The Story of the Stock Markets This Week—Told in Three Tales

From Datadog's pricing squeeze to AppLovin's rocket ride and Trade Desk's brutal reality check

Apriori Note: Following are a few tales from a few companies in my professional space, one of which I dabbled with in the past. For context, I am professionally employed at a programmatic DSP, and an up and coming success story in AdTech. This blog is purely my personal opinion and does not reflect the opinions of my employer in any manner.

Premier: AppLovin – The Meteoric Rise of AdTech

AdTech is back, and AppLovin is the poster child.

Founded in 2012, it started in gaming, then pivoted hard into adtech—first by building its own ad engine, then by acquiring MoPub from Twitter. As a professional in AdTech, I’d heard of MoPub before, but AppLovin really hit my radar when its stock started defying gravity.

That’s just one year. For perspective, Berkshire—my biggest holding—took 16 years to 10x like this.

If you land even one AppLovin (2024) in your portfolio and size it right (say, 5%), you’re sitting on market-beating alpha for years.

P.S. Do I think it belongs at $470? Not sure. I thought the same under $400 and even considered shorting it. Good thing I didn’t. The only thing worse than missing AppLovin would’ve been betting against it. That would’ve been financial ruin.

The next two companies are going through somewhat similar stories here.

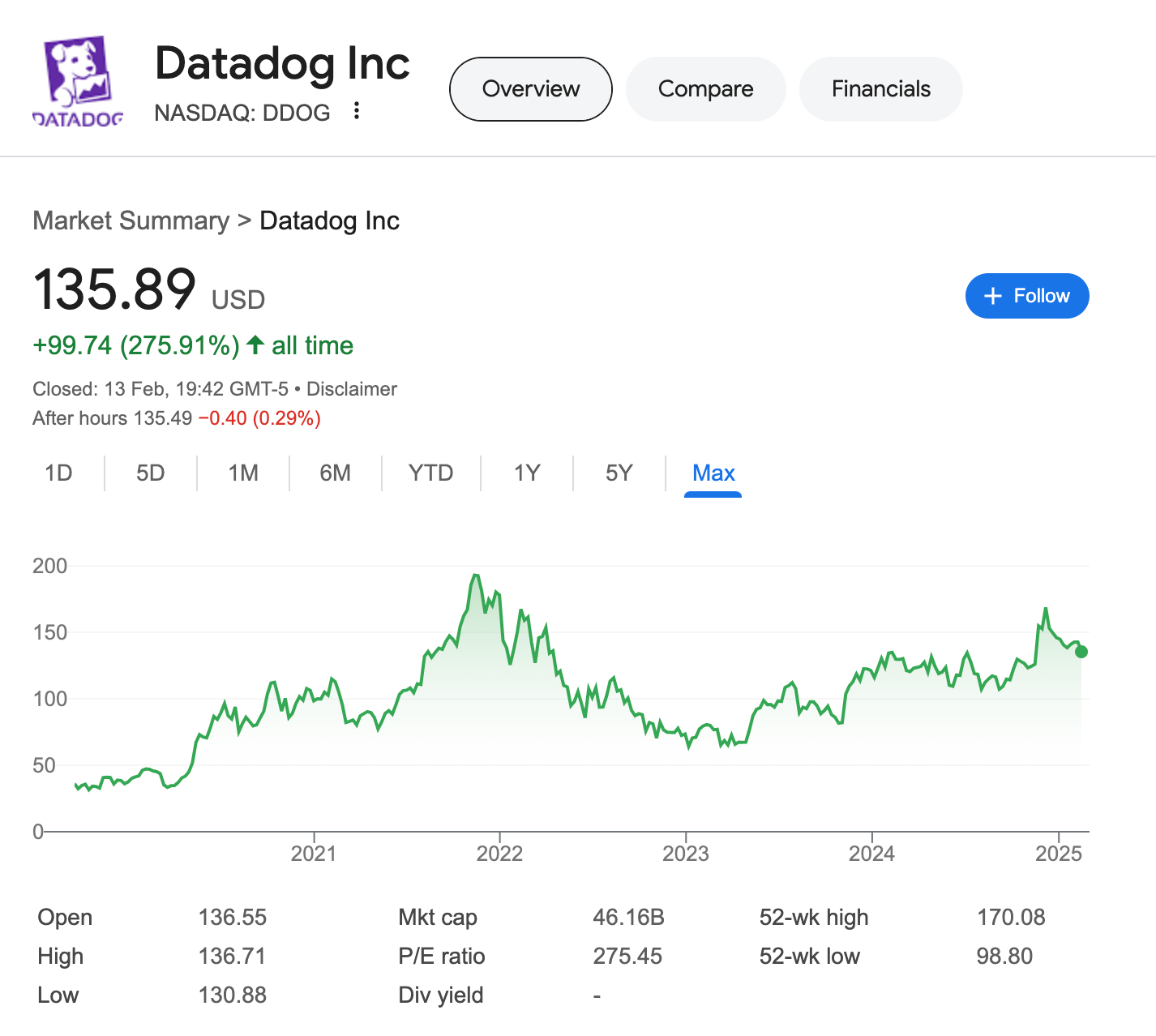

Deuxième: Datadog – When Pricing Power Bites Back

Let’s start with Datadog. An observability powerhouse, it’s the go-to for monitoring and logging—easy to set up, scale, and, well, expensive. The classic SaaS play: fully managed, usage-based pricing, and before you know it, you're on the hook for a seven-figure bill.

Eight years ago, my employer jumped on the Datadog bandwagon. One of my first projects? Migrate from our homegrown Nagios/Ganglia stack to Datadog. It worked like a charm—until the bill started ballooning.

Meanwhile, the stock took off, from its IPO in 2019 to a five-bagger at the COVID peak ($36 to $190+). Remember when we all thought remote work was forever, and governments hit the money-printing button like there was no tomorrow? Yeah, that era. Since then, it’s been a rollercoaster, settling at $155 last week—still a solid 4x in five years.

But Datadog’s aggressive pricing strategy pushed us to a breaking point. Past renewal negotiations weren’t great, and we saw the writing on the wall. Two core components—90% of our Datadog usage—got offloaded to a homegrown stack, saving us possibly millions.

And here’s the kicker: I once thought Datadog was too sticky to quit. But we did. Turns out, we weren’t alone. With cloud costs squeezing budgets, alternatives suddenly look appealing. If we could leave, so can others.

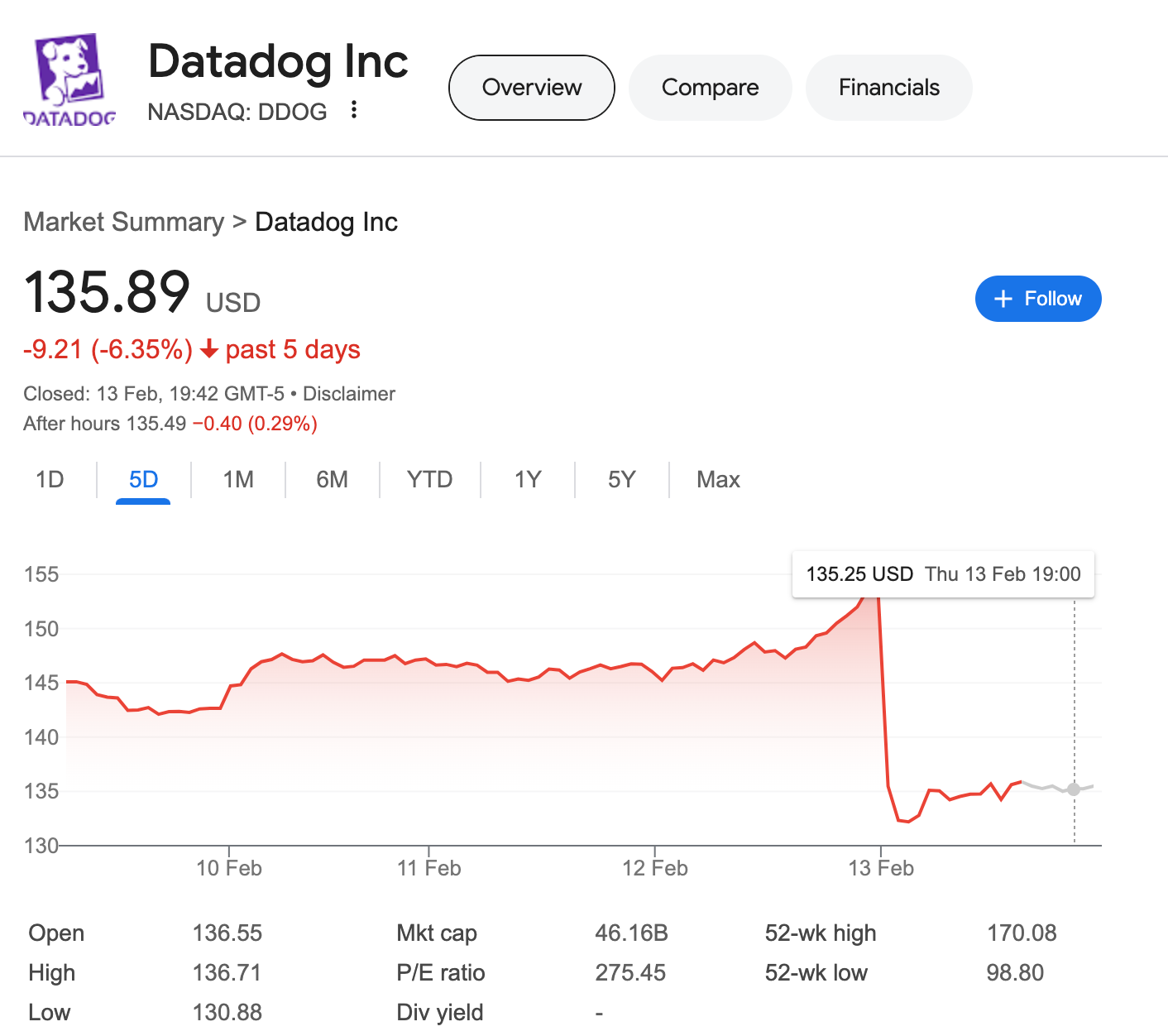

This week? A rough earnings print shaved $5B (10%) off their market cap. Still a great company, still a strong stock—but the market is unforgiving.

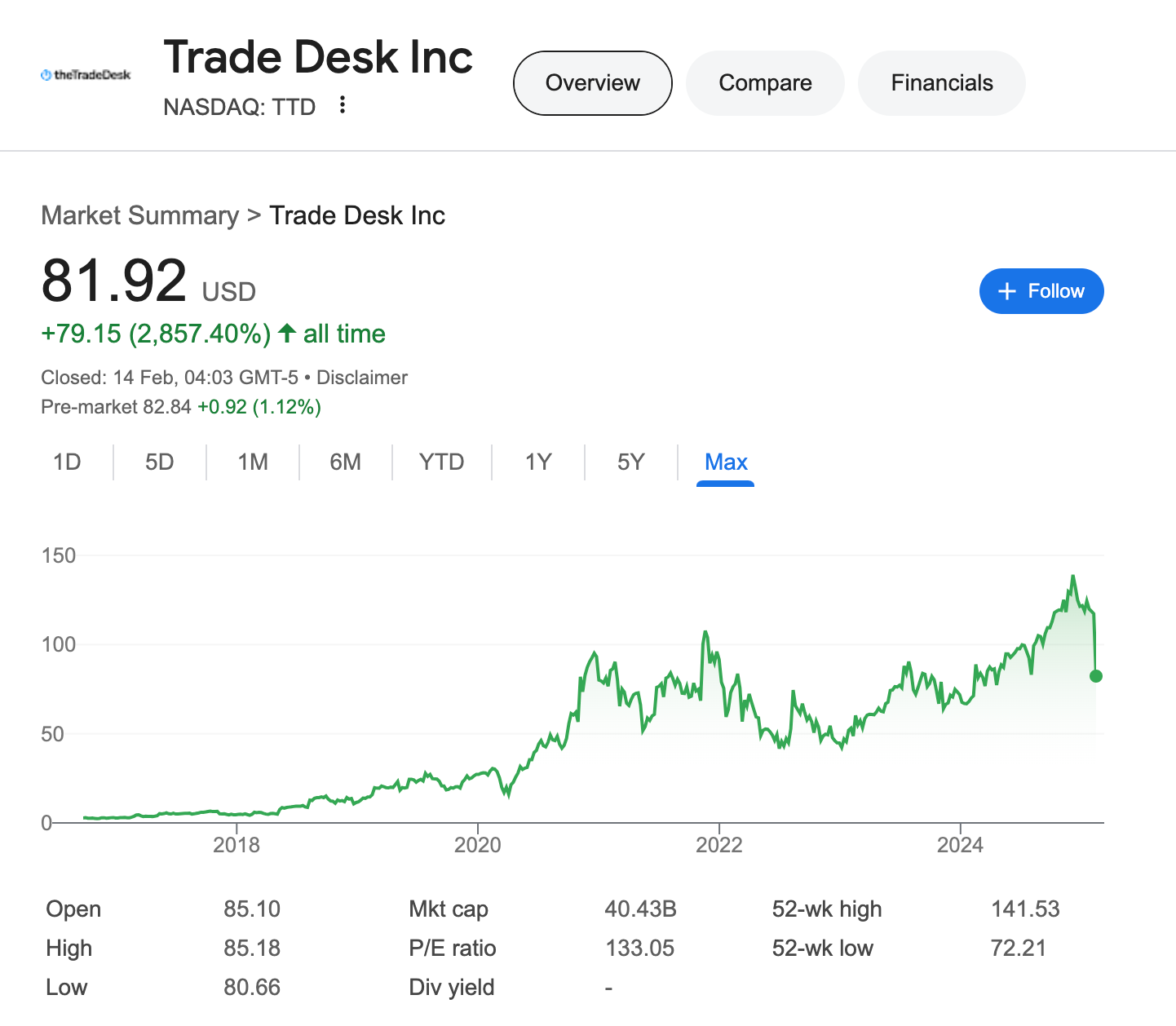

Troisième: Trade Desk – When “Priced to Perfection” Fails

Unlike AppLoving, this part of AdTech isn’t soaring, though.

When I joined my current employer, Trade Desk had just gone public. A behemoth in our space but operating in a different segment, I watched its meteoric rise from the sidelines. Eventually, I jumped in (as an investor) —buying from 2021 through 2023, then exiting my position in 20241. Naturally, the stock climbed higher, triggering mild seller’s remorse.

Meanwhile, my company tried to compete in Trade Desk’s domain before pivoting to a less crowded segment. I was on the sidelines while we were selling to the Big-6 agencies (the segment Trade Desk is great at selling to) — I found the process grueling, slow, and tough. I often wondered: How does Trade Desk do it so well? (Let’s just say I have market intel best left out of this blog.)

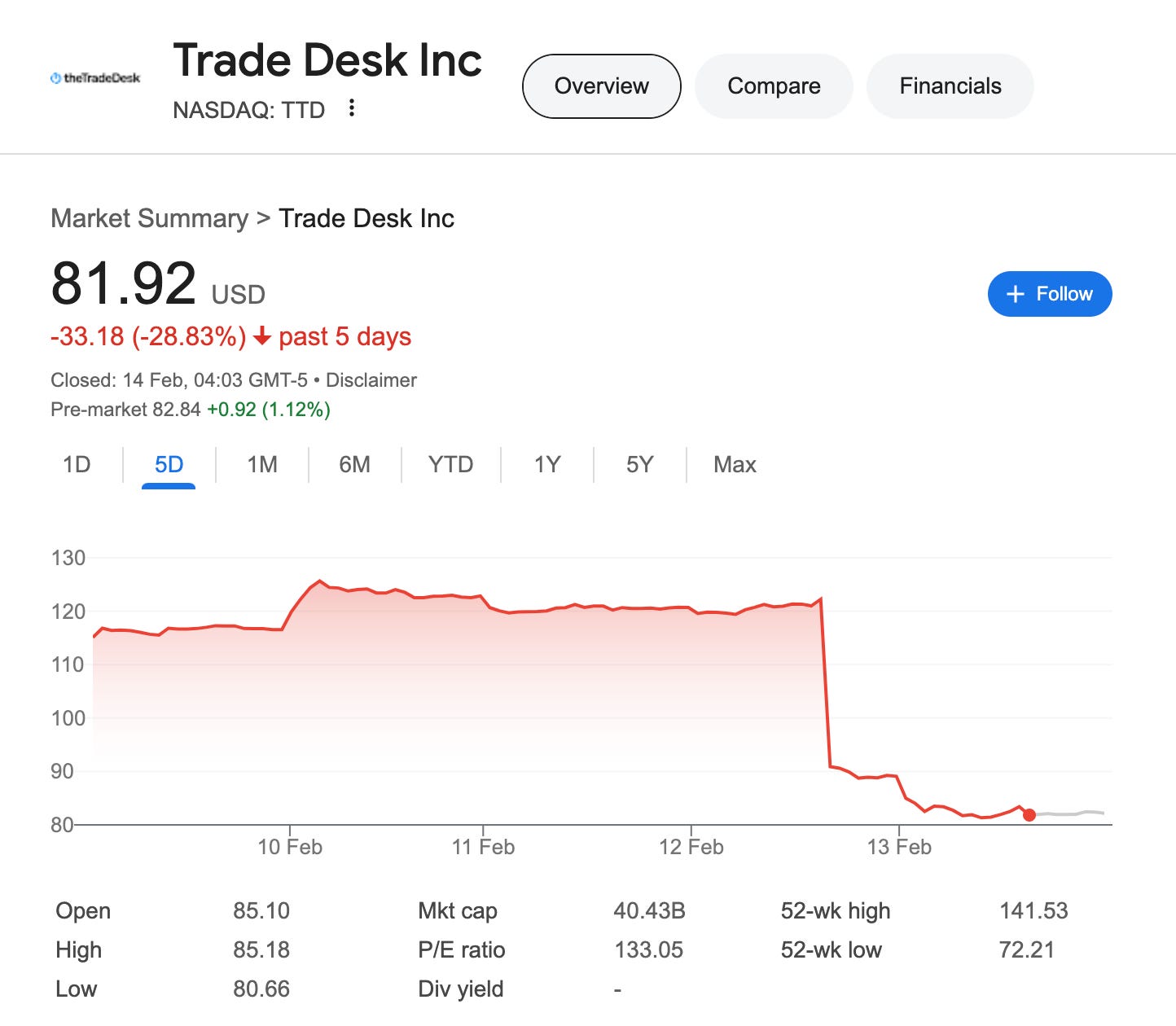

But even giants stumble. A single earnings miss wiped out a third of its value.

And yet—Trade Desk is still growing. Revenue up 26% in 2024, net income up 16%, with more growth ahead.

Pour résumer: In summary

These are all stories from the “growth” part of the market. Valuations using normal metrics don’t make sense, but there is a method to the madness of the prices here. The keyword seems to be growth and even that isn’t binary. It seems that shades of growth matter - 20% is bad, 30% is acceptable, 40% is good, 50% is outstanding. Am I getting the gradation right here?

I know that nuanced growth investors also care on the side about margin, margin growth, per-unit economics, cost of acquisition, CAC/LTV rations and so on and so forth, but growth feels like the underwriting metric. Maybe I am oversimplifying here.

In any case, I reckon the latter 2 stocks were “priced to perfection”, and AppLovin likely is today. When you trade at, say, 17x sales and 100x earnings, as TradeDesk was, every checkbox must be ticked. Miss one, and the market brutalizes you.

You live by the sword, you die by the sword. The trick for investors in these stocks is to ride that growth curve nicely. Buy when the revenue is expected to trot along at 20% and hope it runs at 40% growth. For instance with all 3 stocks, if you picked and held them for the past 5 years, you would be handsomely rewarded. For those who entered the latter 2 stocks last week, the reverse just ensued and likely got their fingers burnt. That’s the game. Know the rules, or get played.

Happy Investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.

As part of my 2024 clean-up.

APP was not spared either. After your post, there has been 46% correction in the stock in the last weeks. Do you consider this now a good long term buy?