Summary Analysis: Alibaba (HKG:9988 / NYSE:BABA)

Reviewing an old holding

Alibaba (HKG:9988 / NYSE:BABA) has been a core holding of the Coffee Can Portfolio since the portfolio’s inception. With some recent run-up, and the subsequent volatility in the stock, it seemed like a good time to review it.

Alibaba Group was founded in 1999 in Hangzhou by Jack Ma and a small group of entrepreneurs as a B2B online marketplace connecting Chinese manufacturers with global buyers. Over the next decade, it expanded into consumer e-commerce (Taobao, Tmall), digital payments (Alipay, later spun into Ant Group), and cloud computing. Alibaba first went public on the Hong Kong Stock Exchange in 2007, listing its B2B arm, but delisted in 20121 after buying back shares from Yahoo to consolidate ownership. In 2014, it completed what was then the world’s largest IPO on the New York Stock Exchange, raising $25 billion. In 2019, Alibaba relisted in Hong Kong through a secondary listing, partly as a hedge against US–China geopolitical tension.

It would be remiss not to talk about its founder, Jack Ma, once celebrated for his outspoken charisma and advocacy for private enterprise, but now largely withdrawn from public view after his critical 2020 speech about China’s financial regulators. That episode, followed by the suspension of Ant Group’s IPO and a broader regulatory crackdown on the Chinese tech sector, marked a turning point.

Ma’s retreat (Wu Yongming is current CEO) coincided with a period of subdued corporate ambition and internal restructuring, as Alibaba shifted from aggressive expansion toward operational efficiency and governance realignment. All that said, Alibaba today presents one of the more interesting valuation puzzles in global tech - a company that is simultaneously mature, cash-generative, and yet priced like a value stock.

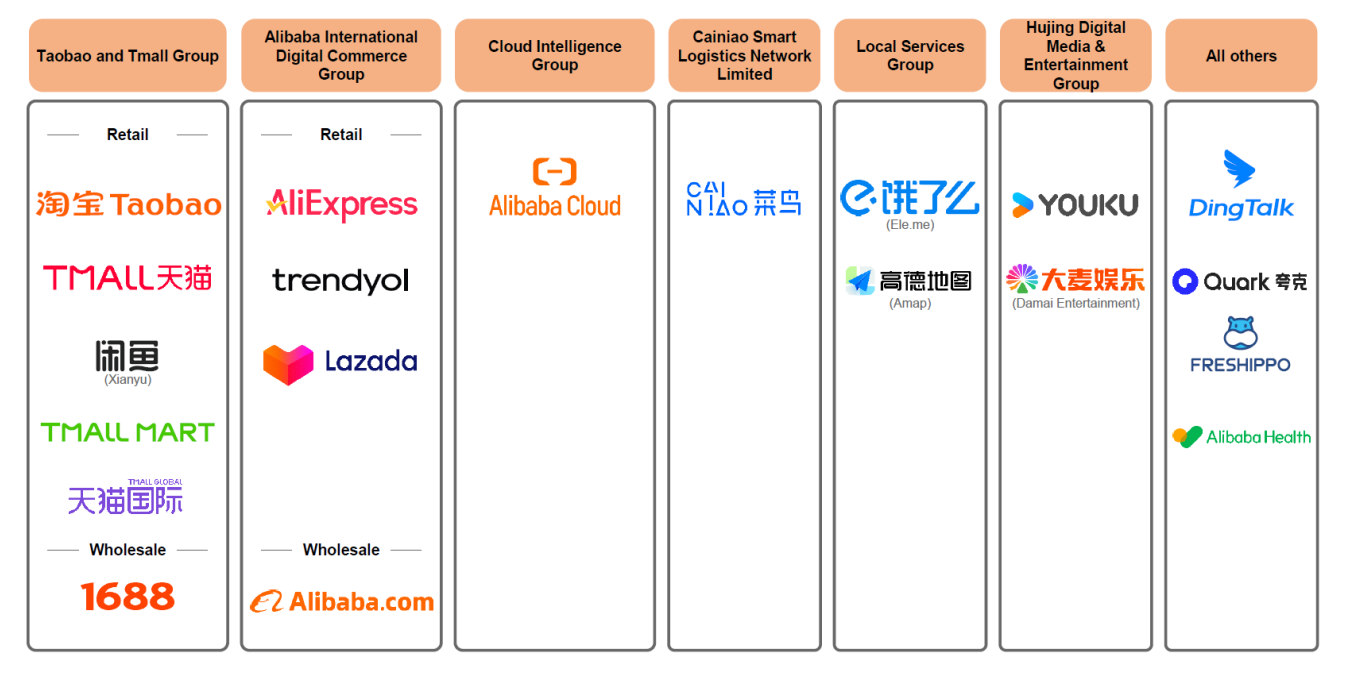

Business Mix

Alibaba today operates as a diversified technology conglomerate spanning e-commerce, cloud computing, logistics, digital media, and innovation ventures. Its core remains China commerce - platforms like Taobao and Tmall - which together account for about 43% of total revenue and generate the vast majority of Alibaba’s operating profit through merchant advertising, commissions, and services.

The international commerce segment (including AliExpress, Lazada, Trendyol, and Daraz) contributes roughly 11% of revenue, though margins here are thinner as the company invests in global expansion. The Cloud Intelligence Group, encompassing Alibaba Cloud and AI services, now represents around 12% of revenue and is rapidly growing, with improving profitability as AI-related demand rises. Supporting these are Cainiao, its logistics arm, and Local Services & Digital Media (Amap, Youku, Alibaba Pictures), which provide additional revenue streams but contribute modestly to group EBITDA. Overall, Alibaba’s earnings mix remains anchored in its domestic e-commerce engine, with Cloud and AI emerging as the next meaningful profit drivers.

Financials

Earnings power has been quietly strengthening. In USD terms (for fiscal years ending March 31), Alibaba’s EPS has steadily grown from $3.63 in FY22 to $4.03 in FY23, $4.38 in FY24, and an impressive $7.60 in FY25. The most recent quarter (Q1 FY26, ending June 2025) printed $2.59 EPS, nearly double the year-ago period - suggesting the business could sustain $8 per share annually as the baseline it once had and built forth from there.

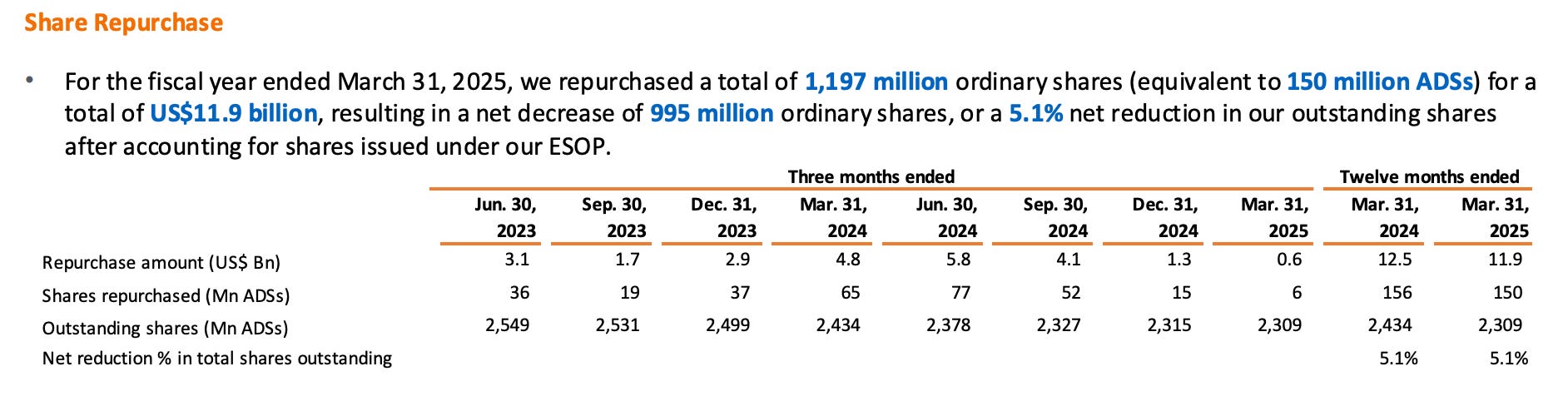

Cash generation tells a similar story. Free cash flow has ranged between $21–29 billion over the past four years, with FY25 at $22 billion. At first glance, retained earnings have been flat for several years, which seems puzzling given strong profitability. The explanation likely lies in capital returns: in FY25 alone, Alibaba repurchased $11.9 billion worth of shares (about 5% of outstanding shares) and initiated dividends, paying roughly $4.66 per ADR across 2024–2025 (~1% yield). Combined, buybacks and dividends equate to a 6% shareholder yield—a meaningful return for long-term holders even before accounting for price appreciation.

Investments

For years, Alibaba made few large capital investments in its core retail business. That appears to be changing. FY25 saw investments going more and more towards AI - a $52 billion AI investment plan over the next three years. Relative to U.S. tech giants—who are collectively spending $400 billion this year and nearly $1 trillion by 2026—Alibaba’s figure seems small. Yet, that may be precisely the point. Where U.S. peers risk over-investing and eroding returns on capital, Alibaba’s approach is conservative and cashflow-backed, unlikely to strain its balance sheet.

AI revenue base - teased out to be ~USD 3.4Bn / 2.4% per year - continues growing at ~100% YoY, the investments could effectively self-fund through expansion. In many ways, this represents a more prudent path: a measured AI buildout supported by domestic demand and policy alignment. Chinese enterprises are likely to prefer (or be encouraged to adopt) local AI technologies, reducing the need for capital-intensive global scale. In such an environment, Alibaba’s model—profitable, domestically focused, and sustainably financed—may prove superior to the “bet-the-ranch” strategies of its Western counterparts.

Valuation & Thesis

If your investment thesis centers on Alibaba as a stable, cash-generative e-commerce leader with optional upside from its Cloud and AI businesses, the stock presents a compelling long-term opportunity. The company’s core commerce platforms—Taobao, Tmall, and related retail ecosystems—continue to generate over $20 billion in free cash flow annually, even amid China’s uneven macro backdrop.

This steady engine funds a disciplined capital return program, combining meaningful buybacks (5% of shares in FY25) with a growing dividend—together providing a 6% yield that’s rare among large-cap tech firms. Its balance sheet remains robust, leaving ample room for AI and cloud reinvestment without compromising shareholder returns.

The real optionality lies in Alibaba’s Cloud Intelligence and AI divisions, which are scaling rapidly and showing early signs of operating leverage. Cloud revenue now makes up roughly 12% of total sales, with AI-driven products contributing over 20% of external cloud revenue and growing at triple-digit rates. As Chinese enterprises and institutions accelerate digital and AI adoption, Alibaba stands well-positioned to capture a significant share of that spend. If Cloud and AI continue compounding at current rates while margins improve, these segments could meaningfully lift group profitability and valuation multiples over the coming years. In essence, investors today are buying a proven e-commerce cash machine—with a free option on China’s AI and cloud transformation.

On a market cap of roughly $420 billion, Alibaba trades at about 20x PE or 21x FCF - hardly expensive for a business of this scale and profitability. For comparison, the US tech sector represented by QQQ trades at about 35x earnings. I know it is not an apples-to-apples2 comparison, with Alibaba’s TAM restricted by Chinese geography, but still, the valuation gap is noteworthy, relative to its cashflow strength, capital discipline, and reinvestment potential.

The flipside, of course, is regulatory and geopolitical risk. The Chinese government retains significant influence over strategic sectors and could choose to favor alternative platforms or policies that constrain growth. This ever-present uncertainty is why I’ve always taken a basket approach to China exposure—diversified across companies and themes rather than concentrated in a single name.

In essence, Alibaba is no longer the hyper-growth story it once was, but it’s evolving into a steady compounder—anchored by resilient cashflows, disciplined capital returns, and credible optionality in AI and Cloud. For investors comfortable with China risk, it still deserves consideration as a core long-term holding.

With that thought, happy investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.

Totally useless facts: I made a bunch of money from that delisting. Investors marked up the stock massively as soon as the announcement was made.

Pun unintended