Harvesting Volatility - part II

Volatility Is Free. Taxes Are Not.

The previous post on Harvesting Volatility landed rather better than I expected. Thank you to everyone who read it, shared it, and most importantly, challenged it. As always, the best value comes from the questions that follow.

A few themes dominated the responses.

Does this extend for other ETFs with high volatility?

Does this volatility harvesting strategy still make sense once taxes are taken into account?

How does it really compare with the simplest alternative of all, buying and holding?

Both are fair questions. Both deserve a proper answer.

A Quick Recap

The original idea was deliberately simple.

Pick a highly liquid, highly diversified ETF.

Invest a fixed amount (say £1,000) once a week on a chosen day.

Accumulate units until the position hits a predefined profit threshold, then sell everything and go back to cash.

Rinse, Repeat, Patiently.

No leverage. No forecasts. Just methodical recycling of capital.

Using thirteen years of data1, the strategy worked across VWRL, a globally diversified tracker ETF, under a wide range of configurations. That in itself was mildly surprising. What was more surprising was that, on a pre-tax basis, it outperformed buy and hold more often than not.

Naturally, the next question was whether this was a quirk of one ETF, or something more general.

Extending the Test Set

To find out, I expanded the analysis to three ETFs.

VWRL, a globally diversified, lower volatility equity ETF

SPY, a broad US market proxy

QQQ, a higher beta, growth-heavy Nasdaq tracker

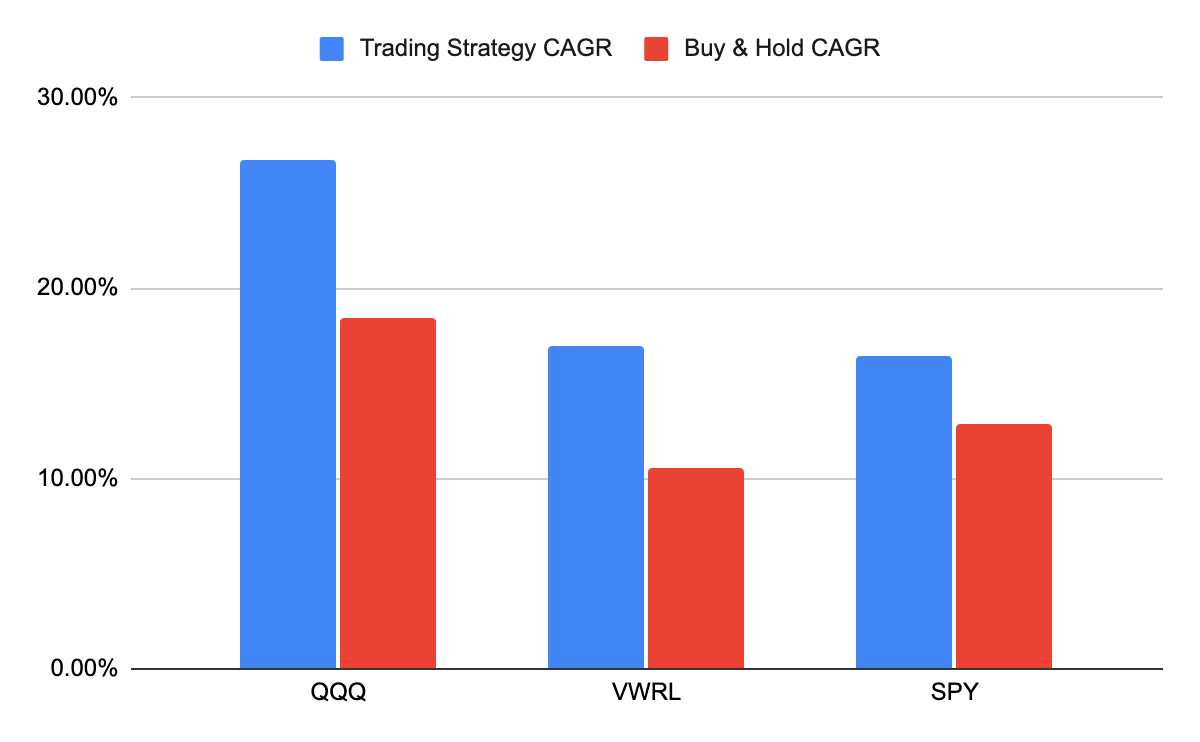

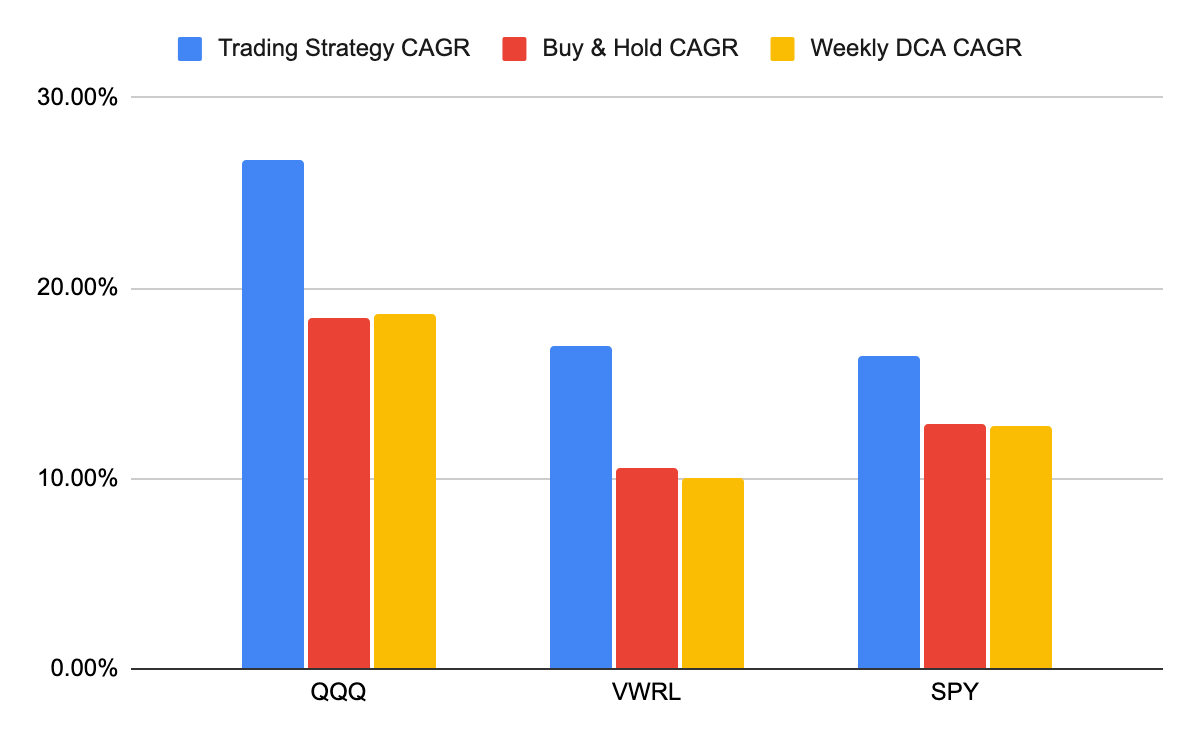

All three exhibit persistent volatility, albeit in very different ways. And all three, when tested using the same rules, produce positive results.

At first glance, this seems to support an intuitive assumption. Higher volatility should mean higher opportunity, and therefore higher returns. The data does not fully cooperate.

QQQ, the most volatile ETF in the sample, does indeed produce the highest returns. That fits the narrative. But SPY, which is more volatile than VWRL, produces lower returns than the global tracker, even though SPY has performed better as a buy and hold investment.

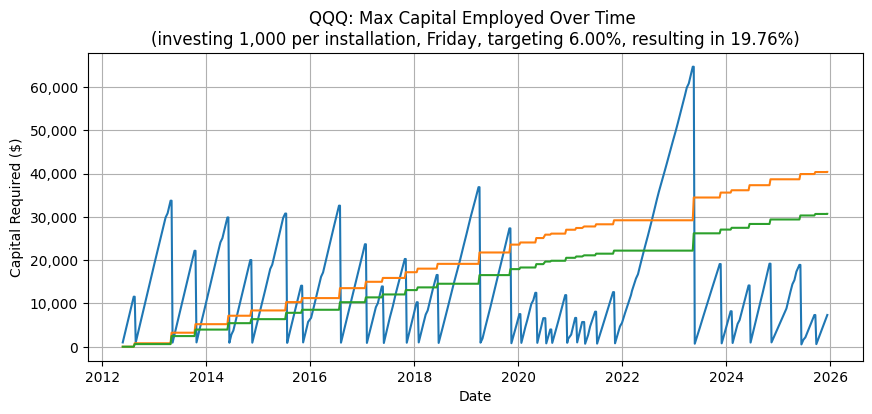

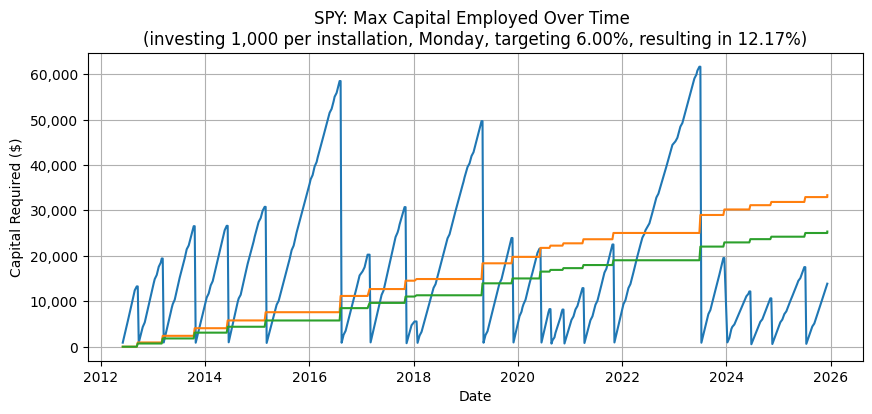

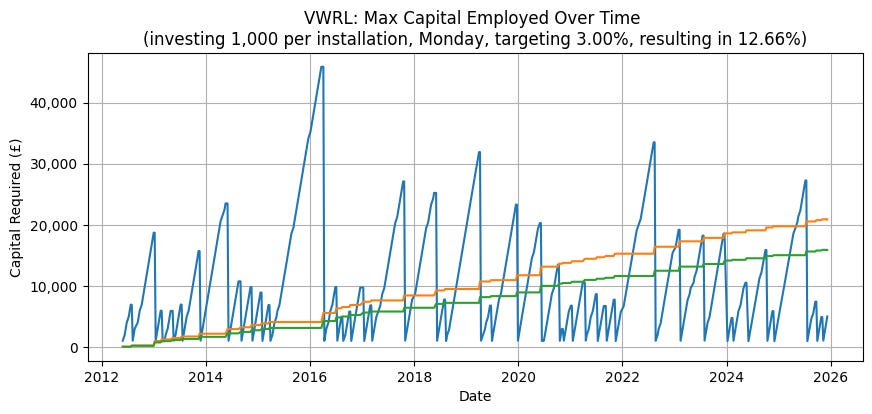

There is no clean, linear relationship between volatility and outcome. Volatility is necessary, but not sufficient. Market structure, trend persistence, drawdown depth, and recovery speed all matter. Higher volatility means deeper and longer drawdowns before a profit target is reached. That, in turn, means more weeks of buying and more capital committed before a sale occurs. This shows up very clearly in the maximum capital required charts.

In fact, SPY and QQQ both require far higher capital than VWRL to churn through the returns, but SPY does not generate significantly higher CAGR than VWRL. However, the trade-off between QQQ and VWRL is clearer - QQQ is higher volatility, requires higher capital through downturns, but produces far higher CAGR returns on this strategy.

Buy and Hold Is Not One Thing

Before declaring victory for any trading strategy, we need to be precise about what we are comparing it against. Buy and hold itself comes in two common flavours.

The first is investing a lump sum at the beginning of the period and holding it throughout. The second is investing gradually, for example weekly, and only selling everything at the end - effective Dollar Cost Averaging (DCA).

Both approaches work extremely well over long periods. Both are brutally simple. Both benefit enormously from the long term upward drift of equity markets. Obviously DCA works very well for most people as they have savings each month and it can easily be converted into a DCA strategy. In my tests, both buy and hold variants produced excellent returns.

Somewhat counterintuitively though, they still fell short of the volatility harvesting strategy in most cases. That is not because buy and hold is bad. It is because the trading strategy is recycling capital more aggressively. It spends less time fully exposed, realises gains repeatedly, and compounds them sooner.

This is not magic. It is capital efficiency.

Taxes Complicate Everything

Of course, none of this matters if taxes erase the edge.

Tax treatment varies wildly by jurisdiction and account type. In the UK, you could run the trading strategy inside an ISA or a pension and pay no capital gains tax at all. In places like Singapore or Dubai, capital gains are generally not taxed. In a corporate structure, you might face corporate tax rates somewhere between 12 and 25 percent.

In the US and India, matters are considerably more complex. Holding period matters. Short term and long term gains are taxed differently. Even in the UK, outside tax-sheltered accounts, the thirty-day rule complicates frequent selling and buying of the same asset.

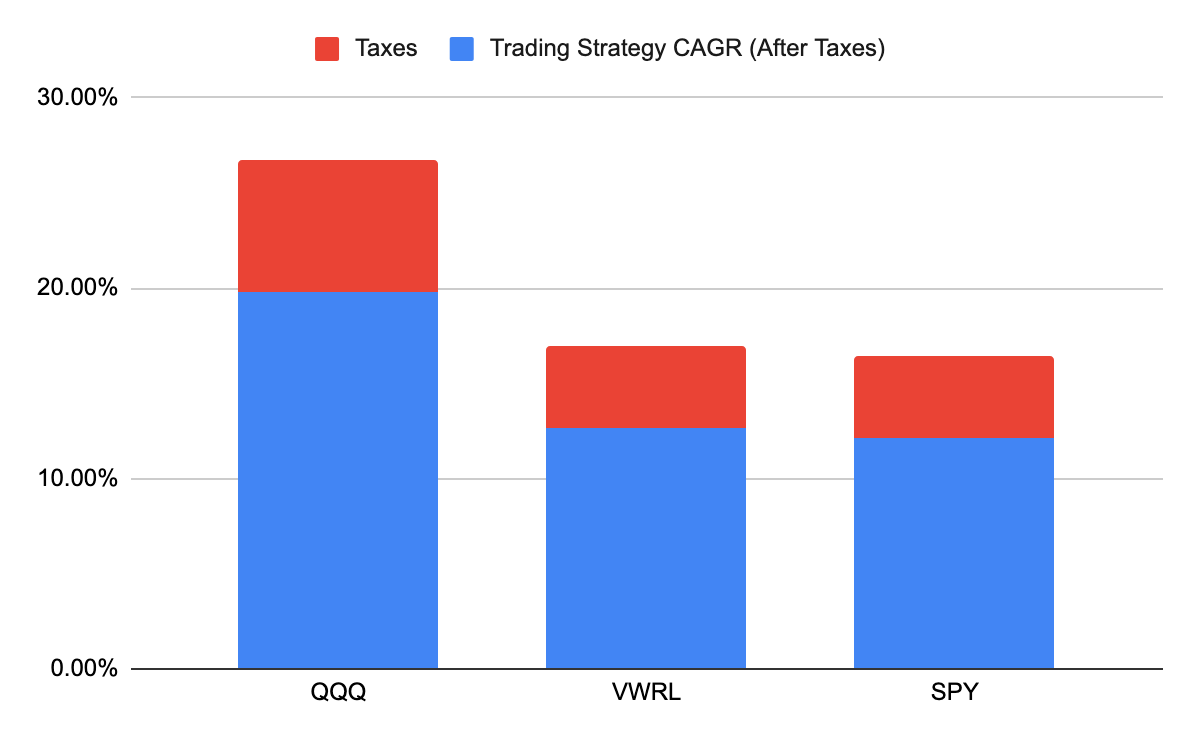

To avoid disappearing down a tax rabbit hole, I assumed something deliberately simple. A flat 24 percent capital gains tax, applied to all realised profits, with no allowances, no offsets, and no clever accounting. This is conservative. It almost certainly overstates the tax drag in many real world setups. Even under this blunt assumption, the volatility strategy still holds up surprisingly well.

Right Then, On to Taxes

First, the obvious point. Taxes hurt. A lot. The question is not whether they matter, but by how much.

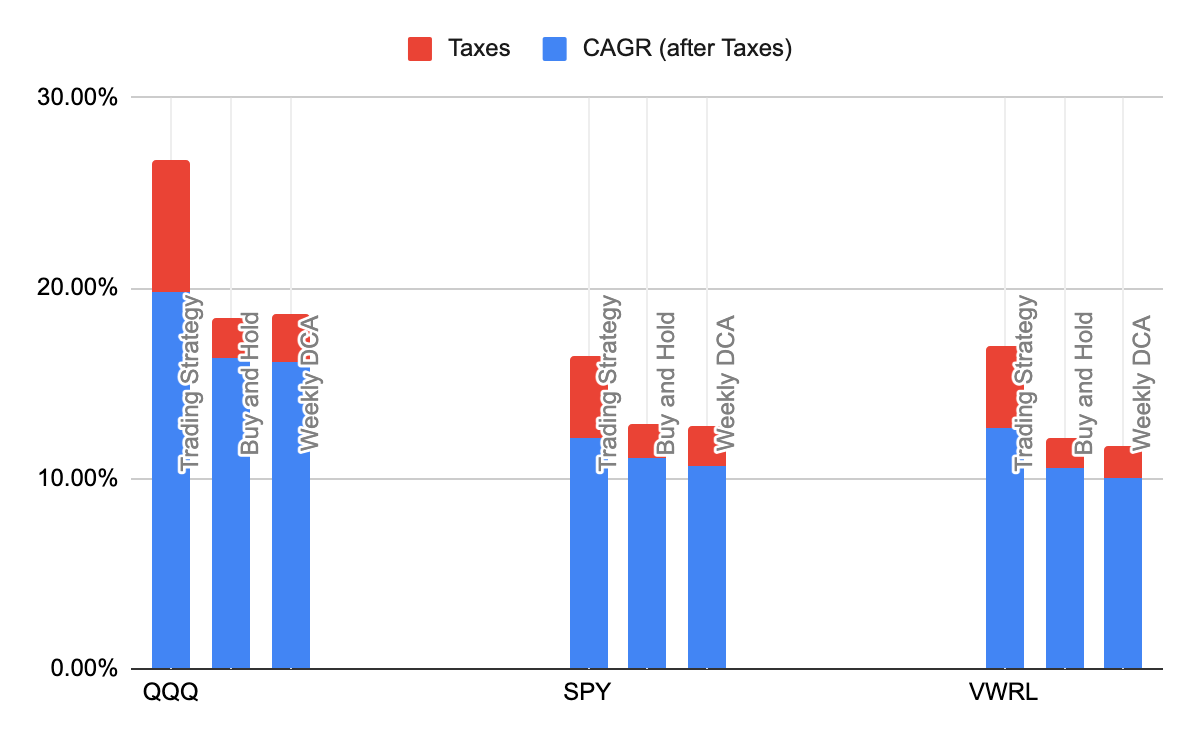

For QQQ, the volatility harvesting strategy produced a pre-tax CAGR of 26.75%. After applying incremental taxation (24%), that dropped to 19.76%. For VWRL, the trading strategy delivered 16.97% pre-tax and 12.66% after tax. For SPY, respective numbers were 16.42% pre-tax and 12.17% post-tax.

Buy and hold came in at 18.41 percent pre-tax and 16.3 percent post-tax. Weekly investing with a final sale landed at 18.61 percent pre-tax and 16.07 percent after tax.

Buy and hold produced 10.53 percent and 8.94 percent respectively, with weekly investing just below that.

For SPY, the numbers were closer. The strategy delivered 16.42 percent pre-tax and 12.17 percent post-tax. Buy and hold came in at 12.86 percent and 11.08 percent.

Even after taxes, the trading strategy often still comes out ahead.

That deserves closer scrutiny.

A Fairer Comparison

One subtle but important point emerged while doing this work.

It is disingenuous to tax only the trading strategy and leave buy and hold untouched. If all strategies are run in the same type of account, then buy and hold also faces tax, just deferred to the end.

Once you apply the same tax logic consistently across all strategies, the comparison becomes fairer, and the relative attractiveness of the trading approach improves.

Buy and hold benefits from deferral, but it also concentrates the tax hit. The trading strategy pays taxes earlier and more often, but it also reinvests post-tax gains sooner. The net effect is not as lopsided as one might expect.

What About Dividends?

There is another omission worth acknowledging.

The buy and hold numbers do not include dividends. For ETFs like VWRL or SPY, dividends typically add around 1.2 to 1.5 percent per year. That would improve buy and hold returns modestly.

However, the trading strategy is not dividend blind either. It will sometimes hold positions over dividend dates and receive distributions. Those distributions would themselves be taxable in most accounts.

I have not modelled this precisely. My rough estimate is that dividends might add around one percentage point to returns for both approaches, once taxed appropriately. Enough to matter, but unlikely to overturn the broad conclusions. In case you are serious about any of this, I will leave it to you as homework.

So, Should You Do This?

It depends on what you are optimising for. If you want to keep capital requirements low, VWRL is the most forgiving candidate. Even after taxes, it produces respectable returns with relatively modest peak capital commitments. If you want to maximise returns and can tolerate higher capital swings, QQQ does what it says on the tin.

But stepping back, there is a bigger point.

Life is not just about optimising returns. It is also about optimising the ratio of returns to headache. Buy and hold remains astonishingly effective. It requires almost no decision making. It scales effortlessly. It is tax efficient by default. And it frees up time and mental energy for things that matter more than weekly rebalancing.

The volatility harvesting strategy sits in a narrow middle ground. It is not passive enough to be ignored, and not aggressive enough to dominate. It is interesting, intellectually satisfying, and potentially useful for a specific bucket of capital that you do not want to commit indefinitely, but also do not want sitting idle.

That is a narrower use case than many trading strategies claim. Which, frankly, is a feature rather than a bug.

Final Thoughts

The real lesson here is not that volatility trading beats buy and hold. It often does not, once taxes, dividends, and effort are properly accounted for.

The lesson is that volatility itself is not the enemy. It is a structural feature of markets. You can ignore it, fear it, or attempt to shape it into something mildly productive, provided you understand the trade-offs.

As ever, past returns are not indicative of future returns. And simplicity, boring as it sounds, remains a powerful edge. On that note, Happy investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is for educational and entertainment purposes only. Do your own due diligence before investing. I may hold or enter into positions in the securities mentioned above. This is not a solicitation to buy or sell any security.

The 13 year time line was chosen as that was how long data on VWRL goes back on. One admitted blind spot in this entire thesis is that it is the beginning of a secular bull run we have had. Caveat emptor!

Interesting. Here's a tax efficient thought for consideration, at least for US investors considering your strategy:

- invest weekly, as you do

- at 52 weeks, harvest the "head" lots [taxed at long term rate]

As a UK tax payer you have no such step, of course.