2023 updates from some European holdings

Nothing great; perhaps time to wait out the mediocrity

Earnings’ season is almost over and a lot of companies in my portfolio have announced results that I haven’t covered yet. Maintaining my weekly cadence and picking on different topics means that I get to earnings in leisure time.

This behaviour is by design - as long term investors, we want to react less, and that means taking our time to review annual results. Coffee Can style of investing is prefaced by selecting high quality companies, which barring a disaster, will tend to report results that will follow normal distribution, for which we should be ready. That said, let’s get to some of them today.

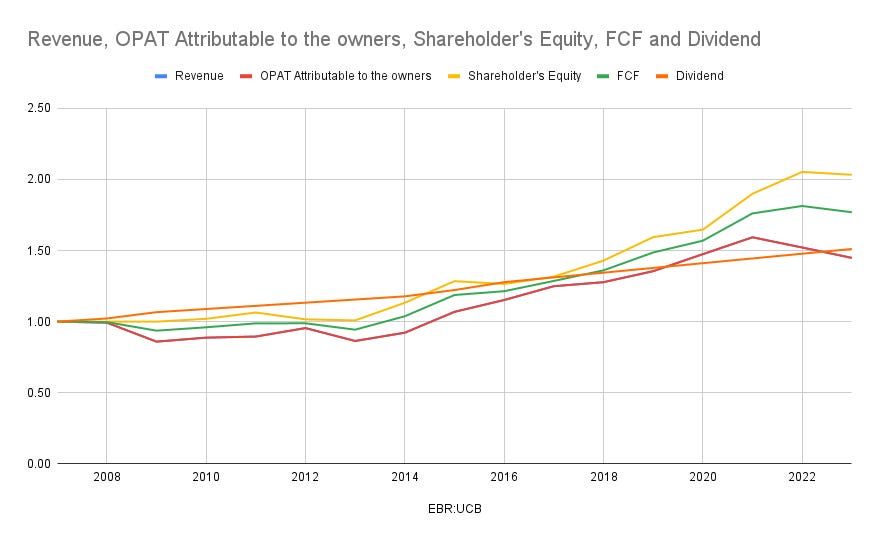

UCB SA (EBR:UCB) ❤️

Revenue net of COGS declined from € 3,843 Mn to € 3,545 Mn, and OPAT attributable to shareholders declined from € 420 Mn to € 343 Mn. Free Cash Flow declined from € 867 Mn to € 523 Mn. On per share basis, EPS declined from € 2.14 to € 1.76, and this is way below the € 5.45 declared back in 2021. 2023 was also the first year that BV per share has declined year on year in a decade (last time was in 2013). It dropped about 1% from € 46.52 to € 45.98.

However, on Adjusted EBITDA basis, the company earned € 1,349 Mn, which is marginally better than € 1,260 in 2022. I don’t like to place too much importance to EBITDA and adjustments, but it is always good to understand how management thinks about these measures and what they are adjusting for.

In UCB’s case, it is

increased amortisation due to FINTEPLA®

first depreciation charge on BIMZELX®

From Adjusted EBITDA to EBIT, there are € 53 Mn of impairment, restructuring etc (and was € 90 Mn the previous year)

From EBIT to PBT, there is finance expenses of € 163 Mn, up from € 74 Mn, “based on higher interest rates as well as higher interest cost due to higher net debt after the acquisition of Zogenix Inc. in March 2022. Also, positive FX exchange gains in 2022 did not reoccur in 2023.” as per the annual report.

For a business of these kind, these are normal, though something we shouldn’t be seeing too often. It is also worth looking at statutory numbers over the longer term to see how they fare and it seems that the company has a pretty good track record.

All put together, despite the reversals, this continues to be a healthy company, and the market seems to generally like the update.

I am going to continue to build my position in UCB.

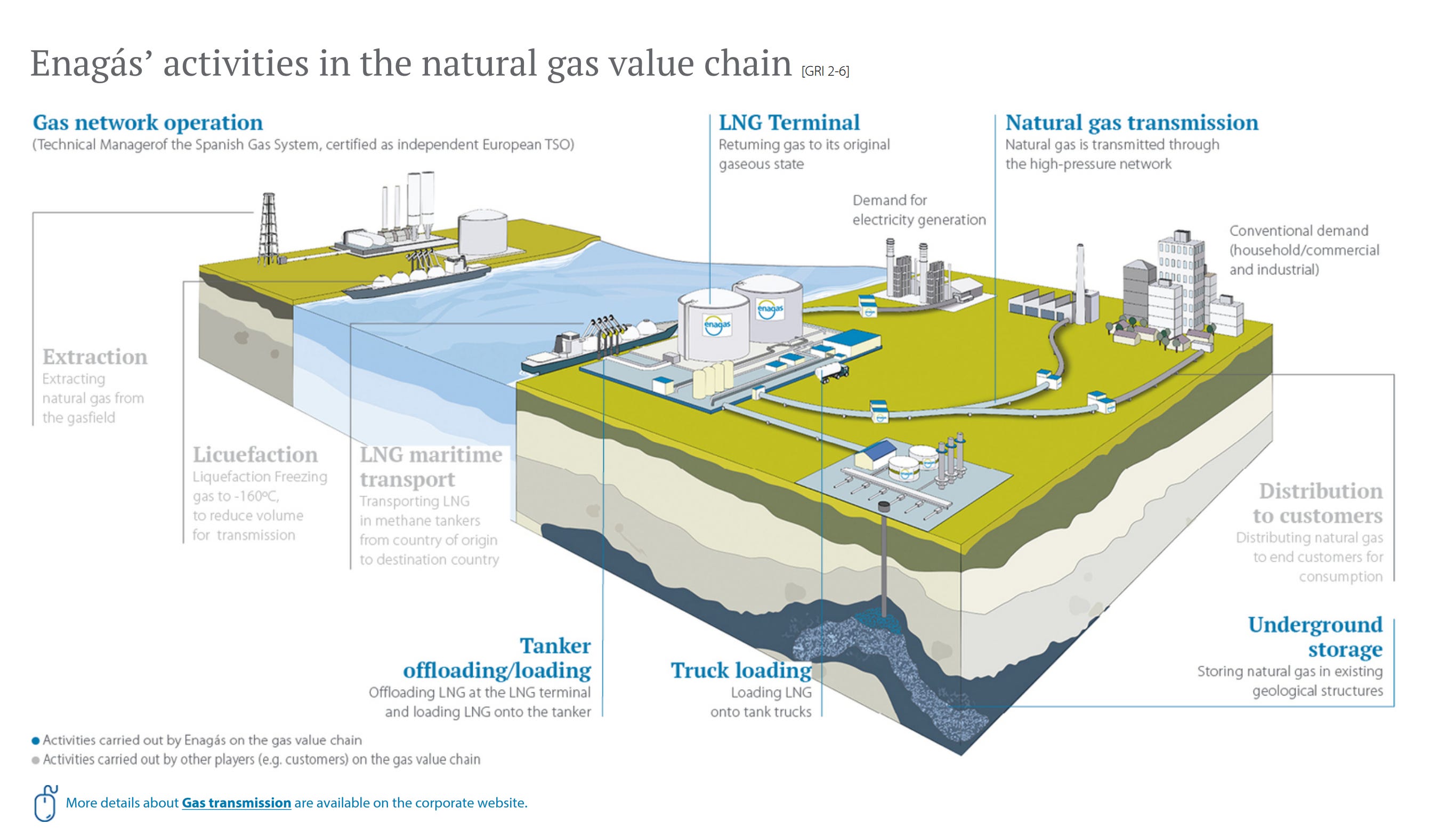

Enagas (BME:ENG) 😥

Enagás is a midstream company with more than 50 years of experience and independent European TSO (Transmission System Operator), and has expertise in the development and maintenance of gas infrastructure and in the operation and management of gas networks.

This company is part of a small set of utility companies I own in my portfolio. The idea is to have a little bit of exposure to high income yield assets that will likely not be too volatile in business performance, and being regulated, the profits are kind of sort of assured by regulation.

From that perspective I expect very little from Enagas. Yet, it was not a year where it shined. Revenue declined 5%, PBT declined 20%, FCF 35% and shareholders equity by 3.5%. It was an overall bad year and the company is now paying out more in dividends than profit after tax. Clearly, the dividend yield itself looks in danger.

Having shared a lot of the negatives, the only upside is that net debt has come down to € 3,347.41 which is the lowest it has been for at least 10 years. Despite the sharp rise in interest rates, this lower debt is being carried at a weighted average interest cost of 2.6%. So, from a debt management, the company has done well.

I am going to let this position dilute for much of 2024 to see how the company comes out in 2024 and then see if I want to build up a larger position.

Redeia (BME:RED) ❤️

Redeia Corporation, formerly Red Eléctrica Corporación, is a Spanish transmission system operator responsible for the transmission of electricity in Spain. It manages the Spanish high-voltage transmission grid and is involved in the operation and development of electricity infrastructure. Like Enagas, this is another regulated utility play in my portfolio.

In 2023 revenue up 2.4%, OPAT up 5.65%, and EPS up 4.07%. Dividend has been retained at € 1 per share, on € 1.28 of earnings, representing 6.47% yield.

In what was otherwise a positive but boring print, there was a massive drop in free cash flow, from € 1.03 Bn down to a negative cash flow of € 465 M. As per management:

This abrupt change is largely due to the refunds made of overcharges collected in previous years. The outstanding amount is due to be repaid in the coming months.

Obviously this is not ideal and has the effect of overstating cashflow in past years which we now to back out. That said, I am happy to give management a pass on a one-off basis (and this one-off basis will extend to 2024 as the management clearly calls out).

I don’t expect utilities like this to be any cause of massive outperformance, and given my low expectation, Redeia seems to deliver. Beyond the small caveat on cashflow, I am happy to own this and build on the position.

Sanofi (EPA:SAN) 🤷

Sanofi, the French pharmaceutical giant had a middling year in 2023.

Revenue increased by 2.31%, but operating expenses went up by about 15%. From Annual report2

This increase, of €1,662 million mainly reflects an increase in the share of profits generated by the monoclonal antibody alliance with Regeneron under the collaboration agreement, the principal factors being (i) increased sales of DUPIXENT and (ii) the impact in 2022 of the recognition of the proceeds arising from the restructuring of the immuno-oncology (IO) collaboration agreement between Sanofi and Regeneron.

This has led to a downward revision in every other metric worth looking at - OPAT, EPS, FCF etc. The business still produced a healthy €4.31 in earnings, and €5.72 in FCF per share, but both are significantly lower than those from previous 2-3 years. The company continues to throw out dividends, including €3.76 per share for last year, marking almost 20 years of ever-increasing dividends, and yields about 4.31% as per current stock price.

Due to the nature of funky reporting, this business often produces YoY reductions in operating income - e.g 4 of the 5 years leading to 2019 saw reductions in operating income which has since significantly improved. I don’t think there is anything great about 2023 results, but I am happy to power through for a year to see how the business shapes up and I am getting paid something to wait this out. I will take it, thought reluctantly. I will cautiously add to my position.

Fresenius (ETR:FRE) ❤️

Almost a year ago, I wrote about Fresenius Corporation. They also dropped their annual report, but it is a much harder read that usual. The good news is that they achieved the biggest hoped for outcomes for 2023 - restructuring the ownership in Fresenius Medical Care ETR:FME/NYSE:FMS (shortened to FME/FMS elsewhere in this post). The bad news is that due to this change, all their past accounts have been restated. This makes it harder to make sense of the incremental business outcome on a strictly statutory basis. So, I am going to rely on figures provided by the management on the restated basis to draw some of the below insights, rather than calculating it myself.

Revenue across the fully owned segments (not accounting for FME/FMS) grew by 6% on constant currency basis, and EBIT/EBITDA margin held at 10.1% / 15.3%. This is largely good news. Other operating parameters in the business, such as Free Cash Flow, Cash Conversion Ratio and ROIC remain healthy.

However, these EBIT/EBITDA numbers have scarcely translated into statutory profit, which has fell significantly due to one of the operating expenses3 and interest. Statutory income came in at € 353 Mn, which is 69% lower than the restated 2022 numbers of € 1154 Mn.

The company also received some € 300 Mn in state compensation and reimbursement payments for increased energy costs4, which means the company cannot legally distribute any dividend.

When I wrote about this company last year, I called out the restructuring of the FME/FMS shareholding and the restructuring as major challenges that the management needs to address. Progress has been 100% on the former and notable on the latter, but this has meant poor visibility into their statutory accounting (forcing investors to look at EBIT/EBITDA metrics) and the temporary suspension of the dividend.

I am going to continue to be cautiously optimistic about the company’s prospects.

Summary

In choosing European companies, I signed up to share some depressing results, as Europe in general has had a tough 2 years or so, and no major economy seems to have picked up pace since some of the own-goals from the Pandemic era, made worse by Russia-Ukraine war. These 5 companies however only represent 6.4% of my Coffee Can Portfolio, and are collectively in the profit in my books (marked by a significant uptick in UCB). I will continue to hold them and slowly add to my positions, more to Redeia, UCB and Fresenius and less on Sanofi and Enagas.

As always, Happy Investing!

“thanks to the strong performance of working capital due to the premiums collected from the increased utilisation of LNG terminals in 2023” as per management

With some paraphrasing sourced from Page 72 of the Annual Report

“The gross margin decreased to 22.7% (2022: 25.1%). This was mainly due to the transformation of Fresenius Vamed, legacy port- folio adjustments, expenses associated with the Fresenius cost and efficiency program and an inflation-related in- crease in the cost of revenue.”

through Hospital Financing Act (“Krankenhausfinanzierungsgesetz”)