Earnings Season Reflections: Stella-Jones, Bunzl & BAE Systems

Analyzing the latest earnings reports of three key stocks in my portfolio

I recently wrote about a selection of stocks in the “growth” world and how unforgiving the market can be. Turns out, the “value” world is no different. In this post, I’ll revisit three stocks following their latest annual results—each with some interesting patterns.

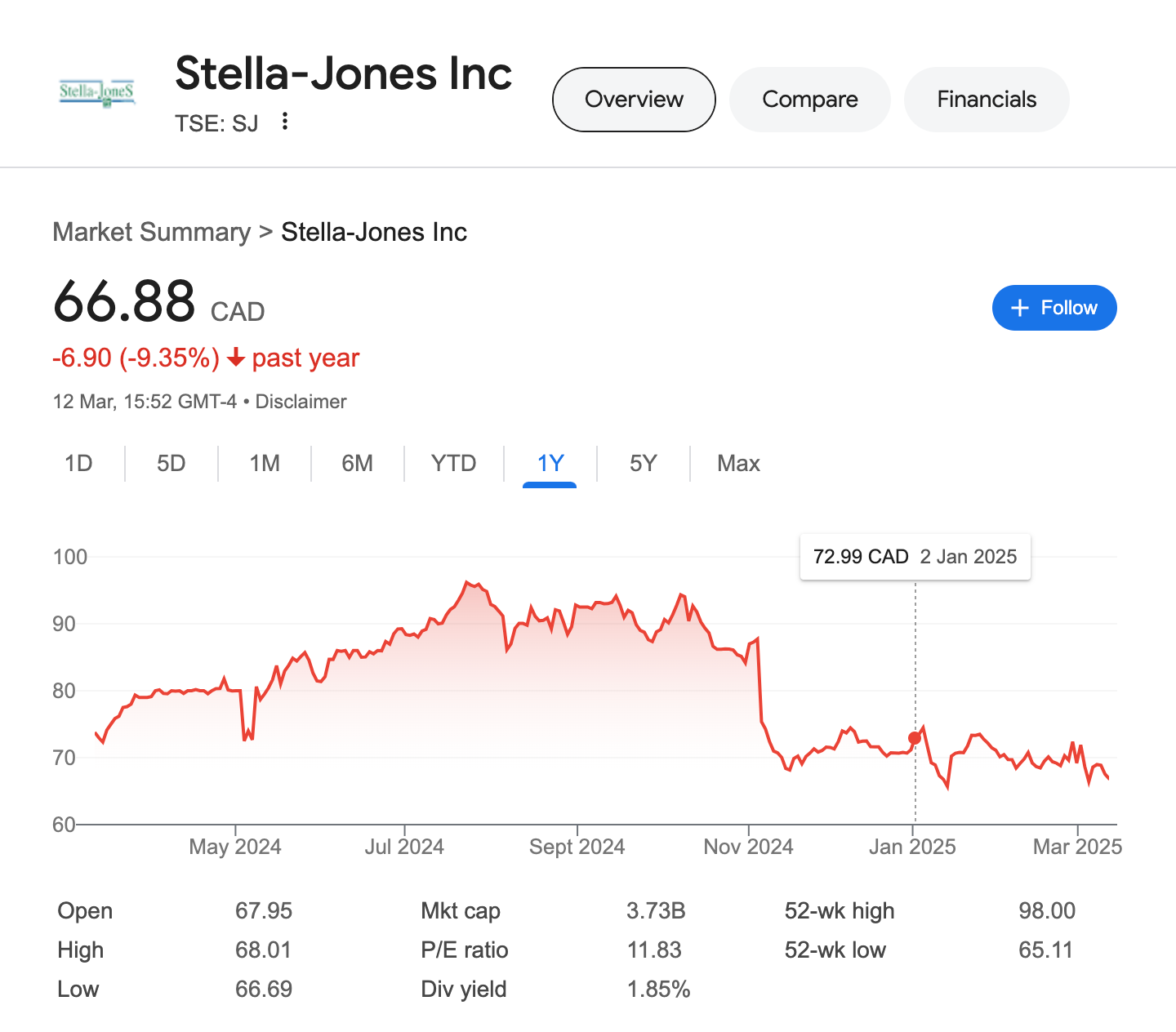

Stella-Jones (TSE:SJ, previous posts)

Just last month, I posted about Stella-Jones and the long-term upside I see in it. Now that their full-year results are out, it’s worth revisiting.

The numbers were largely in line with expectations—profit per share came in at $5.66, slightly higher than the previous year due to share buybacks rather than organic growth. 2024 was a challenging year for the business, no doubt.

That said, management’s outlook remains consistent with the original thesis: steady single-digit sales growth, solid profitability in the 17%-19% range, and a disciplined approach to capital allocation—primarily returning capital to shareholders through dividends and buybacks, with selective acquisitions.

What makes Stella-Jones compelling is its superior capital allocation. With a return on capital employed (ROCE) in the 15%-20% range, the company is generating about $320M in free cash flow. Roughly $150M goes to dividends and buybacks, while the remaining $170M strengthens retained earnings and supports further investments. This disciplined approach should continue delivering strong shareholder returns in the years ahead.

Despite these strengths, the stock trades at just 12.5x earnings—valued almost like a utility, even though its fundamentals are much stronger. One reason for this could be limited analyst coverage and the fact that it operates in a niche market.

As a long-term investor, I see an 8%-12.5% IRR at $70 per share, even under conservative assumptions. Any reasonable tailwind could push the stock to $90-$110 relatively quickly. After recent consolidations, this has become a fairly large position for me, and I plan to hold it for at least another year or two. Patience might be well rewarded here.

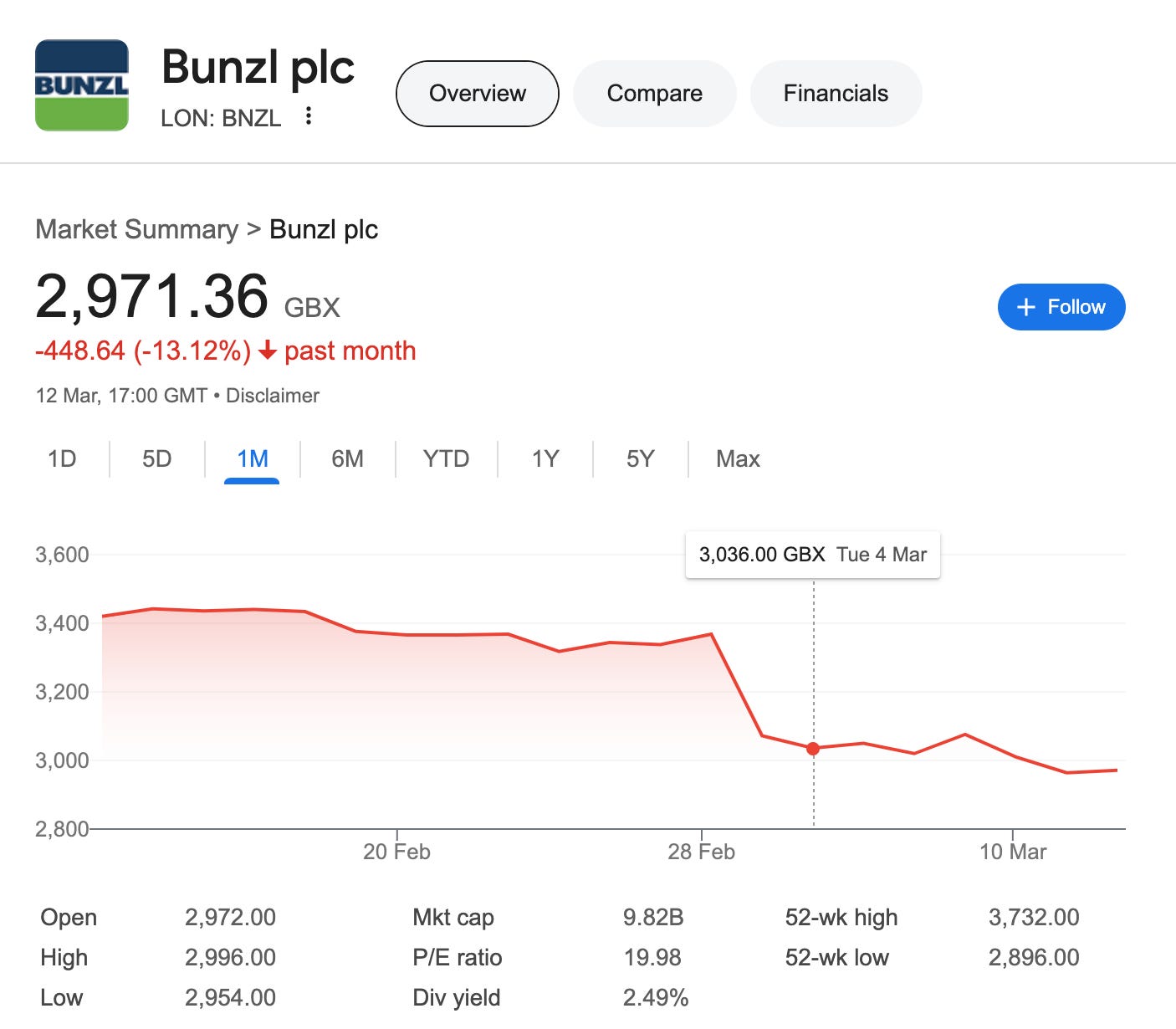

Bunzl (LON:BNZL, previous posts)

Like Stella-Jones, Bunzl was a solid performer in my portfolio—until a rough earnings report brought it back to earth.

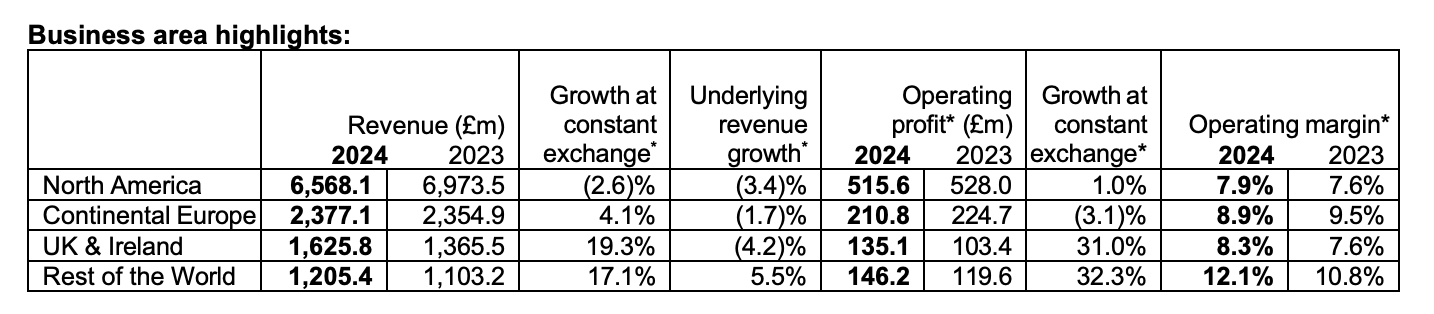

2024 was a challenging year, especially in North America, where revenues declined by a single-digit percentage. While other markets grew, North America is the company’s largest segment, and its struggles dragged down overall results.

Where Stella-Jones focuses on share repurchases alongside dividends, Bunzl prioritizes dividends and acquisitions. In 2024, it made a series of larger-than-usual acquisitions totaling £885M, adding around £72M in annualized operating profit—an expected 7-8% boost. These acquisitions were done at approximately 12.25x earnings, compared to Bunzl’s own trading multiple of 20x trailing earnings. If all goes well, these earnings should contribute meaningfully and make the stock appear cheaper.

The board continues to emphasize prudent capital allocation, and any normalization in the business should make the company even more attractive. Like Stella-Jones, this remains a large position for me. I don’t plan to add more unless I see improvements in the numbers, but hopefully, the next few quarters will bring positive news.

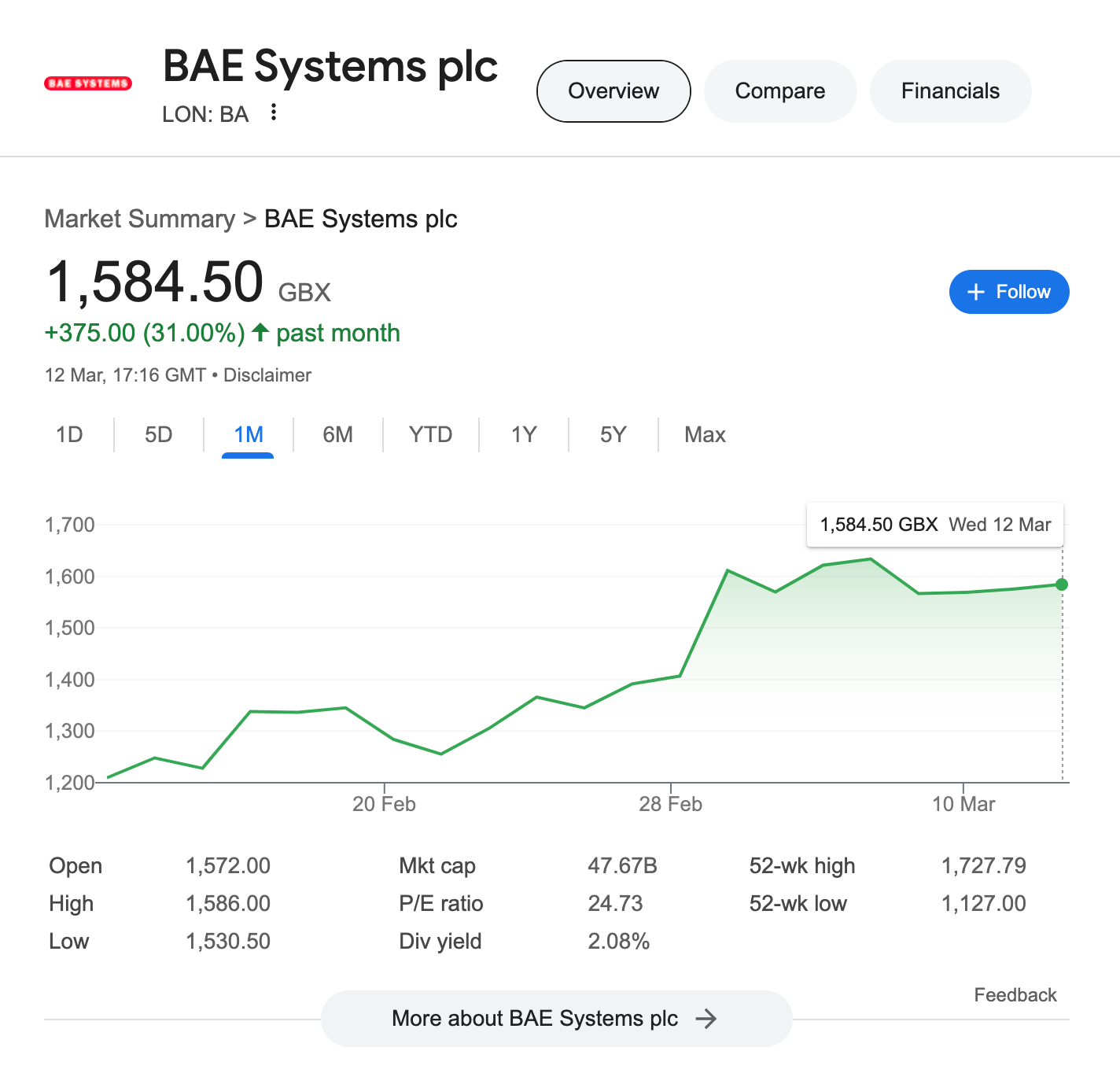

BAE Systems (LON:BA, previous posts)

Now for some good news—BAE Systems, another core holding in my portfolio, had an outstanding 2024.

I won’t go into too much detail because one graphic from their annual report sums it up perfectly: revenue, operating profit, cash flow, order book, and dividends—all moving in the right direction.

And shareholders have rewarded it accordingly.

Interestingly, I bought both Bunzl and BAE shares on the same day—just before their latest results. The market’s reaction to each stock couldn’t have been more different. If not for BAE, I’d be feeling extra disappointed right now. But as they say, you win some, you lose some.

Summary

One of the side effects of having a concentrated portfolio is feeling every earnings report more acutely. A disappointment can sink my portfolio, while good news can propel it forward. This stomach-churning volatility takes some getting used to, but I’d rather ride my winners than dilute returns with a portfolio full of mediocre stocks.

As always, happy investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.