Earnings Update: Challenger Financial

Things are improving; time to increase holdings

Survey on next stage of the substack

Thank you for the love and support you have show to the Coffee Can Investor substack. It has been many months of regular writing for me and I have loved every minute of it so far & I hope I have not wasted too much of your time in doing so. Now seems like a good time to gauge from current readers on what you like reading today on the website. I am also trying to assess if newer streams of content (like a podcast or more coffee can portfolios) might be of interest. Please take 2 minutes of your time to respond to a survey please.

Latest Results at Challenger Financial (ASX:CGF) ❤️

Readers might recall my summary analysis on Challenger Financial (ASX:CGF) from about 2 months back. This week, the company dropped its latest results and it is timely to revisit the stock.

For those who want to go through the source information, here is the investor presentation, and here is the annual report.

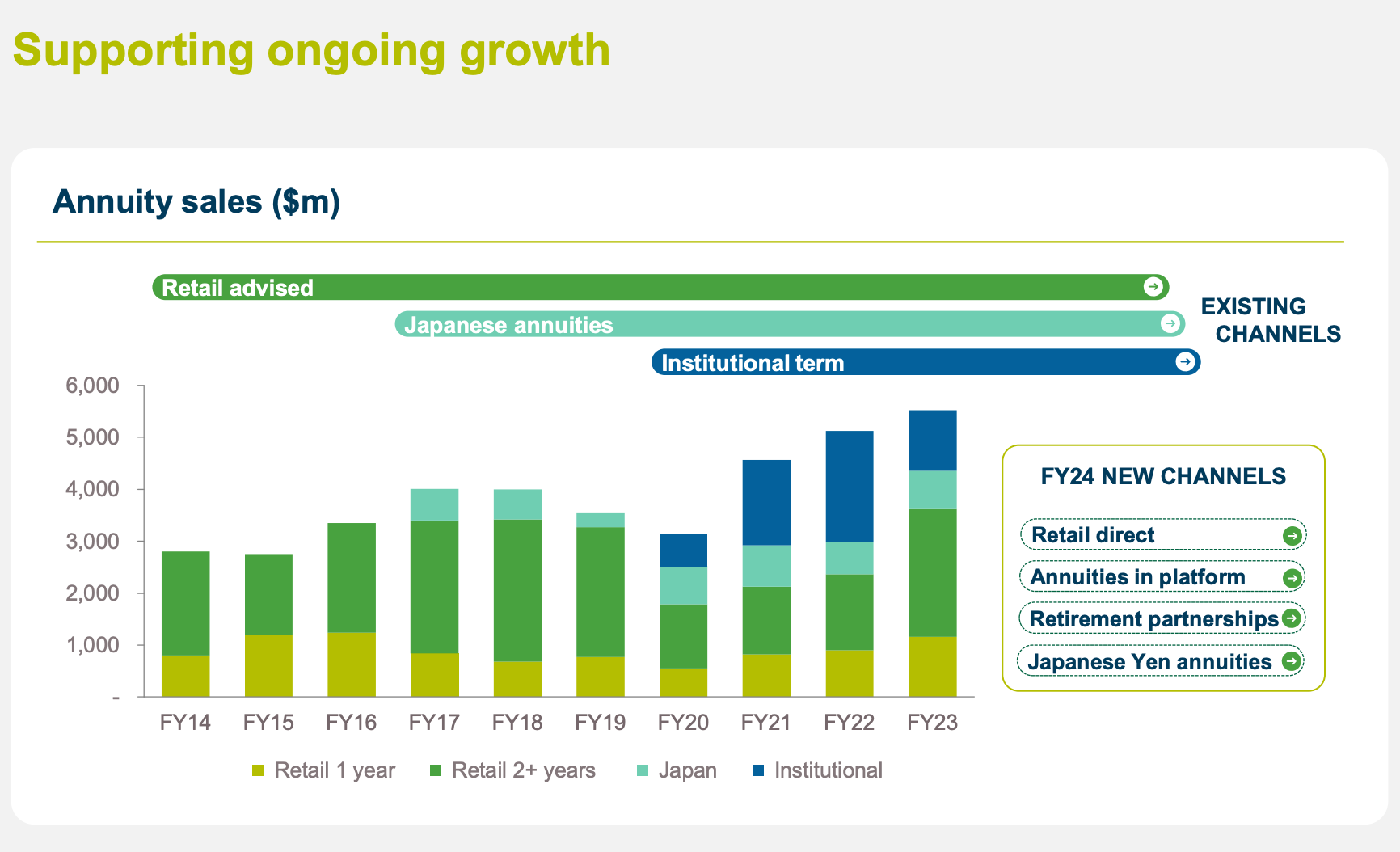

As a quick recap of my last post, Challenger Financial is a leading provider of annuities and retirement products in Australia and operates in what is a growing opportunity space in that market. Challenger had a fantastic growth phase between 2009-2018, but faced headwinds since, especially due to the regulatory changes emanating from the recommendations of the Hayne Royal Commission. Post that change, business dropped significantly, along with dividends and the share price. A new Chair, CEO and CFO have come together in the last 2 years to rebuild the business.

With that context, the latest tape update is distinctly encouraging news. Revenue is up 32%, and profits are up about ~14%. This is now the third consecutive year where numbers are looking up. With the company announcing a dividend increase from A$0.23 p.a to A$0.24 p.a, it signals the 3rd year of increasing, fully-franked1 dividend. Recall that this company had a 14 year track record of ever-increasing dividend before the business fell off a cliff and dividend had to be cut by 50%.

Encouraging signs are visible elsewhere in the print too, including a 6.5% growth in assets under management (AUM), a key indicator of health for this business, and a growing margin of extracting profits from AUM - up from 0.33% last year to 0.35% this year. It is not yet close to the 0.56%-0.70% it was able to extract from AUMs 5-10 years back, but it has arrested the decline and improved the metric for 3 years now.

Channel mix is looking healthier than before too, where annuity sales through the retail path is seeing solid growth after 3 years of sluggishness. For this business retail is going to be the strongest channel, as it will have maximum margin potential on this route.

With interest rates being high, and annuity products being priced attractively, I believe the company will continue to have some macro-economic tailwinds behind it.

Future of this company

It is in the DNA of the company to build on momentum and be a consistent generator of growing profits and shareholder returns. While it is hard to ascertain whether or not we have already hit that growth phase or if the business will see more hurdles, but it is clear that the company has survived the headwinds at large and the recovery, however slow, is steadily being achieved.

Pricing

This business is now attractive priced - at about 12x price-to-earnings, or about 5x price-to-free-cashflow, or about 1.5x price-to-book, or about 3.7% dividend yield. Slice it whichever way you want, this is a business well priced for long term investors like us. The last time the business was this attractively priced was in 2014 and shareholders from that time were very handsomely rewarded in the next 5-6 years.

"Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas." — Paul Samuelson

The way I see it is simple - at these price points, the downside is relatively low, for a profitable, well-run business that has a product fit for the market in what is a growing industry is a major, stable economy. On the other hand, if the business continues to inflect upwards, then this could be a leading generator of upside in the portfolio. I like such asymmetric bets.

Summary

I last wrote about this company when it was trading at $6.06 and since then the stock has moved up roughly 10% and a dividend due in a few days (28th August to be precise) which will add another 2% upside. At $6.73 close on Friday trading, with all the updates we have received, this continues to be attractively priced for me. I promptly added to my position this week. I expect to continue to add to my position.

As always, Happy Investing!

Disclaimer: I hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

Australian companies can “frank” their dividend so the receiver of the dividend don’t have to pay any more taxes on it. Typically, for foreign investors, franked dividends mean no withholding taxes in Australia.