Reviewing the Stella Jones opportunity

Let’s revisit Stella Jones (TSE:SJ) - I last wrote about the company about 18 months ago. At that time, it was the best-performing stock in my coffee-can portfolio, but since then, it has regressed to a more moderate 70th percentile. This post is a quick review of where things stand and where the opportunity may lie.

A Quick Refresher

Founded in 1992 by Brian McManus, Stella-Jones Inc. is a Canadian company specializing in the production and marketing of pressure-treated wood products—wood that is treated to resist decay, insects, and environmental factors. Its core products include railway ties, utility poles, and residential lumber. Stella-Jones operates solely in Canada and the United States.

This is a company that generates consistent, growing cash flow and knows how to reinvest effectively—both back into the business and into shareholder returns—through an ever-increasing dividend and share buybacks.

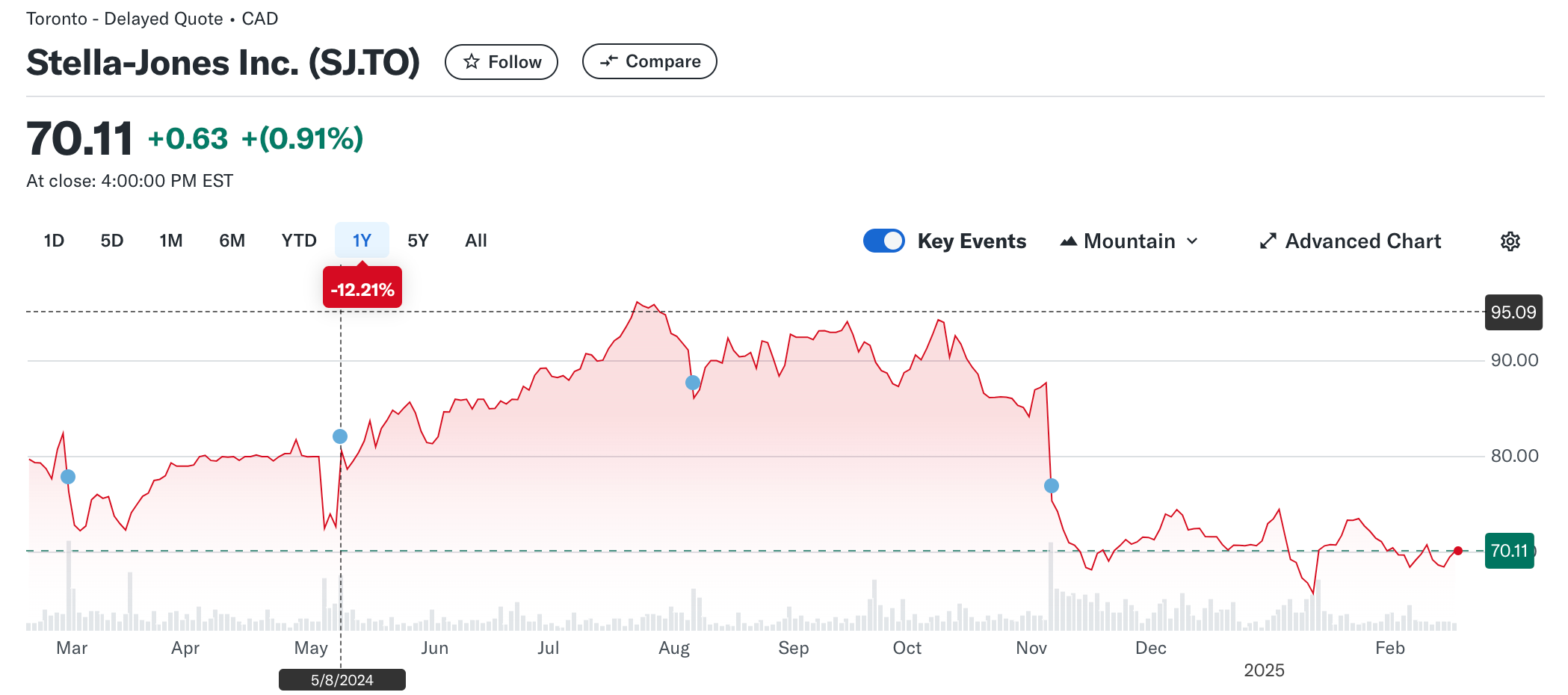

Despite what I think is a solid track record, the company has remained relatively cheap, trading between 12x-21x trailing price-to-earnings (P/E). (Emphasis on trailing—I’m taking a conservative view here and not even factoring in forward earnings, yet the valuation has still been relatively low.) Since my last post, the stock shot up to C$951 before correcting down to ~C$70.

So, What Happened?

Stella-Jones enjoys a modest valuation when it’s seen as just another steady, well-run business. But when investor sentiment heats up, it can get a bit lofty. At its previous peak of C$95, it was trading around 25x P/E—setting relatively high expectations. Then, after a weak Q3 2024 update, the stock dropped 20% and has since trended below C$70. While the quarter showed year-to-date (YTD) growth in most metrics, the company candidly pointed to a slowdown in sales growth, and investors caught on.

Here are some key takeaways from that Q3 report (note: YoY comparisons are based on Q1-Q3 over successive years):

The Good

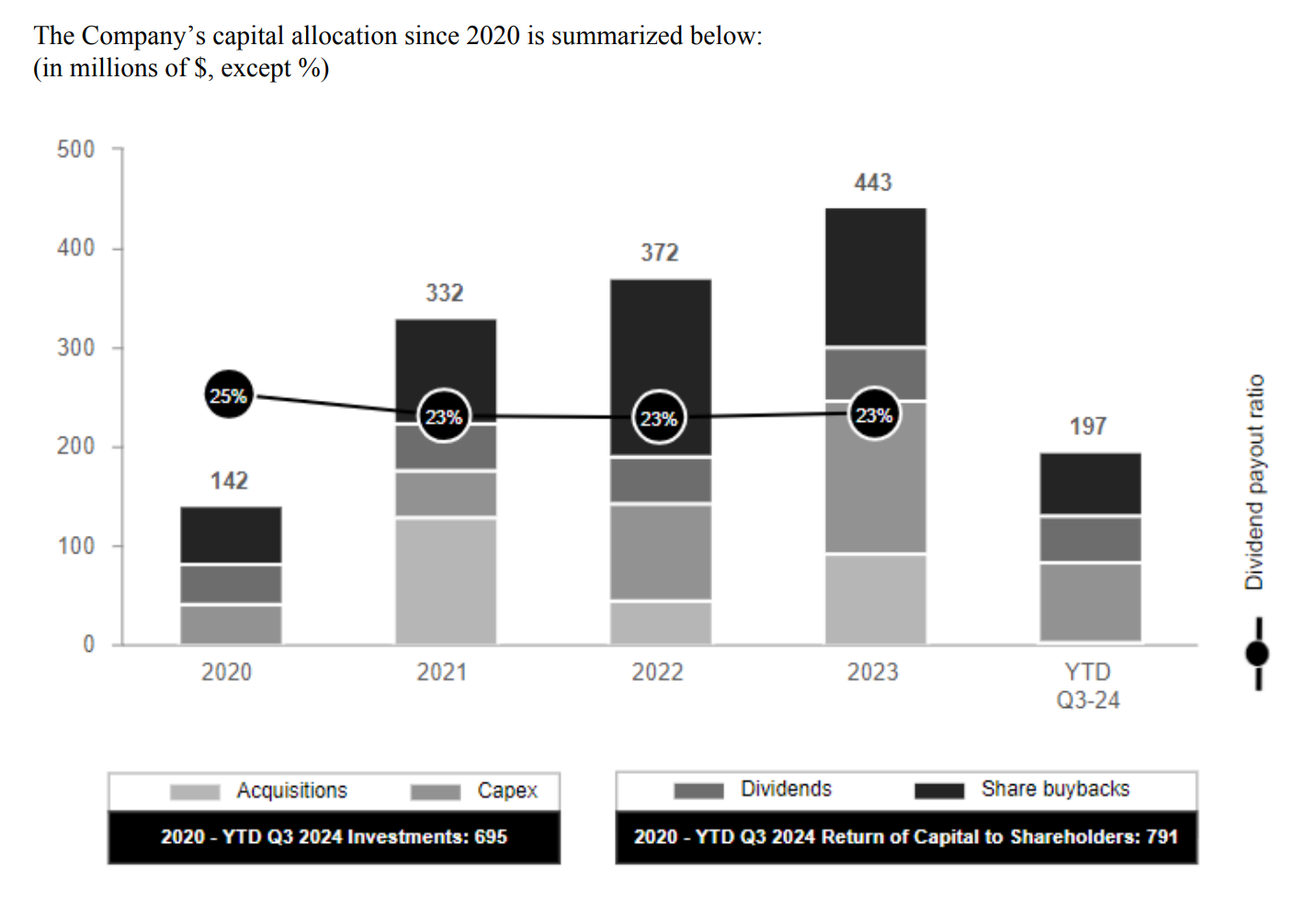

Acquisitions: Stella-Jones acquired Baldwin Pole and Piling, Balfour Pole Co., and Industree Pole & Piling, LLC, for a total of C$100M. For a C$4B market cap company, these are relatively small acquisitions but seem like solid strategic moves.

Not Too Bad

Stock Buybacks: On the surface, their 2024 share repurchases look expensive (C$85.39 per share) relative to today’s price. However, Stella-Jones has a strong history of reducing share count. Even in this costly repurchase period, the board and management deployed fewer absolute dollars (C$22M per quarter) versus previous years (which averaged ~C$42M per quarter). This suggests prudent capital allocation, leaving room for further buybacks—up to 1.7M shares—at more attractive prices.

Q3 Performance: The Q3 miss was bad, but looking at the broader picture (first three quarters of 2024), they’re holding up fine. Sales remain healthy overall, with residential lumber being the only soft spot—which was (a) expected after the COVID-era demand surge and (b) a relatively small portion of the business. Total sales grew 4%, which isn’t great for a company that has compounded sales at ~11% annually, but businesses go through cycles. I expect them to post full-year EPS of ~C$5.7 - C$5.8 vs. C$5.62 in 2023.

The Bad

Rising Debt Costs: Long-term debt has increased, and financial expenses rose from C$47M in 2023 to C$65M in 2024, suggesting that their average interest rate has likely gone up. That said, even if we adjusted for this, it would only budge EPS by ~7%—not a major factor in rerating the stock.

Overall Thoughts

The market probably got ahead of itself in early 2024 and has since corrected its view of Stella-Jones. That’s fine by me.

A company consistently generating ~C$5.6 per share in earnings without significant growth will trade more like a utility, which typically carries a multiple of 11x-12x—implying a fair value of C$62-C$69. That’s exactly where we are today. Unless Stella-Jones meaningfully declines in either sales and cash flow generation, the stock seems to have overcorrected.

Their annual report is due next week, and I suspect it will show that while nothing spectacular happened, things remain stable. A couple of tepid quarters for a well-run company isn’t a cause for concern.

I’ve increased my position by 20% this week (making it my 3rd largest holding) and won’t lose much sleep adding more if the opportunity presents itself. Hopefully, the upcoming results give us some upside.

Happy investing!

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

All numbers are in CAD in this post.