Cheap Looking Chinese Equities

Opportunity or a Trap?

The joke a decade ago used to be that Chinese products are cheap, both in price and in quality. Of course, the Chinese corrected that reputation by going further and further upstream in the quality of the products they produce, including the top end of the iPhone and EVs and so on. However, today’s post is going to be about Chinese stocks, which are seemingly cheap. The question is whether it is cheap just on price, or also in quality.

2023 has been the year of come back for global markets, with the FTSE All-World ETF up 13% for the year, the S&P 500 up a whopping 22% and Nifty in India is up 15%. After a turbulent year, most markets are now in risk-on mode, where everyone is prepping for a resumption of the 2022 bull run.

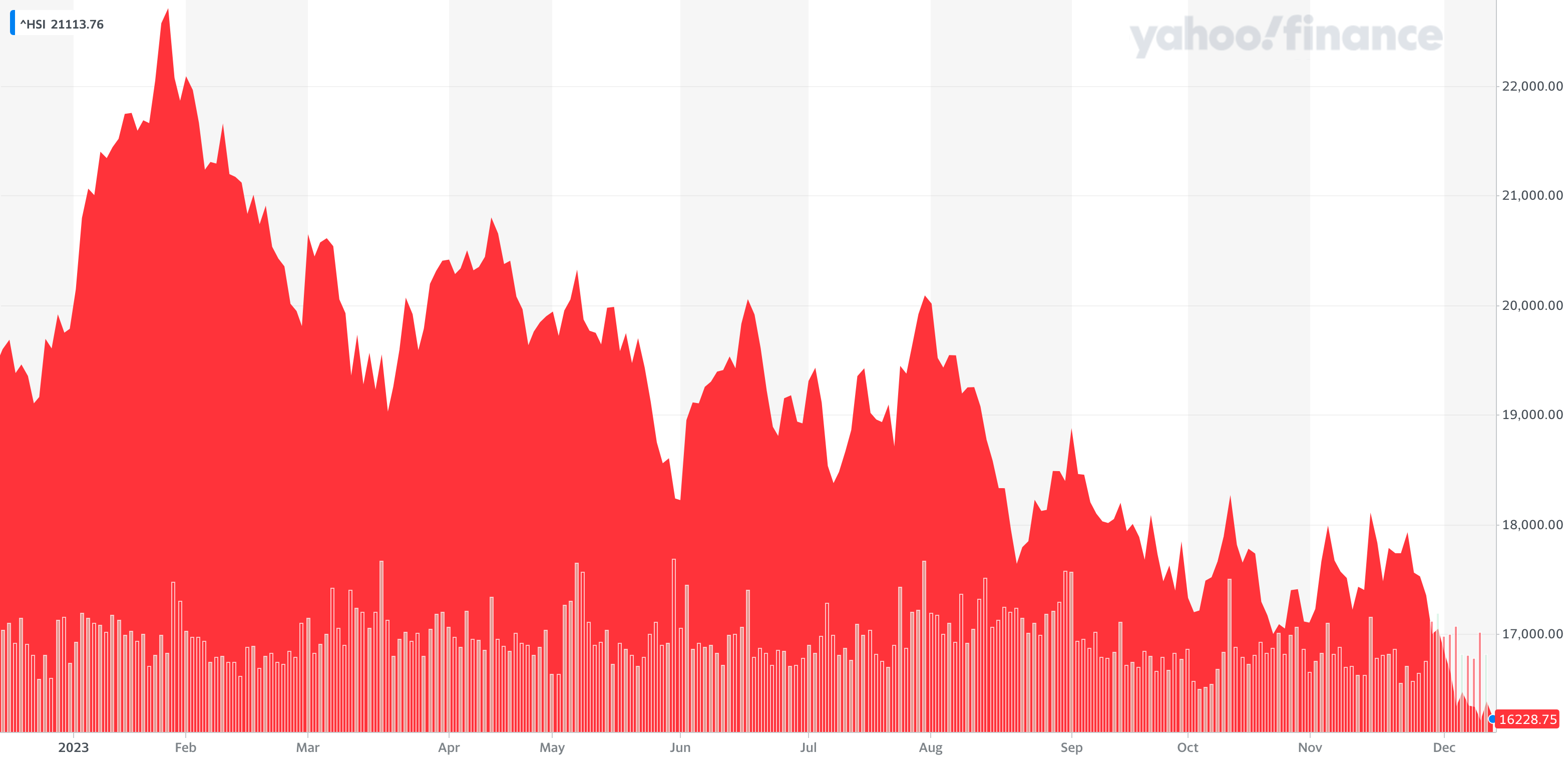

One market that has been left out of this has been the Chinese equity market, represented through the Hang Seng Index, which is down 14% and closing in on a 5 year low. the shrink is so big that India has overtaken them in market size now.

There are very good reasons for this degrade:

There are fears of deflation in the Chinese economy

Geo political fears with US moving to choke China’s role in electric vehicle supply chain

After years of being the world’s factory, major companies are trying to reduce their dependence on China, e.g. Apple.

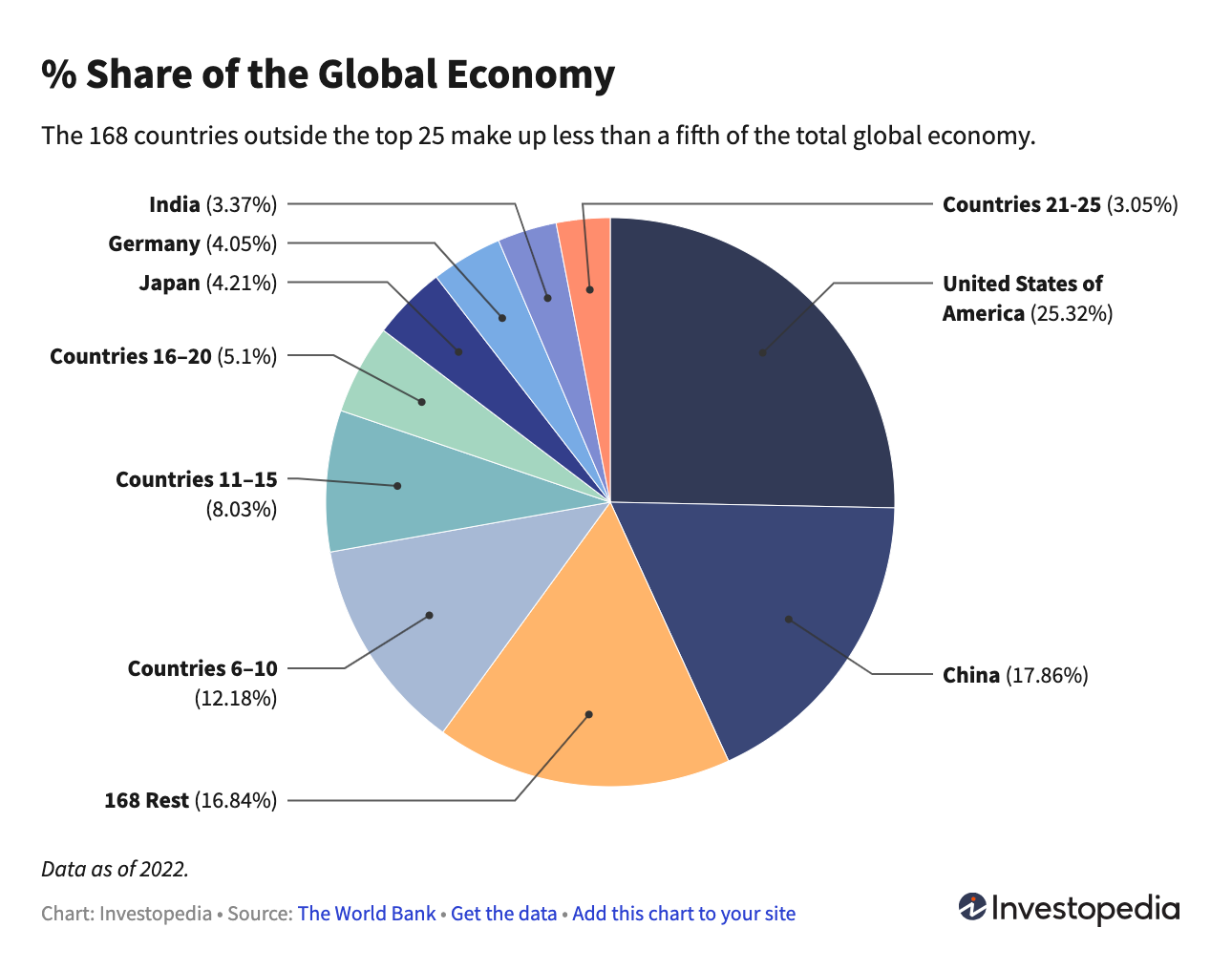

However, step in one level deeper, and things aren’t as bad. China is already the second largest economy in nominal terms, and largest in terms of PPP. They are a sixth of the of the world GDP.

A mere 3% of their economy is exports to the US. Even with the geopolitical and the globalisation fears being around, the country will likely have enough demand to keep chugging on. In fact they are already leading in climate change investments, without making as much noise as say the IRA in the US.

64 of the 82 companies in Hang Seng Index have posted declines this year. Many of the companies have had their 2023 highs either around Jan 2023, or around May 2023, both of them being market highs too. This means much of the decline in the prices are market-wide and not idiosyncratic. I am not the only one noticing it - Chinese companies themselves have noticed the slump in the market pricing and have started buying back shares in droves.

A basket approach

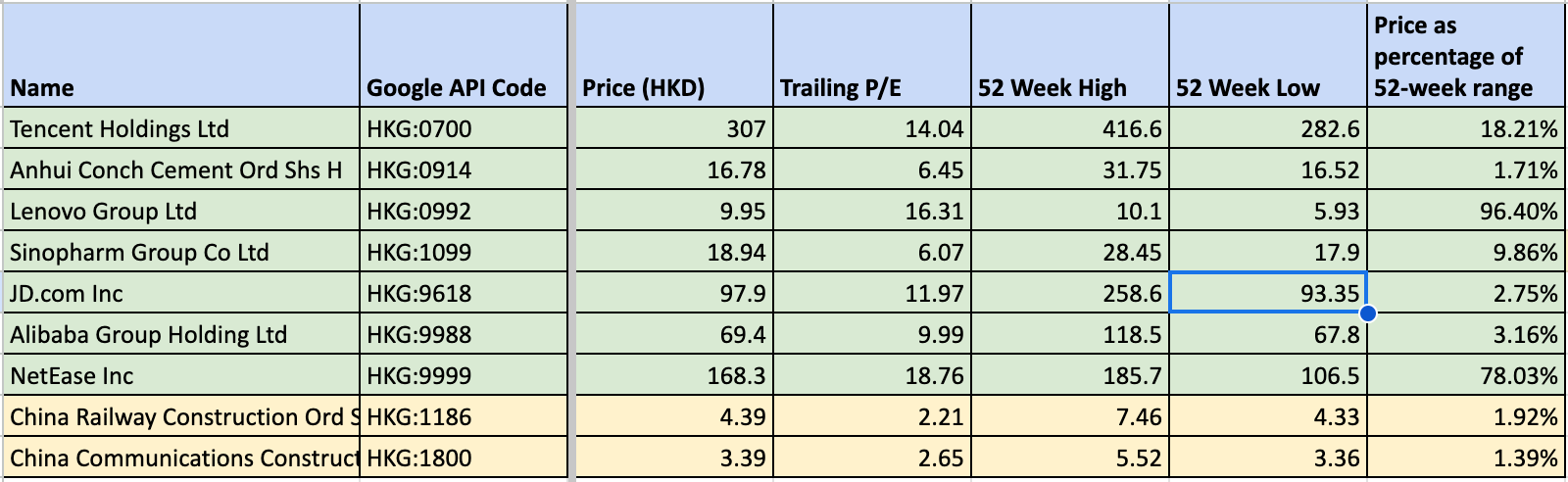

With such a market-wide decline in the prices, trying to identify the best stock to play with is largely unnecessary. We can even take a basket approach. Of the 9 stocks I own (7 of them in the Coffee Can Portfolio and 2 from outside of it) in the China/HK market, 5 are trading at PE of less than 10, and all of them are trading at PE of less than 20. Most of them are not only trading near there 52-week lows, 5 of them are trading near 5-year lows.

I have already written about Lenovo and Sinopharm recently, so I won’t go into them. Leaving aside NetEase (as it is trading well), the following 6 stocks are looking very interesting:

Tencent Holdings (HKG:0700)

Anhui Conch Cement (HKG:0914)

JD.com Inc (HKG:9618)

Alibaba (HKG:9988)

China Railway Construction (HKG:1186)

China Communications Constructions (HKG:1800)

They all come from diverse selection of industries and all of them have good track record of running their core business successfully. Aside from Alibaba and possibly Tencent, none of them is expected to get into the crosshairs of the Chinese Government, with these 2 also looking like they have managed the Government risk over the past 2 years.

This blog, however doesn’t just look at the prices and macro-trends - I like to base my decision on fundamentals. For these companies, they don’t look all that bad:

Tencent announced results in mid-November: Revenue up 10% and PBT up 6%

Anhui Conch interim results in Mid-Aug: Revenue down 10% and PBT down 30%, announced buyback in Nov.

JD.com 3rd Quarter results: Revenue up 1.7% and PBT up 6%

Alibaba.com 3rd Quarter Results: Revenue up 9% and PBT up (from a loss a year ago)

China Railway Construction interim results: Revenue up 0.1%, PBT up 1.8%

China Communications Construction 3rd Quarter Results: Revenue up 13% and PBT up 2.5%

For all the doomsday scenario, 5 of the 6 companies are printing better numbers than last year and the last company, Anhui Conch cement, with its PBT down, is still a profitable company throwing cashflow (and dividends) and is priced at 6.5x earnings offering enough margin of safety.

Put it all together and there might be a once-in-many-years opportunity to snap up assets in the world’s second largest economy, for bargain pricing. If the Chinese economy doesn’t go into a full tailspin, these stocks should re-rate in due course of time.

Will that happen? Or will these prove to be a value-trap? I will leave that as homework for readers. At my end, I am looking to buy the basket of these 6 stocks from time to time.

💡Pro Tip: If you have experience trading options, then buying pure CALL options 1 year out might be a good way to play this opportunity. The at-the-money calls for December are about 10%-20% of spot prices with tight spreads and ample liquidity - so might have some merits to it. Please note the additional risks of options trading and contract sizes. (ps: I am trying to get my head around the opportunity still, but *may* use derivatives to keep the risk low.)

As always happy investing!

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility for your actions. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.