Summary Analysis: Sinopharm (HKG:1099)

Consistent compounder available at juicy prices

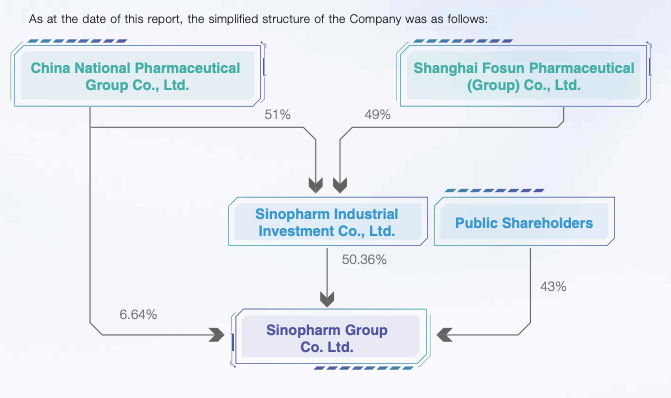

I am going to be talking today about Sinopharm (HKG:1099), the largest pharmaceutical distributor in China and a steady but constantly compounding machine. Its parent company is China National Pharmaceutical Group Corp, which is one of the state-owned enterprises held directly under the State-owned Assets Supervision & Administration Commission of the State Council.

Background & Ownership

Established in 2003, Sinopharm is involved in various aspects of the pharmaceutical industry, including R&D, manufacturing, and distribution of pharmaceutical products. It has played a crucial role in the healthcare sector in China and has gained international recognition for its contributions, particularly in the development and production of vaccines. It was listed on the HKEX in 2009.

The company has a mixed-ownership structure, with the Chinese Government controlling about a quarter, Fosun International controlling about another quarter with the rest listed on the registry as “public shareholders”, though this is likely to be a mix of institutional and retail investors.

Despite the size of the company, it is relatively a small player in China’s high fragmented pharmaceutical industry, having no more than 16% of the market share by revenue. Despite the fierce competition, with some 6,500 wholesalers, 120,000 retailers and more than 6,300 producers, Sinopharm has consistently expanded its revenue and profit base.

Demographic Tailwinds

China is going through a massive change in demographics, with one-child policy leading to declining fertility. In western countries, declining fertility has been substituted by immigration, which isn’t a big factor in China. In fact more people migrate out of China than to it, making it a net-negative-migration territory. So, the dependency ratio has moved from 35% to 47% in the past 10 years and is expected to rise to as high as 83.8%.

With this increase in dependency ratio is an ageing population that is going to tap into increasing need for healthcare.

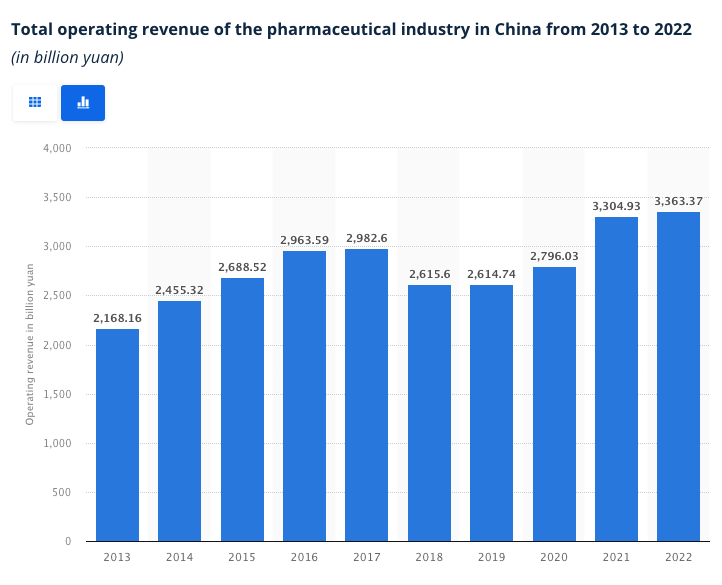

Some of the characteristics of the China’s pharmaceutical market are (a) Generic medicine dominates China’s pharmaceutical market (b) Slow rise of the China’s patented medicine market is on the rise and (c) China is one of the world’s most promising markets for over-the-counter medications. Sinopharm is well placed to capture all of these trends.

The industry was about RMB 2,100 Bn in 2013 and about RMB 3,400 Bn in 2022, compounding at 5.5% p.a. In this demographic tailwind we find Sinopharm as a well operated business to bet on.

Consistent compounding machine

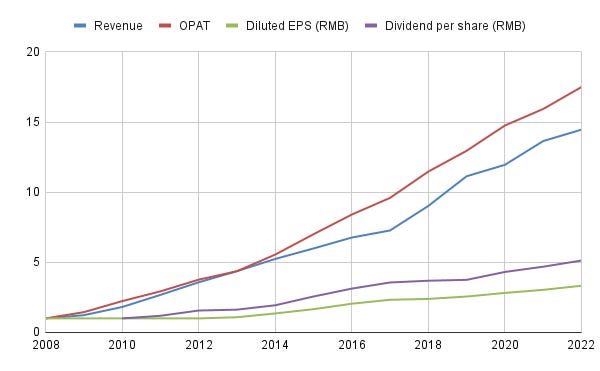

In the same time period, Sinopharm grew its revenue from RMB 166 Bn to RMB 552 Bn, compounding at 12.8%. The business has been a profit machine, going from EPS of RMB 0.53 in 2010 to RMB 2.73 in 2022, compounding at 13.4%, along the way paying some 30% out of it as dividends, while growing book value from RMB 4.81 per share to RMB 21.82 on latest print.

The increases in OPAT are not directly translated to increased in EPS, largely due to dilution in the stock base, with outstanding shares increasing from 2,264Mn in 2010 to 3,120Mn in 2022. Much of this increase has happened on H-shares and not in the domestic shares. I have dug through the reports to see where the dilution of the share count is coming from, but beyond employee and management incentive schemes, there is nothing much more of note here. It is obviously not ideal to have 844Mn shares added to the registry over 12 years, but it is likely that competition for talent has forced the hand of the management on this. Nevertheless, even with the stock dilution, as mentioned earlier EPS has compounded at 13-14% over the past 15 years or so.

The company had a lot of activity during the COVID Pandemic, issuing their own vaccine, getting a boost in revenue from the increased vaccination spend during the phase, but even after China has come out of its vaccine restrictions, it is clear that the company is continuing to print good numbers, as the 2023 interim results suggest.

We have a company, then, that is situated in an industry/market combination that has significant room for growth, is a well run business, producing consistent profits and has a desirable capital allocation record of paying out dividends while building out retained earnings and book value.

Risks

The risks of this company are not hard to spot. It (a) operates in China, a market where transparency is not forthcoming for foreign investors, (b) with a sizable ownership by the Chinese Government, whose interests might deviate from investors’ interests, and finally, (c) the possibility of a regulatory/quasi-regulatory crackdown on pricing power in the market. Of these risks, (a) and (b) are concerning, but the regulatory fear is de minimis, largely because the company extracts modest profits (ranging between 2.1% - 2.7% of revenues) and the large fragmentation in the market means that pricing isn’t getting out of hand in any case.

Even the risk of Government intervening is somewhat subdued - (i) because the company has material government ownership who can exert whatever influence they want through that ownership (and have likely done so over the years), and (ii) Pharma can hardly be compared to the tech darlings of China, who through their size and reach, pose a risk to the state.

All said and done, risks exist, caveat emptor.

Stock Price

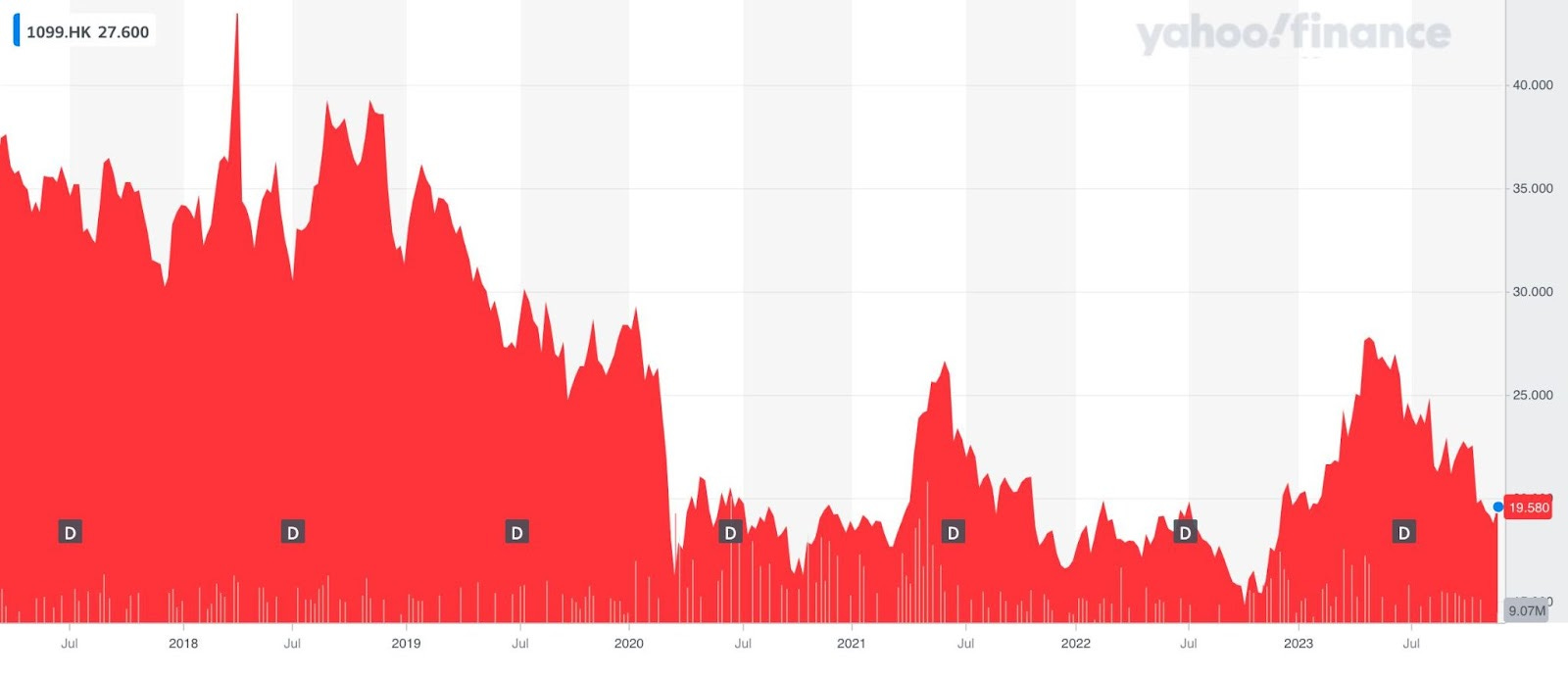

Where are we with this stock today? The stock has had a torrid time over the past 5 years, with the stock getting beaten down all the way from RMB 35 to RMB 19.5 (at the time of writing). This is despite the fact that the business has continued to grow and compound almost all business metrics owners should care for. I reckon this has a lot to do with investors’ general unease with China. Be that as it may, we investors who are looking at opportunities ground up, must make a decision on whether or not the situation warrants the attention of our wallets.

The stock, at 20 and change, trades at ~7x 2022 earnings1. The company’s interim results show only encouraging results, with revenue growing 15.1% and OPAT growing 10.7% YoY. In addition, management has indicated that certain business metrics such as expenses ratio are also improving YoY, auguring well for investors like us.

Summary

In my portfolio, this stock is currently running underwater by a little bit. However, nothing in the bullish thesis on this company has changed. With everything I have read, apart from a general anti-China investor sentiment I see little reason for not adding to this position. So I have pronto added to my position.

💡Pro Tip: If you have experience trading options, then the Feb’24 HKD 19.50 PUTs are trading at ~ HKD 1.20. With these premiums I find it a compelling opportunity to sell some PUTs. Please note the additional risks of options trading and a large contract size of 800. (ps: I just sold some PUT options this week, while also buying the stock.)

As always happy investing!

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility for your actions. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

Earnings are in RMB and stock price is in HKD. 1 RMB = 1.1 HKD.