Is Your Pension Working Hard Enough?

Why default funds might be holding you back—and what you can do about it

It’s been a while since I last attended to this blog. Life’s been busy. I’ve been channeling some of my creative energy into LinkedIn, and my work life has been demanding—particularly during a recent reorg, which needed my full attention. While I plan to resuscitate this blog, don’t expect the frequency of posts to be what it once was.

Let’s Talk About Pensions

In the UK, the default pension deduction for most employees is 3-4%, matched by another 4-5% from the employer. That means for many of us, 8% of our monthly income is automatically set aside for retirement—money that we won’t touch for decades.

Pensions are a uniquely powerful tool in your retirement kit. They offer a trifecta of benefits:

Massive tax advantages – Contributions are tax-deductible, some withdrawals are tax-free, and retirement often involves a lower marginal tax rate1.

Forced long-term savings – You can’t access these funds until a minimum retirement age (currently 55 for SIPPs2).

Compound growth over time – The longer the money stays invested, the more it can grow, unencumbered by taxes on gains and dividends.

Given these features, pensions are an outsized factor in most UK residents’ retirement planning. How much we contribute, how efficiently we handle taxes on contributions and withdrawals, and the performance of our investments can significantly impact our long-term financial security.

The Case for Examining Pension Investments

Most employers in the UK partner with pension providers that are great at handling payroll logistics. Their "customer" is typically the HR team making procurement decisions3—not you.

Pension providers have a fiduciary duty to keep your money "safe." To achieve this, they often promote highly diversified, low-volatility funds to minimize risk. The default funds they recommend to HR are usually on the conservative end of the investment spectrum. There's no malice here—HR approves providers who meet these criteria, and pension providers act responsibly to protect your funds.

But here’s the catch: Your pension might not be working as hard as it could.

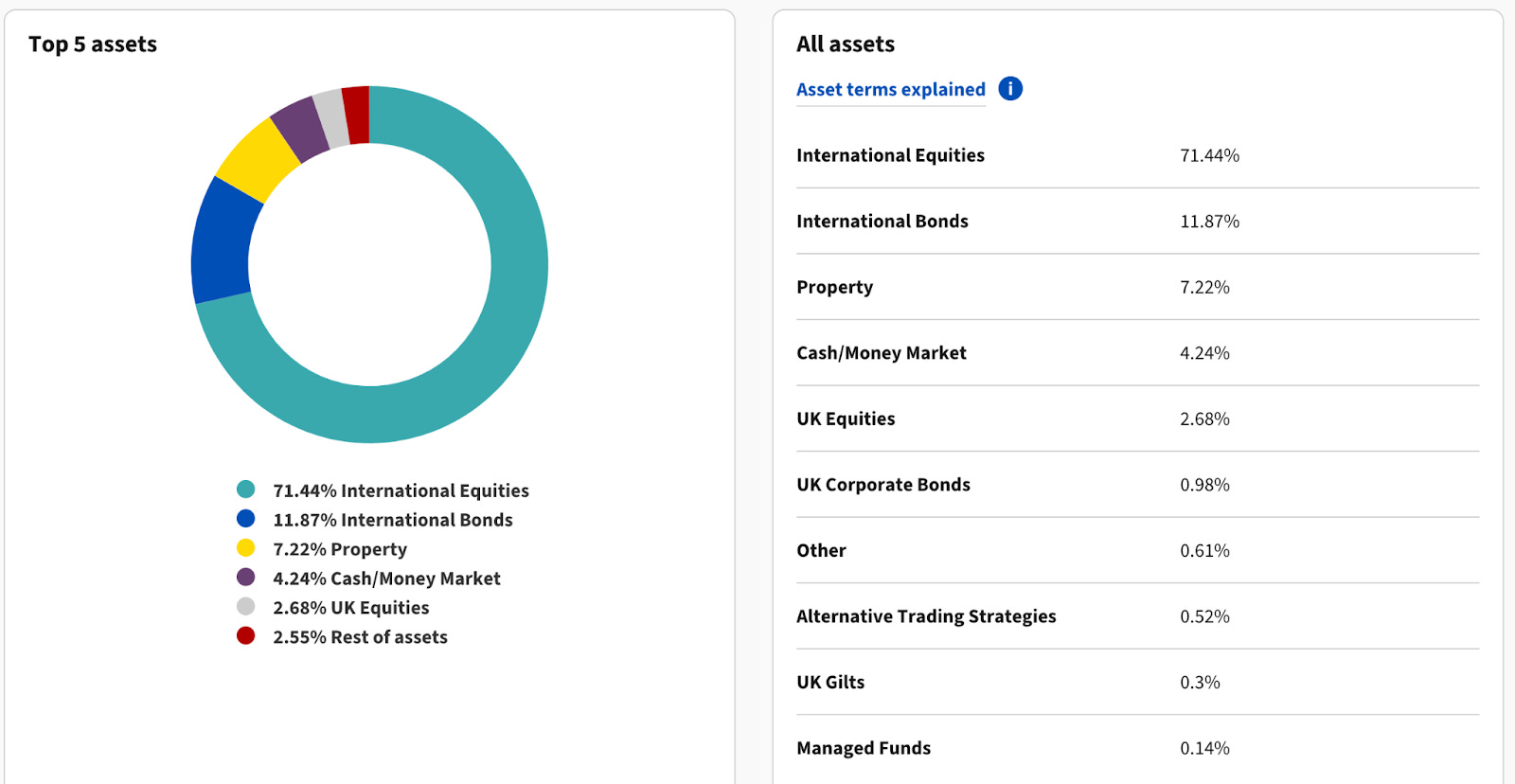

Take my case as an example. My employer uses Aviva as its pension provider, and the default fund is the “Aviva Pensions My Future Focus Growth S6.” It employs a lifestage investing approach. At first glance, its asset allocation seems reasonable, leaning toward securities but with a substantial allocation to bonds, property, and cash (~24–25%).

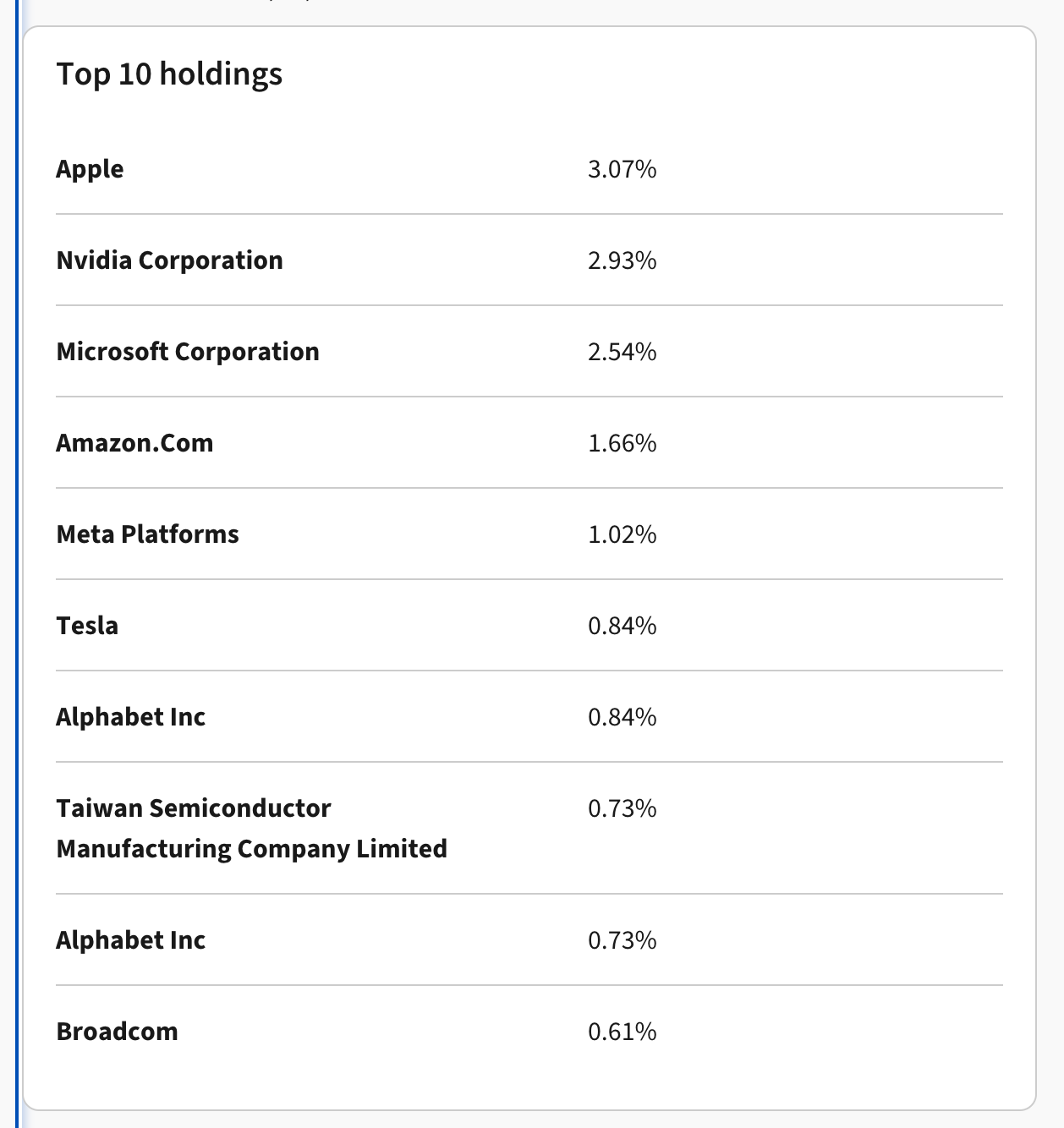

Its top 10 holdings include the usual market giants, but their cumulative weight (15.97%) is slightly lower than that of a global tracker fund’s top 10 (18.73%).

Here’s the issue: Performance.

Over the last 12 months, this fund delivered a return of 19.25%, compared to 25% for a global tracker.

Based on my contributions, my fund’s total return was 7.01%, while a global tracker achieved 11.87%.

There is also the small matter of fees. Pension providers who work with payroll will typically extract a little bit more in fees that providers who aren’t payroll friendly. After all the technology and investments to make it easy for payroll to work with, needs to be paid for. The performance gap is far too wide to be explained by mere fees, but is probably a contributing factor.

I’m not suggesting malice or incompetence. Maybe investing less in the top 10 holdings is smart. Perhaps the lifestage approach is sound. But when your pension is one of the largest, most illiquid parts of your financial plan, shouldn’t it be working harder?

What Can You Do?

Fortunately, UK pension rules offer flexibility. While your employer might stick with a single provider for simplicity, you have options:

Choose a better fund within your provider. Look for one that aligns more closely with your investment goals.

Transfer to a SIPP. Take control by moving your pension to a Self-Invested Personal Pension, where you decide how it’s invested.

Stay the course. If the default fund aligns with your strategy, great! Pour yourself a pint and relax.

The key is to look under the hood and ensure your pension works for you. Whether you adjust, transfer, or stick with your current setup, make sure your choices are deliberate.

UK is becoming more and more predatory in its tax approach - these tax advantages will be challenged in the future, as Governments look to find newer ways of extracting more out of the middle-earning people, but its hard to speculate how they will be affected unless we see the specifics of the changes when they come along. At the moment, taxpayers are better off just making the most of what they see as the current tax status and adjust as things change.

As the state pension age will likely increase, the age for personal pension is also likely to increase. I believe the current age limit is 57.

Most employers don’t directly talk to pension providers, but involve a broker, whose job is to go out and identify the best possible solution for the employers’ requirements. Some of this indirection is for effectiveness, and the rest is to ensure that the task of “due diligence” has been outsourced, in case questions are asked in the future. No malice, just reality of life.