NVDA, China & Performance Update (Q2'24)

I continue to be backing the wrong horses in the short term

After a brief interlude into politics and UK economic growth last week, I am back on to investing and will post a brief performance update this weekend, as Q2 has just closed. Previous performance write-ups here. For reference, here is my Coffee Can Portfolio and the benchmark is FTSE Global All Cap Index Fund (henceforth known as “benchmark”)

Cumulative Portfolio Return (XIRR basis): 8.60%

Cumulative Benchmark Returns (XIRR basis): 13.55%

Alpha (over benchmark): -4.95%

Inflation (XIRR basis): 4.45%

Real returns (net of Inflation): 4.16%

Holding Pattern on Returns

If you compare these results with the last quarter, both the Alpha (-4.95%) and Real Returns over Inflation (4.16%) have continued to be very similar between Q1 and Q2. The former is bad - i.e. the portfolio is unable to narrow the gap with the benchmark. The latter is okayish - the portfolio continues to produce real returns that will keep my buying power of my investments growing. However, it is worth looking at two aspects that are underpinning the underperformance of the portfolio.

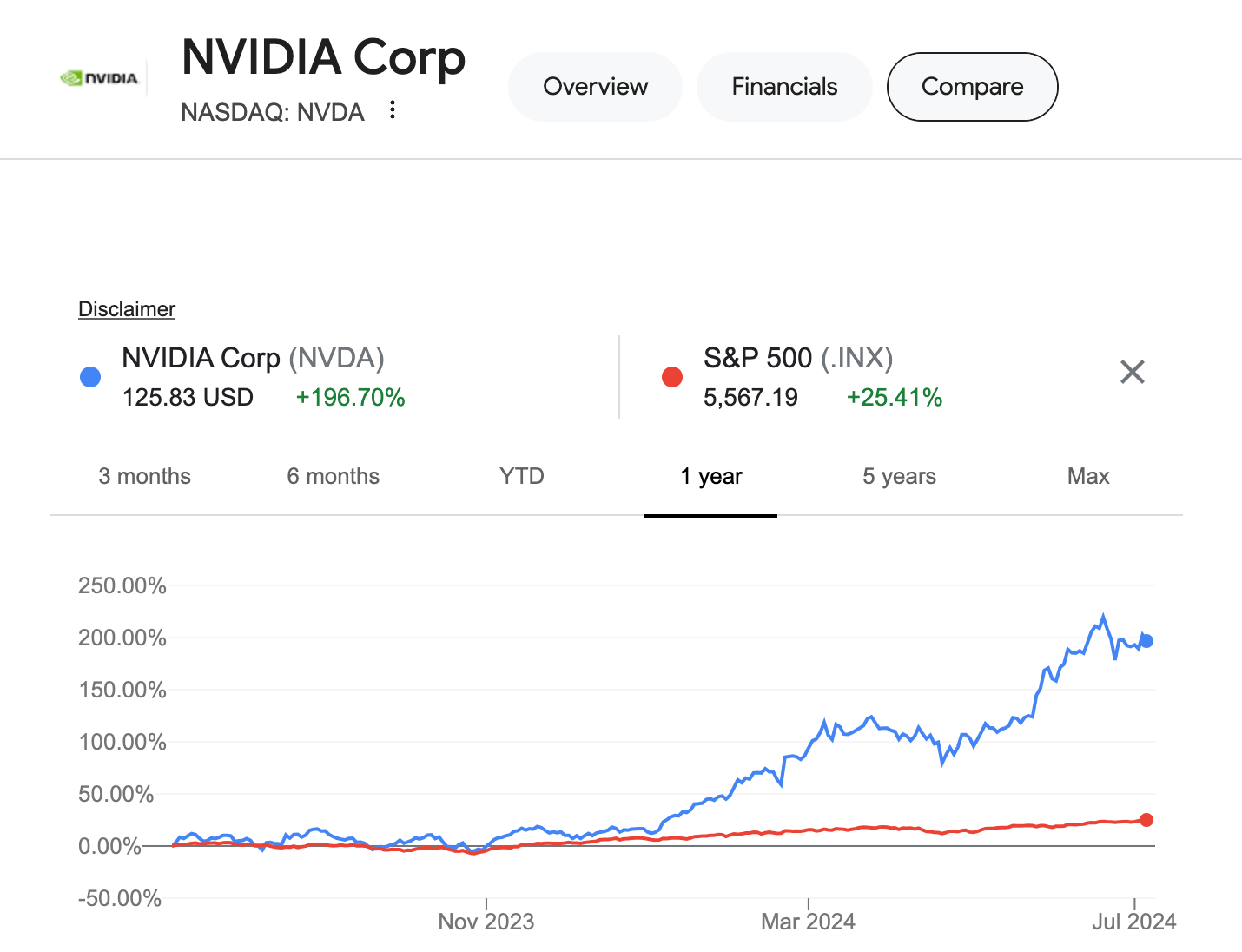

The rise and rise and rise of NVDA

The US stock market and the benchmark have a single major linchpin - the rise and rise and rise of NVDA. S&P 500 has had a spectacular 25% rise in the past year or so, but that has been completely dwarfed by the 200% rise in NVDA.

It is somewhat rare for a mega cap stock (valued at about a $1Tn a year ago) to be tripling in value in a single year, but such has been the historic nature of this spectacular rise. NVDA has morphed itself from a punt on the future, to a growth stock, to being a bit of an all-in-one - it is growth, it is value, it is meme stock, it is futuristic. It seems to be in the basket of every kind of investor, except of course mine. 🤦

Within my style of investment, NVDA is unlikely to have fit my portfolio at any given time. It was always just too costly by most metrics, even though the business was doing very well even before the AI inflection. In fact, Andrew Walker recently captured a better mental model for identifying value in such companies in this very well written article:

The point I am trying to make is that my portfolio is based on certain assumptions of returns and the expectations is to be surprised on the upside, not based on clairvoyance, and it is almost designed to miss out on such growth stories, except of course by happenstance.

From a performance perspective, NVDA has on its own accounted for 34% of the S&P 500’s rise this year, or roughly 17% of the performance of the FTSE AWAC fund. Back that performance out and I believe the alpha with the benchmark would be closer to about -3%. Let me explain where that -3% can be accounted for.

China underperformance

The largest underperforming group in my portfolio continues to be my Chinese holdings (some 15% of the portfolio), all of whom baring Lenovo have continued to be a massive drag. A good macro barometer for non-Chinese investors like us is how the Hang Seng Index (HSI)1 is faring:

In the past 5 years, the index has been roughly cut in half. In the past 12-18 months most investors have been fleeing China/Hong-Kong markets, creating a significant downward pressure on prices. However, the underperformance is not purely due to technicals here. There is genuine slowing down of corporate performance across my Chinese holdings:

Tencent (HKG:0700) announced an OPAT of RMB 115Bn for 2023 (down from RMB 188Bn in 2022)

At Anhui Conch Cement (HKG:0914), while revenue went up in 2023, COGS and interest expense has shot up so much, that net profit is down roughly a third.

Sinopharm Group (HKG:1099) is holding steady, eking out a small 5% increase in OPAT.

JD.com (HKG:9618)’s 2023 OPAT is up from 2022, but it is still significantly below 2020, and there isn’t much growth visible for 2024.

Alibaba (HKG:9988) has done well, posting a 10% increase in Diluted EPS. Even then, it is about half of what the company was posting in 2020 and 2021.

NetEase (HKG:9999) produced solid results - Revenue up 7%, OPAT up 50%, and continues to be one of the consistent performers in the portfolio from a business perspective.

As you can see the Chinese holdings in the portfolio aren’t blazing away from a business front in the past 1-3 years. The market was generally right in downgrading these stocks.

In fact the remainder of the 3% of the gap between the benchmark and my portfolio can be purely explained by the underperformance in China which lost 5.2% in the past year, while the rest of the world gained roughly 20%. With a 15% weighting, that amounts to about -3.75% in alpha.

While I don’t know if or when Chinese holdings will start performing in line with the rest of the world or not, the underperformance is unlikely to correct itself in the short-term, i.e. the next 6 months or so. Given the mixed bag results on the fundamental end, and the lack of a visible timeline where these companies will start performing again, I have wound down my derivatives exposure in China, and converted all of them into holdings in the underlying stocks (not on a 1-1 basis, which would have increased my holding way beyond my comfort level).

This means my net position in China (inclusive of derivatives) has come down this quarter, while I haven’t sold a single stock yet, Coffee Can style. My take on it is that if China picks up steam in the next 18 months or so, my 15% holding is enough to earn the upside, and if continues to underperform, I am happy to let my China holdings dilute with time.

Summary

When I set up this portfolio, I was prepared for significant periods of underperformance with the benchmark. In fact one of the primary objectives of the Coffee Can style of Investing is to limit the reactions that an investor can make when faced with market extremes and I wrote this about a year ago on this topic:

I am going to stick the philosophy and let the portfolio do its thing, however painful the interim might be. And with that note, Happy Investing!

Most Chinese companies list in Hong Kong as an avenue for foreign investors to buy into them. Over time, Hong Kong’s main index HSI has become a China centric bellwether index for non-Chinese investors.