strategic Holdings, Large Cap equity, Private Equity, Structured Yield, Emerging Companies etc. A full analysis of WHSP/ASX:SOL is outside of the scope of this blog post. However, we need to understand the basics of this asset and assign some value to it.

Founded in 1903 as a chain of 21 pharmacy stores, Washington H Soul Pattinson & Co eventually morphed into an investment holding company. Presently, it holds some $10B of assets across a wide spectrum of assets, generating about 7% of the assets as NPATs through dividends, interests and other forms of gains.

Attentive readers would have seen that WHSP holds Brickworks as one of its strategic holdings - hence the label cross-holdings. Cross-holdings are common in this part of the world, and there is a long standing relationship between the two countries. As a standalone fact, the cross-holdings don’t bother me. I am attracted by the quality and diversification of the rest of the holdings in this portfolio.

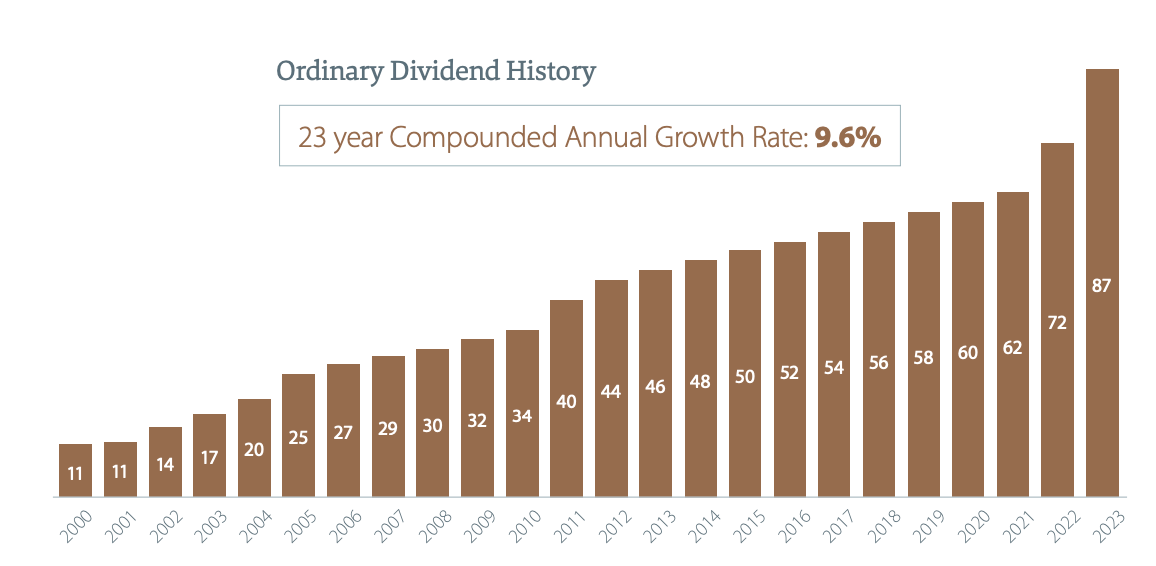

WHSP has been paying out ever increasing dividends for the past 23 years compounding at 9.6%.

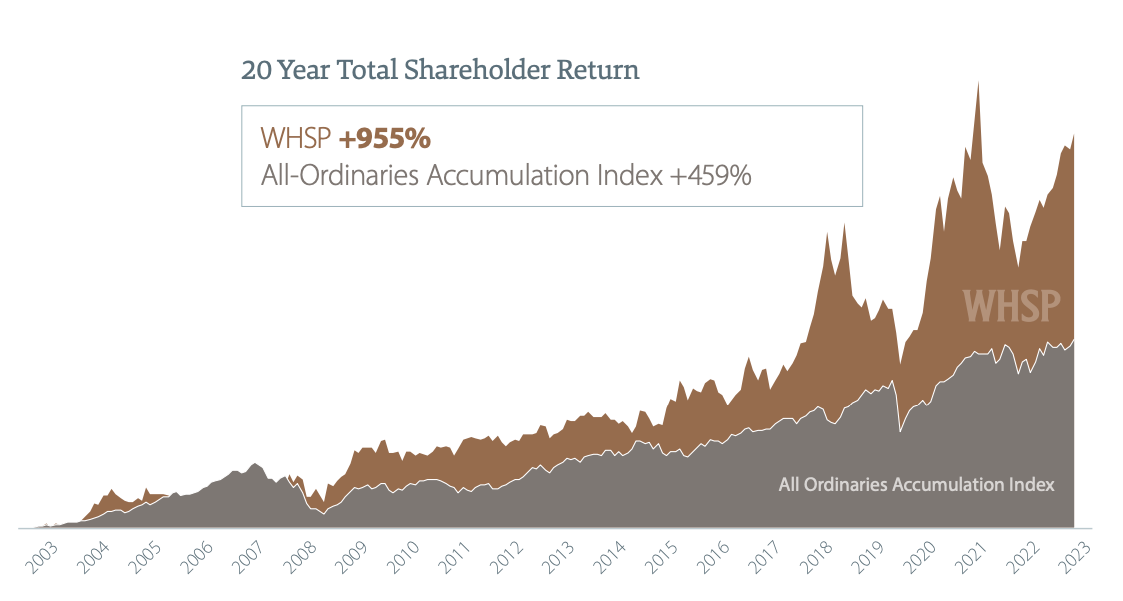

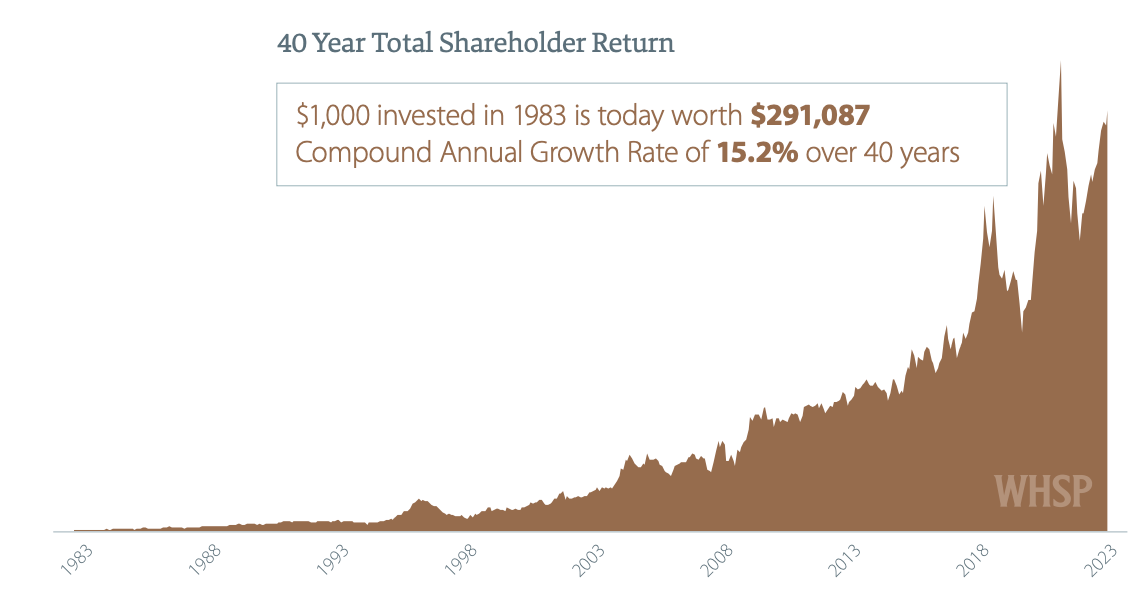

WHSP has beaten the ASX all shares ordinaries over both 20 and 40 year time periods.

As mentioned before, a detailed analysis of WHSP/ASX:SOL, is outside of the scope of this post, but in general, the company looks like a reasonably good proxy for capturing economic growth in Australia, in a possible efficient manner.

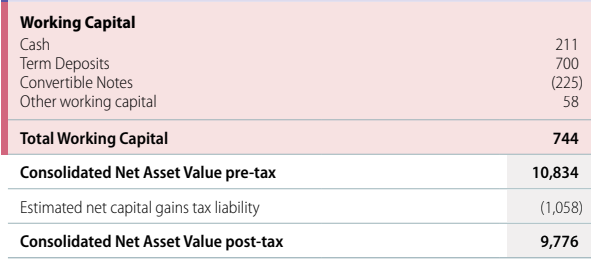

As of July 31, 2023, WHSP/ASX:SOL was valued at $32.95 per share, so the value of the Brickworks holdings is about $3.107Bn. In it’s own latest financial reports, WHSP is carrying net asset value of $9.776bn, which when allocation to the 326.5M outstanding shares, gets us to $29.94 a share of WHSP/ASX:SOL. If we were to take this lower price point, the WHSP/ASX:SOL holdings can be carried at $2.82B.

Even at this lower price point, the business is being chalked up to around 13x-14x. Again, a very defensible price point for the assets in question.

Head Office

As per Brickworks last annual report, head office cost roughly 3% of the EBIT for the group, but it was as high as 5% in 2019 and 2021. Let’s take 5% as a worst case discount to the sum of the parts.

Sum of the Parts

Put it all together and you get: ($330M + $1.5B + $2.82B)*0.95 = $4.417B.

The stock on July 31st (from whence all the above valuations were sourced) was $25.91, or market cap of $3.94bn, a cool 10.8% discount. As you can see we already took some conservative estimates to reaching to this number, so the margin of safety in this calculation is inherently substantial. The stock this week traded at a similar price, so it is as attractive today.

On a conventional basis, the stock now trades at about 8.1x earnings. For a company that has grown its OPAT by 9.5% over the past 15 years, so by that account too, this is an attractive hold.

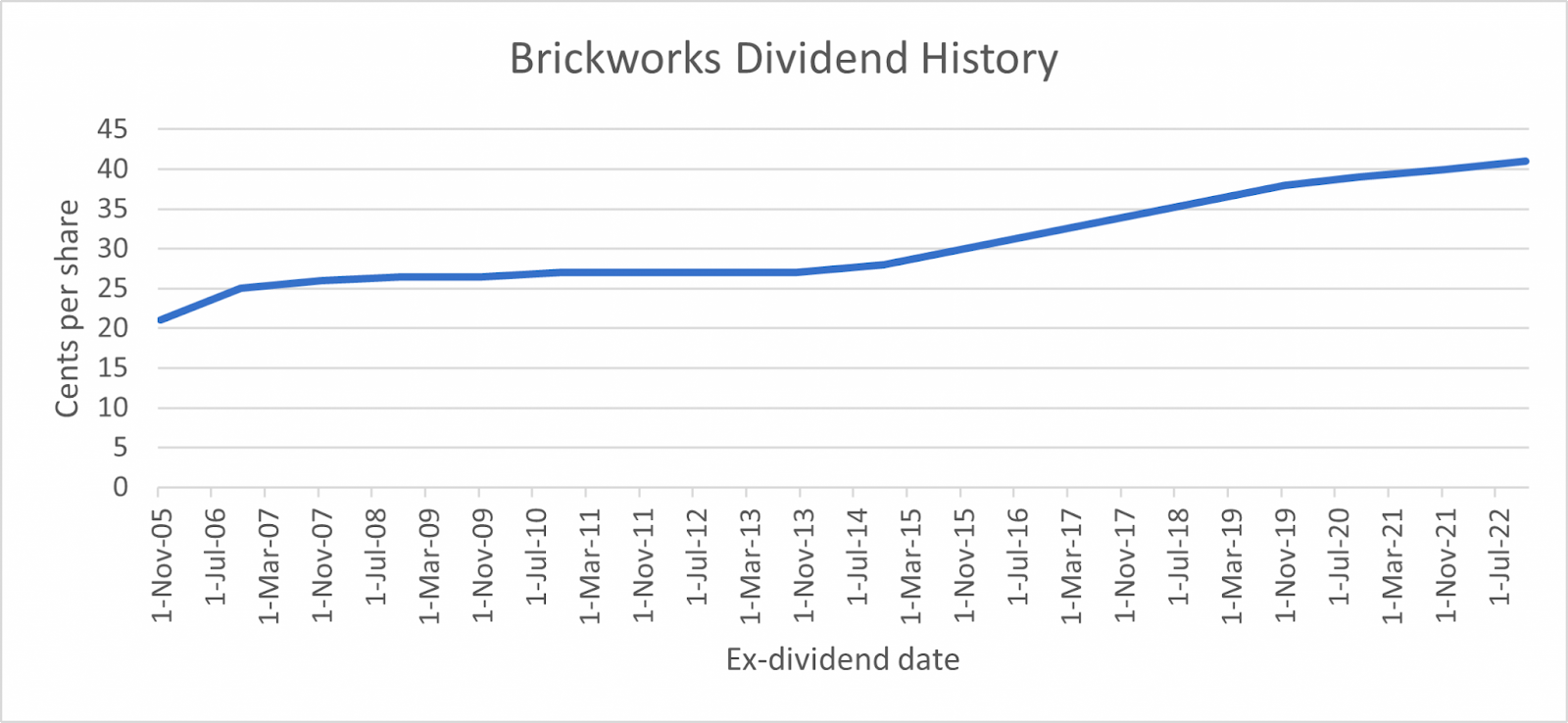

We looked at the consistent dividend track record of WHSp/ASX:SOL, but Brickworks itself is not far behind, having increased its dividend consistently for 15+ years, now returning a fully franked4 $0.65 per share, or about 2.5% yield.

It has not just been dividends that are attractive here. Even total shareholder returns for Brickworks has been pretty impressive over 1 year, 5 years and in the long run.

SOL vs BKW

The natural question is - why not own SOL directly? I wrestled quite a bit between the choices and I like the slightly expanded exposure to property and the small but efficiently run bricks business that we get to carry at a very low multiple with BKW. If however the companies decide to disentangle these cross holdings, then I might have to consider having exposure to SOL itself, but for the time being I am happy with Brickworks as the choice vehicle here.

Risks

Make no mistake - past successes don’t guarantee future success. In terms of risk, it is possible that the portfolio managers at WHSP/ASX:SOL could make terrible mistakes of capital allocation - over-trading is a natural risk of having a bunch of smart people manage money5. It is also possible that Brickworks property assets are knocked down by revaluations well beyond the conservative estimates taken in this post. A bigger risk, however, in my mind is that the market tends to discount conglomerates, something I have seen at play at other positions in my portfolio and is likely to be felt here too. That discount may never close-up, and might likely widen. This means, investors like us, however long term, might not realise the true economic benefits of an upside in the value of the company.

"Beware the investment activity that produces applause; the great moves are usually greeted by yawns." - Warren Buffett

In balance, I am happy taking that risk. This week, I reviewed Brickworks latest annual report (from which I have referenced numbers throughout today’s post) with pleasure and promptly added to my position.

Summary

Putting it together, I believe that Brickworks is a relatively safe long term bet on economic growth in Australia, both through its holdings in WHSP/ASX:SOL as well as through its property holdings in tier-1 cities. As mentioned in the beginning, Brickworks has served well in my portfolio and I intend to continue accumulating this stock.

As always, happy investing!

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

It has done more and it has done less in recent years. However, the latest 2023 number of $66m looks more like an average year than an aberration.

There is a small optionality in this business - if the business can invest in producing the alternatives to bricks and do so at a low cost of capital, then there might be something there, but I am not factoring much of it in the current scenario. Any such positive inflection would be a bonus.

It is a conservative estimate. However, the point of this post is that conservative estimates still add up to something valuable.

Fully franked in Australian terms means that any taxes are paid by the company, so foreign investors like us don’t suffer any withholding taxes.

Latest WHSP Annual report announces “In FY23 we added to our team of portfolio managers” - to be candid, that's not a particular great source of optimism for me. When it comes to investment management, a small number of autonomous capital allocators are going to likely outperform decisions by committee, is my humble opinion on the matter.