Harvesting Volatility

A data-driven look at profiting from volatility using plain-vanilla ETFs

Volatility is usually spoken about with a degree of nervous respect. It is the thing that makes portfolios lurch around, that causes perfectly rational people to abandon long term plans at precisely the wrong moment. An entire industry (with many niches1) exist to help us dampen it, hedge it, smooth it away. But step back for a moment and a slightly uncomfortable question appears. If volatility is so persistent, so measurable, and so unavoidable, is it really just something to fear? Or is there a way to profit from it?

For most retail investors, the accepted answer is dollar cost averaging (DCA). You invest a fixed amount at regular intervals, regardless of price. Over time, volatility works in your favour by lowering your average purchase price during drawdowns. It is a perfectly sensible approach for long term accumulation, especially for those still in the wealth building phase of life. But DCA is fundamentally passive and best suited for long term buy-and-hold - with both averaging and long-term mentality expounded frequently on this blog. DCA assumes volatility exists, but it does not actively monetise it. Which raises the next question. Is there a trading strategy that can do exactly that?

Trading volatility is not new. In fact, it is one of the oldest games in institutional finance. Proprietary trading desks at banks, and multi asset managers running internal capital, have been exploiting price oscillations for decades. They do not care deeply about long term valuation. What they care about is turnover, time in position, and return on capital employed. Make a small return, repeat it often, and keep capital working efficiently. When you have leverage, this approach scales beautifully.

And that last point is precisely why retail investors rarely do this. Volatility trading works best when you can amplify small price moves with leverage and do so in automated ways doing many hundreds, if not thousands of transactions in a fixed time period. Make half a percent a hundred times a year on borrowed money and suddenly the returns look impressive. But leverage brings its own risks, margin calls being the most obvious one, and it is neither cheap nor psychologically comfortable for most individuals, and automation of this extend is most certainly not the domain of the retail trader. Without leverage and automation, the sums appear underwhelming, at least at first glance. If you are deploying your own capital, tying it up for uncertain periods, and paying transaction costs along the way, the strategy needs to work rather hard to justify itself.

However, difficult does not mean impossible.

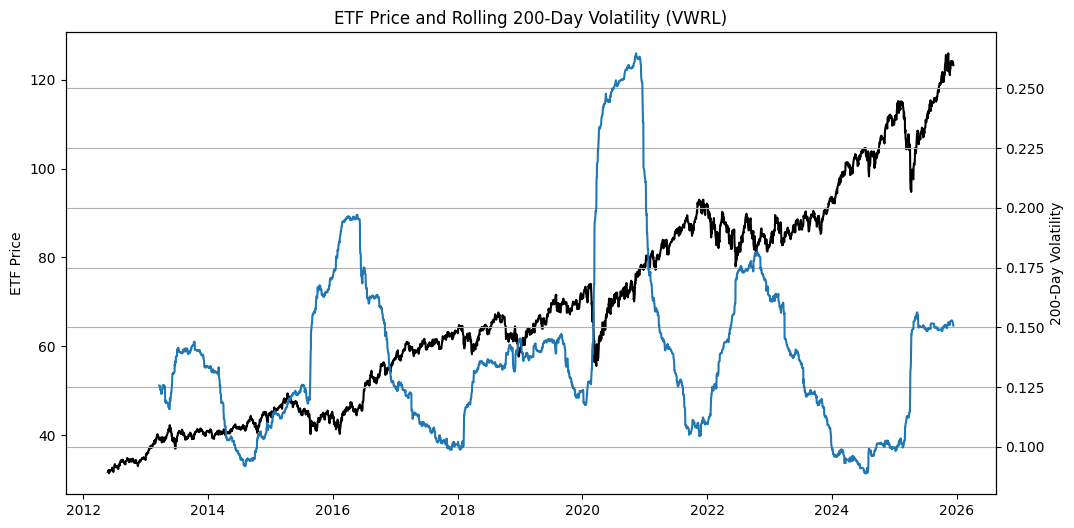

Consider a highly liquid, highly diversified, and heavily tracked index ETF. Something like VWRL.

It owns thousands of companies across regions and sectors. It is not going to zero. It is not going to triple overnight either. What it does do, relentlessly, is wobble. Even in broadly rising markets, it regularly moves up and down by a few percent. That volatility is often ignored because long term investors are told to look through it. But what if we do not?

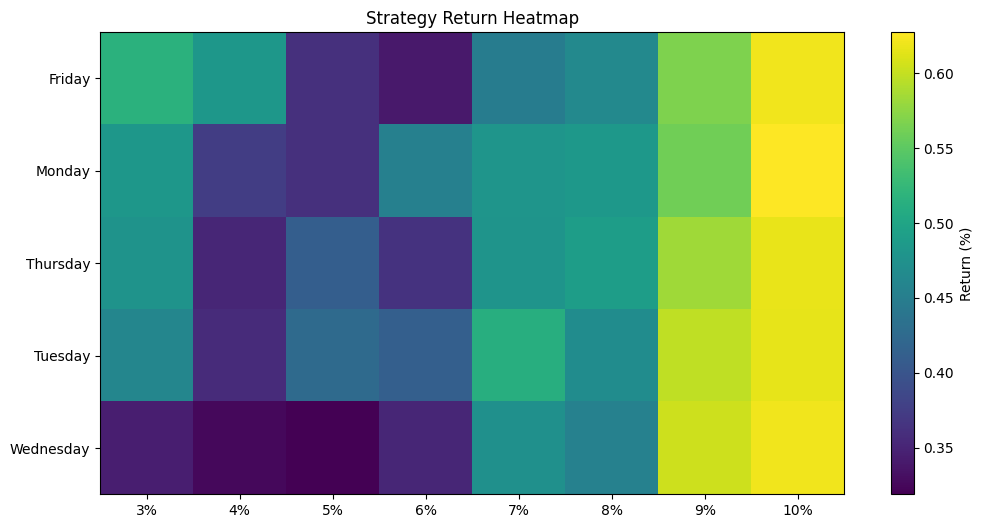

Here is a simple thought experiment, turned into an actual backtest. Pick a single day of the week. Every week, on that day, you invest a fixed sum into the ETF. You only buy whole units, no fractions. When your accumulated position reaches a certain positive return, say 3 percent, 5 percent, or 7 percent, you sell the entire position and go back to cash. Then you repeat the process from scratch. You never buy and sell on the same day. If the chosen day is a market holiday, you do nothing. You pay a small brokerage fee (£2) on every transaction, and you assume a modest bid ask spread cost on selling (0.1%)2.

This is not momentum investing. It is not value investing. It is not market timing in the traditional sense. It is simply harvesting repeated excursions away from a local mean, using time and patience instead of leverage.

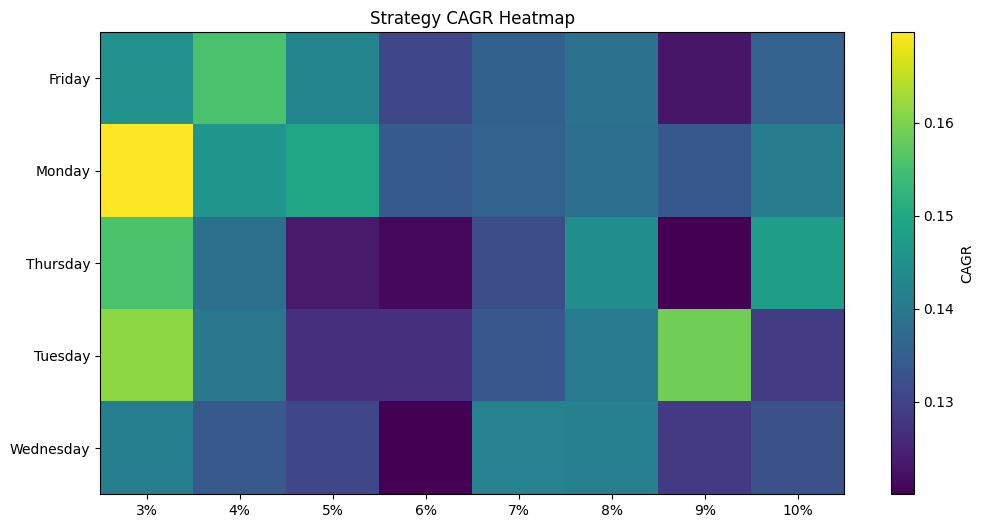

To make this more than armchair theory, I ran this strategy across thirteen years of daily price data. Different weekdays were tested. Different profit thresholds were tested, from 3 percent to 10 percent. Transaction costs were explicitly included. Whole units only. No flattering assumptions. Returns were measured not just in absolute pounds, but in CAGR terms using actual cash flows, so that faster capital recycling was rewarded appropriately.

The results were, if not spectacular, at least interesting. First, the strategy does make money - surprisingly in almost all configurations. Higher thresholds require more patience and more capital tied up at peak, but they reduce churn.

Lower profit thresholds tend to trigger exits more frequently. Somewhere in the middle, typically around the 4 to 6 percent range, there is often a sweet spot where capital does not sit idle for too long, but transaction costs do not overwhelm returns.

Second, cadence matters. The day of the week is not irrelevant. Some days consistently perform better than others for certain thresholds. This is not magic, and it is not guaranteed to persist, but it does suggest that even simple behavioural and liquidity patterns can leave fingerprints in price data. That said, as you can see above, while there is variation ins returns, almost all of the combinations result in at least 11% CAGR return - which is, to put it mildly, not bad.

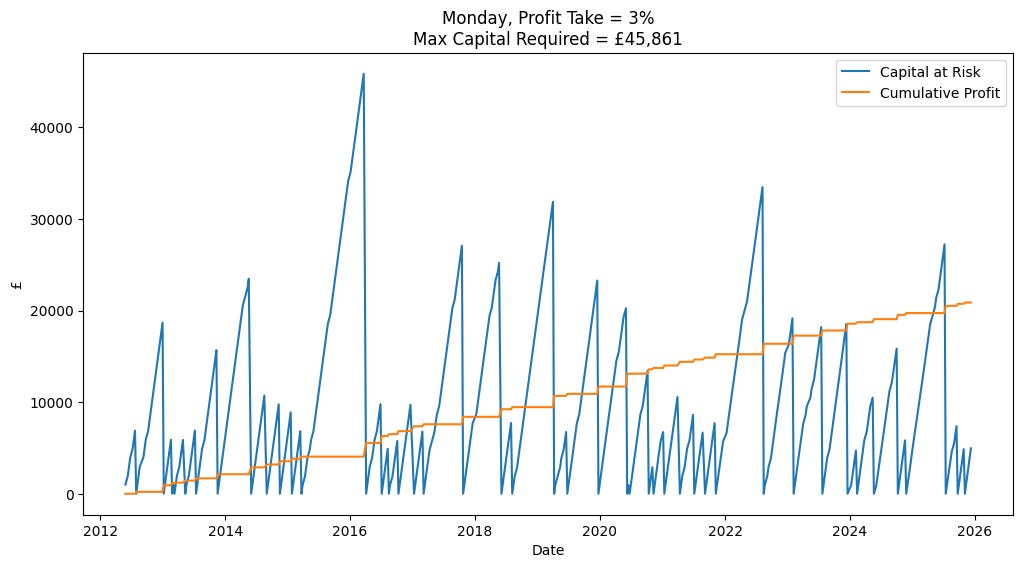

Put together, profits relative to capital employed can be surprisingly attractive. At a 3 percent profit target, capital often completes a full buy and sell cycle within roughly twelve months. In other words, the money you put in is not necessarily locked away for years.

Over time, as profits accumulate, the psychological and financial burden of future cycles becomes less onerous. You are still deploying capital, but you are increasingly doing so with gains rather than fresh savings.

This is not a magic money machine. It will not replace a well constructed long term portfolio.

It is important to be clear eyed about what this is and is not. After adjusting for transaction costs and the opportunity cost (roughly 4-5% risk free rate) of having capital intermittently tied up, the long term CAGR ends up not wildly different from normal equity returns. This is not a magic money machine. It will not replace a well constructed long term portfolio. It is also sensitive to assumptions. Increase costs, reduce volatility, or impose longer holding periods, and the edge quickly shrinks.

So why bother?

Because as an intellectual exercise, it is valuable. It forces you to think about capital efficiency rather than just raw returns. It highlights the difference between time in the market and time of capital. And it demonstrates that volatility is not just a source of anxiety, but also a raw material that can be shaped into something mildly useful.

More practically, this kind of strategy may suit a very specific bucket of money. Capital that you do not want to lock away for decades, but that you are also not comfortable leaving entirely idle. Capital that you can tolerate being tied up for months, perhaps even a year, but not indefinitely. In that narrow space, a disciplined volatility harvesting approach can make sense.

(ps: I am well aware that this complicates matters compared to a simpler approach of just holding bonds for short term needs, and having everything else in equity, as advocated in my previous post - hence, this is more of a mental exercise than anything else. To be clear, I have not run this trading strategy, nor have commitments to do so - if you plan to try this, then do your own due diligence first.)

The real lesson, though, is not about this specific strategy. It is about mindset. Volatility is not an enemy. It is a feature of markets. Long term investors can ignore it. Short term traders can fear it. Or, with the right constraints and expectations, you can attempt to profit from it quietly, methodically, and without leverage.

Just do not expect miracles. On that note, happy investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the securities mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.

Buffer ETFs, for one, among many more

All graphs and simulated reports produced on Google Colab, with code produced from ChatGPT.

Great article. It would be helpful to know how much return you gain by doing this exercise over what you would have gained if you just held the equity throughout the period. Also which days of the week are best to buy and sell?