Summary Analysis: Lenovo (HKG:0992)

Reasonably priced hardware manufacturer

Today’s post is going to talk about Lenovo (HKG:0992). It is a relatively well known brand and there is ample literature on this company, so I will keep it brief.

Nb: Please note that this company trades in Hong Kong as HKG:0992 in Hong Kong Dollars (HKD) and in US markets as OTCMKTS:LNVGY, which are units in an ADR. There are 20 Hong Kong shares for each ADR. To complicate things, the company declares its financials in US Dollars. So all numbers mentioned below are in USD (including the per-share data). However, to calculate the earnings yield, I have converted the per-share data into HKD before computing. If you plan to hold LNVGY, then you must multiply per-share numbers by 20x before computing multiples and yields. Apologies for the confusion. It is what it is.

Lenovo is a multinational technology company that designs, manufactures, and sells a wide range of products, including personal computers, laptops, tablets, smartphones, servers, and other electronic devices. The company was founded in Beijing, China, in 1984 as Legend and later rebranded as Lenovo in 2003. Lenovo has grown to become one of the world's largest personal computer vendors by market share.

Lenovo has been a publicly traded company from 1994, but became popular as global name only after they purchased IBM’s “Think” brand and the personal computers division. Since then, Lenovo has acquired the remainder of IBM’s x86 server lines in 2014. Lenovo has a good history of establishing joint ventures with NEC, Fujitsu and EMC to launch products to expand the range of what they sell.

As it stands today, Lenovo sells hardware products such as personal computers, workstations, servers, storage, smart televisions, and mobile products such as smartphones & tablets, clubbed into a business group called Intelligent Devices Group (IDG). It also has 2 other business groups called Solutions and Services Group (SSG) and Infrastructure Solutions Group (ISG).

The ISG and SSG groups are small, but are becoming a growing part of revenue, with only $5.9Bn (13%) coming from this (then called Datacenter Group [DCG] & Others) in 2018 to about $15Bn (25%) in 2023’s print. In 2018, these divisions were booking operating losses of about 6%, whereas today, they are booking operating profits of 9%, with SSG already significantly profitable at close to 20% operating margin.

In effect, we have a small, but healthily growing set of businesses who are gaining a lot of operating leverage and are likely to be profit drivers in the future. We will come back to this later.

The core of the business today is packed in the Intelligent Devices Group (IDG), which is what we retail consumers know Lenovo the most for. This is not a massively growing business. It has grown from about $39Bn in revenue 5 years ago to about $47Bn today. It had a big pandemic-time boost in 2022 sales (covering revenue from 2021 July to 2022 June) but sales is slowly settling down to pre-pandemic trend.

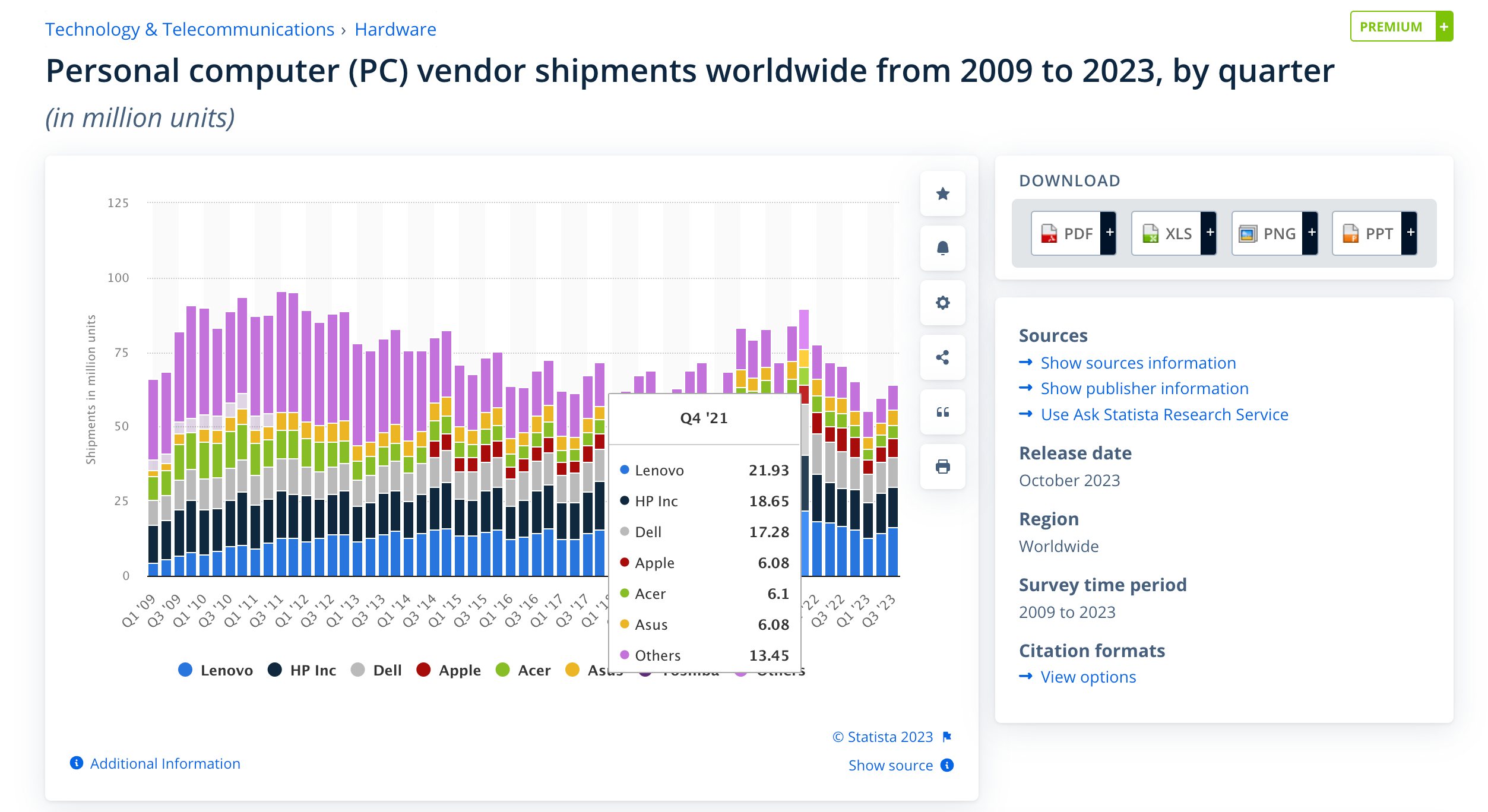

In fact, this trend is hardly isolated to Lenovo. All the major device manufacturers faced similar trend - Global shipments of PCs seem to be settling down into a stable state now, with some cyclicality as pandemic boosted purchases, but the comparables are now lagging behind.

While this trend has not been charitable to the industry as a whole, Lenovo has benefited from (a) increasing its market-share, now close to about 24% of all shipments, and (b) benefitting from selling non-PC devices, such as mobile phones, tablets and the like.

The collective effort of the changing but productive mix of revenue generators has been largely positive, moving revenue from $16Bn in 2008 to about $61Bn in 2023, compounding at 9.3% per year. EPS has accordingly grown from about USD 0.0486 to about USD 0.1274. The company has a culture of paying out its profits as dividends, paying out some 56% of its profits over the past 15 years as dividends.

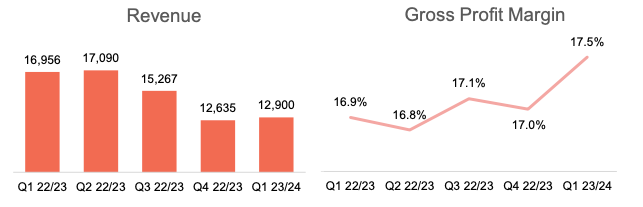

Notwithstanding the past, the company continues to face revenue challenges, printing another YoY decline in the latest quarterly results, though it is sequentially recovering.

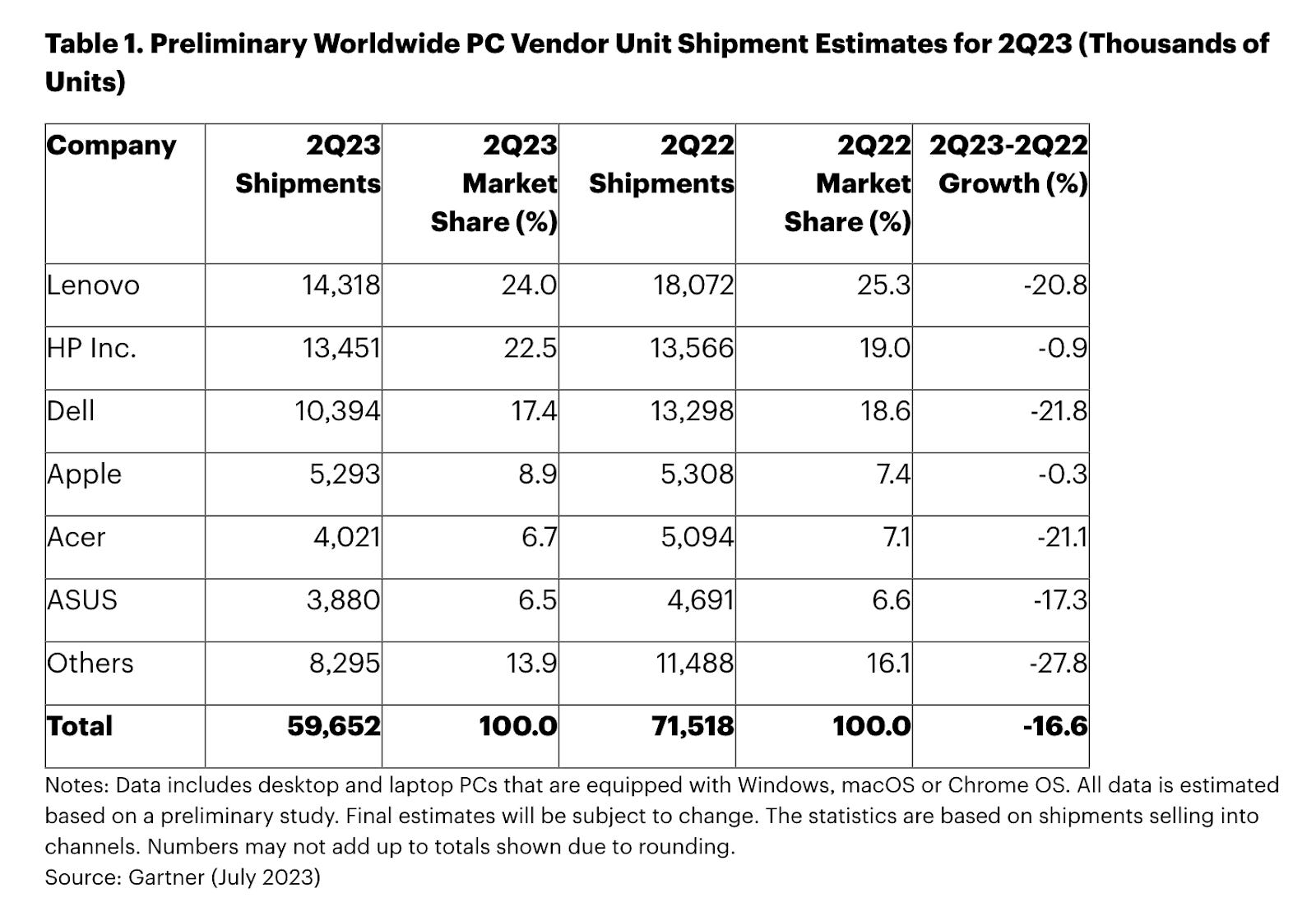

More important than the absolute numbers is the marginal decline in the PC marketshare from 25.3% in Q2’22 to 24% in Q3’23, with most of the differential going to HP Inc, though Apple has gained too.

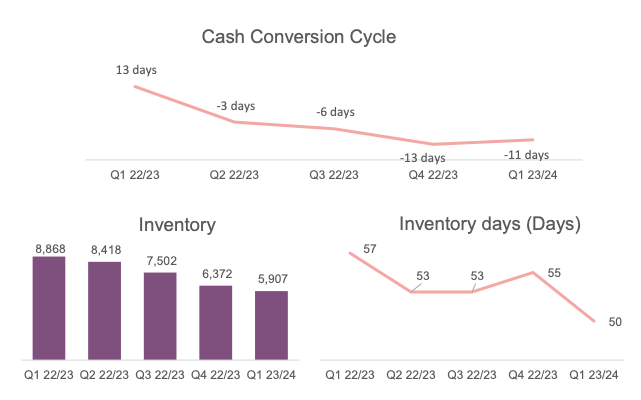

Internally, however, the business is well run, with a stable management both in terms of tenure as well as tactical performance. See cash and inventory management over the past 5 quarters, all of which are trending in the right direction, with margin also improving (graph above).

So despite the challenges in its core business, between its tactical improvements and small but growing parallel business units, there is enough to keep investors interested.

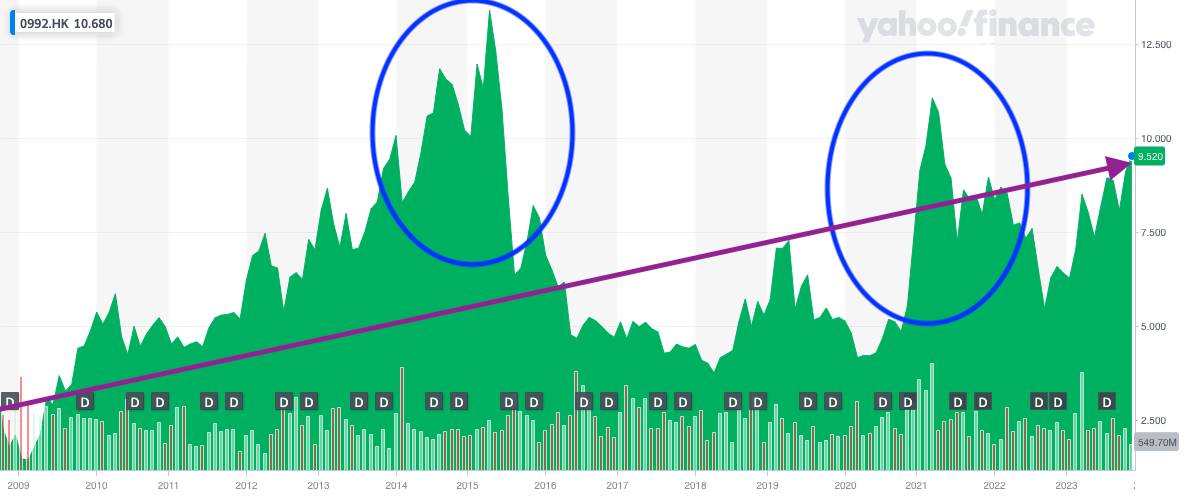

At face value, it seems like a relatively staid business that sells low-margin hardware at volumes, generates some profits, and remits a good portion of those profits off to shareholders from time to time. So, I would expect this to behave more or less like a FMCG or a Utility. Interestingly though, Lenovo behaves a lot more erratically when it comes to trading on the bourses. It has the tendency to be treated like a “tech” stock and be taken to stratosphere from time to time, but then brought down, with some overcorrection, to FMCG like valuations at other times.

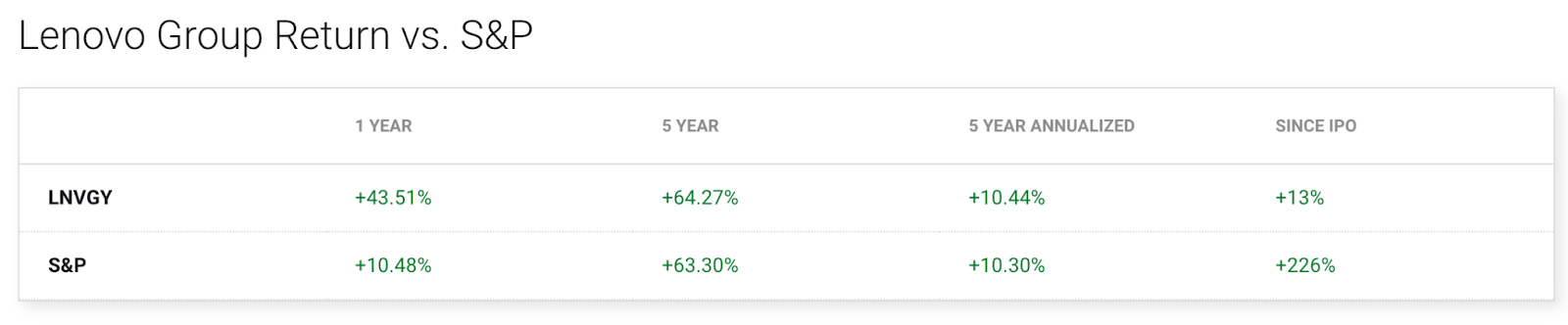

Nevertheless, the returns on the stock has been profitable for patient investors.

Even in my portfolio, it has a compounded well and is the 3rd best performing stock. The upside is partly attributed to the consistency of the company earnings and partly to acquiring the stock when trades more in line (or under) the long term trend line1.

As it stands today, in 2023 financial statements, it has printed USD 0.1274 in diluted EPS and generated about USD 0.13 in Free Cash Flow per share. After forex conversions, that works out to be ~10.5% earnings yield and ~10.7% FCF yield.

Remember that the business is currently declining in revenue (24% YoY) and EPS (-64%). In the worst case, EPS could be as low as 0.0572 but as the business improves, analysts estimate that the EPS in 2023/24 will be closer to 0.0905 or closer to 7.5% earnings yield or 13.3X P/E2. These same analysts expect the EPS to improve to USD 0.1575 by 2025-26, which if it happens, would put today’s purchases in the “win” category. Not blindingly cheap but not excessively expensive.

My current average price is HKD 7.4 and the stock trades at HKD 9.5 today. I will continue to add to my position from time to time.

💡Pro Tip: If you have experience trading options, then the Jun’24 HKD 9.25 PUTs are trading at ~ HKD 0.96. You can possibly pocket a neat 10% over 7+ months by underwriting these. Even if the options are exercised, given that Lenovo’s final dividend ex-date is roughly end of July and it is expected to be around HKD 0.30 per share, you are acquiring it for the long run at a net price of HKD 8.0, a neat 15% lower than today’s price. Not bad. Please note the additional risks of options trading and a large contract size of 2000. (ps: I just sold some PUT options this week.)

As always happy investing!

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility for your actions. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

This is generally good advice for acquiring the stock of any company.

These analysts expectations are not outlandish. I largely concur.