Rethinking the Pension Default

A simple global tracker often beats the elaborate portfolio you never asked for

Some time ago, I wrote about how the default pension portfolio lovingly picked by your employer is often about as useful for long term returns as an umbrella during Chennai’s Cyclone season.

To quote myself:

Pension providers have a fiduciary duty to keep your money “safe”. To achieve this, they often promote highly diversified, low-volatility funds to minimise risk. The default funds they recommend to HR are usually on the conservative end of the investment spectrum. There’s no malice here. HR approves providers who meet these criteria, and pension providers act responsibly to protect your funds.

But here’s the catch: Your pension might not be working as hard as it could.

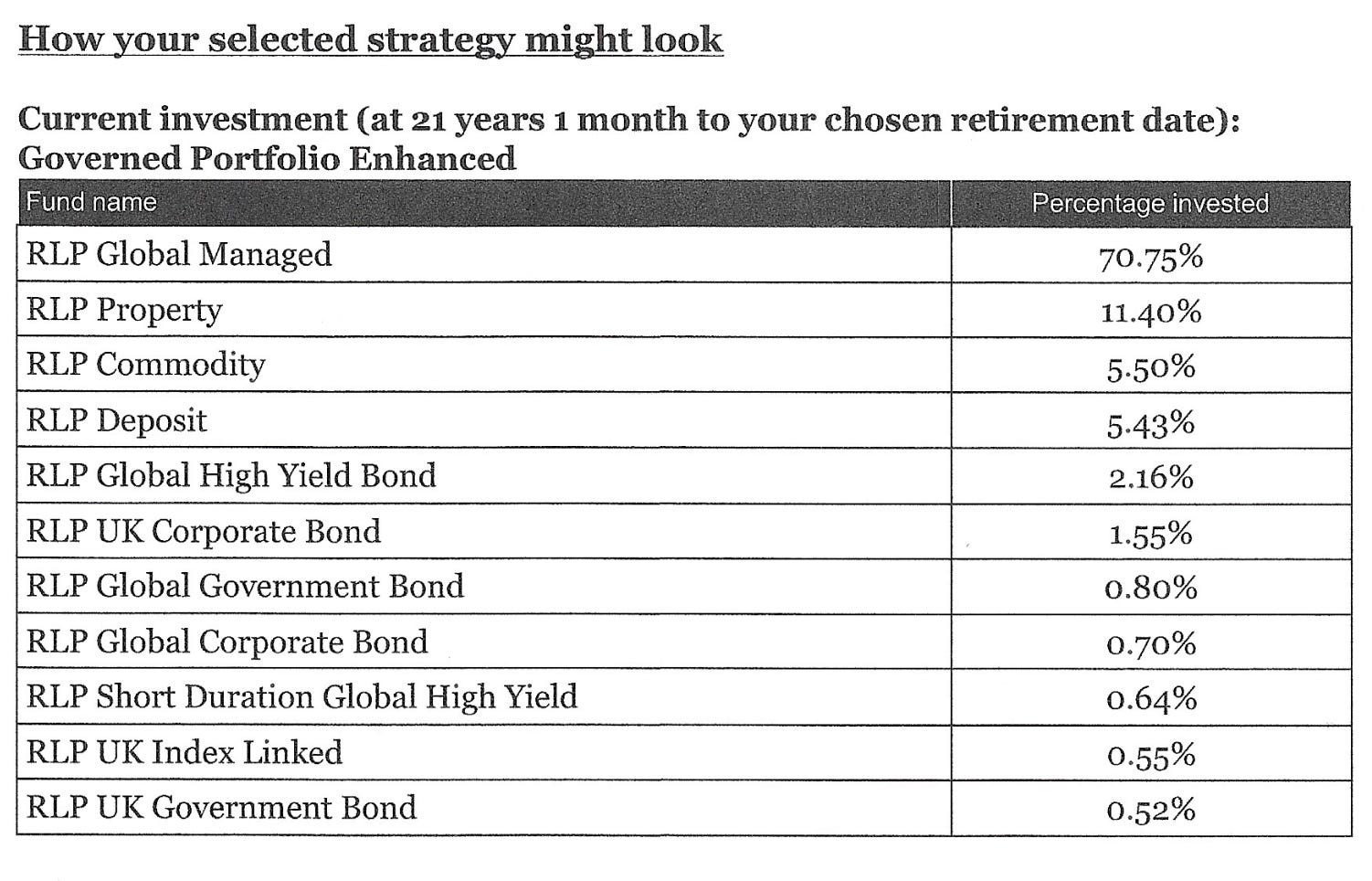

If my previous example was not convincing enough, allow me to present Exhibit B. Earlier this year, I switched jobs for the first time since moving to the UK. My new employer provides pensions through Royal London. Their default configuration for me looked like this:

As you can see, about 30 percent of the portfolio was a cheerful assortment of Property, Bonds, Commodities and even a Cash bucket that goes by the dramatic name of “RLP Deposit”. For some people, this might be comforting. For me, it looks like dead weight. Unleveraged property and bonds simply do not deliver the long term returns that equities do, and the opportunity cost compounds over time.

But what about volatility? After all, bonds are supposed to soothe the nerves during market downturns. Fair point, and bonds have their place. However, if bonds are meant to protect me from selling equities during a slump, then they belong in the pot of money I might actually need within the next three to five years. My pension sits firmly outside that category. Between savings accounts and ISAs, I already hold a sensible cushion of cash and bonds covering several1 months of expenses.

Redirecting pension money into bonds when I am more than a decade away from even early access makes very little sense to me.

So yes, collectively the roughly 30 percent allocated to these non-equity assets does not inspire confidence. What about the equity portion then? Surely the RLP Global Managed fund is a hardworking equity engine. Sadly, no.

Over the past ten years, the RLP Global Managed fund delivered 9.29 percent a year. A simple world tracker delivered 10.69 percent before dividends and about 12.29 percent with dividends included. That is a yearly gap of about three percentage points. Over a decade, the difference compounds into something you would notice on your pension statement2.

Even if I assume the rest of the portfolio managed something around 4 percent, the combined weighted return sits near 7.7 percent. That is well below what a straightforward global equity tracker would have produced during the same period.

Now yes, equity markets have performed unusually well in the past thirteen years3 and long term averages are typically lower. Even so, 70 percent of this Royal London portfolio sits in an equity fund that has already underperformed. When equities eventually revert to the mean, the odds of this combination catching up through property, commodities and cash are slender. Bonds might rally, but given their single-digit representation, it hardly moves the needle.

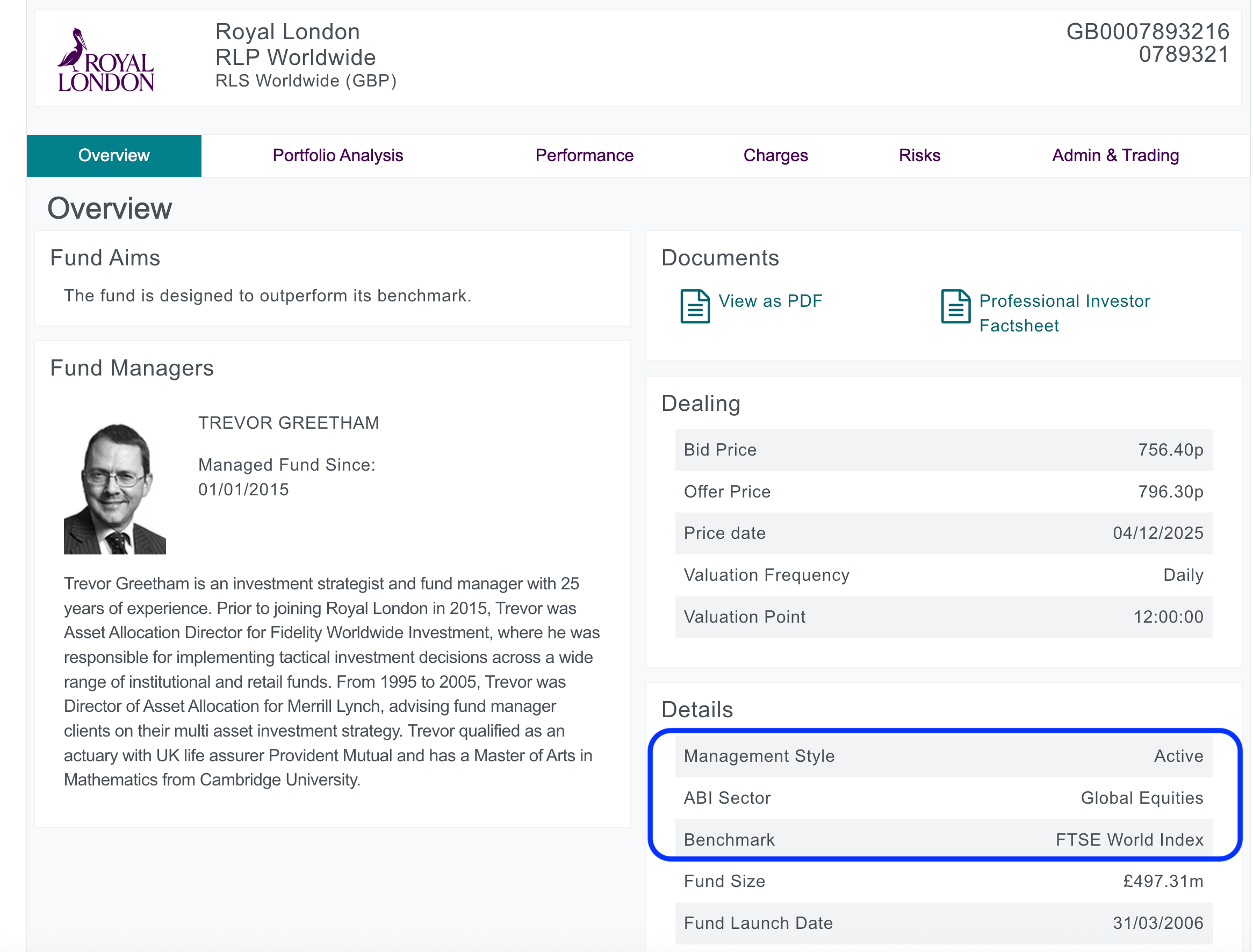

At this point, I was unconvinced that this was a good trade-off. So I went looking. After a bit of rummaging through Royal London’s investor site, I discovered an interestingly named alternative: RLP Worldwide.

Their unassuming style and the promise of “Active” investing aside, it is simply their version of a global equity tracker.

Their five year performance chart4 practically sits on top of Vanguard’s world tracker (LON:VWRP, the accumulation version), which is exactly what one hopes from a tracker. Royal London’s investor portal is slightly clunky and feels as if it was last updated around the time floppy disks were still a thing. However, after a bit of persuasion, I managed to move my entire pension pot, old and new, into this fund.

To be clear, such equity concentration is not ideal for everyone. Risk appetites vary, time horizons differ and some investors sleep better knowing they hold bonds and property. But if you do prefer a clean, equity-heavy approach for long term pension accumulation, this option makes far more sense than the smorgasbord5 I started with.

On that note, Happy Investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.

Generally targeted at 6 months of expenses, which is about 2-2.5 months of pre-tax income. I got to confess, though, that I have been under that number many times, but at least all of 2025, I have maintained that much in cash - in fact, my cash pile was at all time high earlier in the year, but have slowly been allocating it away this year.

So much so, that the out-performance could just pay off the newly introduced Inheritance Tax on pensions that was announced in UK’s 2024 budget.

2012 was roughly when equities shrugged off the 2008 induced slump and have since been on an absolute tear.

LON:VWRP, the accumulation version of the Vanguard global tracker, in GBP, hasn’t been around for 10 years, and hence I couldn’t put a longer chart, but basic comparison to the non-accumulation version, i.e. dividend-paying, tells me a very similar story.

A word I only learnt during the just-concluded UK Budget season.