The continuing case for India

The best economy in the developing world

A year ago, I wrote about the investment case for India and China. In hindsight, I should have stuck to just making the case for India, and would have looked like an absolute genius. Since writing that post, Nifty, one of India’s primary indices has grown by about 28%1!

I am just about completing my latest trip to India and I want to make a few quick observations.

India’s Economy ❤️❤️❤️

The Indian economy is on an absolute tear. These are some of the news articles I came across in a few days here:

Sales of Passenger Vehicles to grow ~10% yoy, and SUVs are now the highest selling segment

Airport’s Authority of India is growing its revenue circa 25% and doubling it’s post-tax profit

Railways is seeing it freight increase by 5% and profit by ~10%

India’s credit ratings are all getting better with upgrades following on the heels

Within less than a generation, India is aiming to be a developed nation

A slowing growth in India means 12%-15% growth - as is the case with eCommerce in India

By no way is this a scientific treatise, but it is clear from multiple observations that India’s economy is growing fast (~10%), and that translates to about 7% in per-capita terms, on USD basis!

India’s Financial Structures ❤️❤️❤️

In the UK, pension funds hold under 2% of their corpus in UK securities and retail investors fare no better. Sentiment in the UK for investing in locally listed companies is extremely low. India stands in dark contrast2.

Often India’s innovation in UPI is mentioned as a big success3. While that is the case, what’s not as celebrated is the quite revolution in retail investment sentiment fostered by excellent regulatory environment.

Through efforts like (a) Retail IPO Book building, (b) Prevention of naked shorting (which avoids things like gamma squeezes), (c) Application Supported by Blocked Amount (ASBA) in IPOs, and (d) widespread promotion of Mutual Funds through the “Mutual Funds Sahi Hai” campaign, Indian regulator SEBI has done a fantastic job of getting retail investors to invest and stay invested4. The rise and rise of Portfolio Management Services (PMSes) have followed this arc of success.

A healthy ecosystem for retails attracts enough institutional investors, as well as foreign funds who have poured money into India5.

A Stable India ❤️

India’s political setup is stable, and is likely to stay the same after the upcoming elections - there is little threat to the continuity of the current regime.

If you however take a step back, since Liberalisation, Privatisation & Globalisation reforms were unleashed in 1991 by the then Prime Minister PV Narasimha Rao6, every government has effectively carried on the path set out by that change, be it his party Indian National Congress, their primary opposition, BJP, which is now the party running the government, or the fringe parties in the form of United Front.

Parties and Governments have varied in their execution and how much they publicly supported that ideology or for what reason, but the core economic policy regime has been more or less the same. When you have the right policies in place and let is compound for 30+ years, you are bound to get good results.

In fact, if you look at economic indicators of the 21st century, it is becoming very clear that the (i) US in the developed world and (ii) India in the developing world are shaping to be the large, performing economies with good long-term tailwinds.

The only other country that came close to either of the two was China, but Chinese rule-makers have chosen to score too many own goals. To add, unlike China, the other big developing world success story of the same time period, India has more predictable governance structure (or put another way, less anarchy), and far less geopolitical risk.

All this bodes well for long term investors.

Valuation Risk 😕

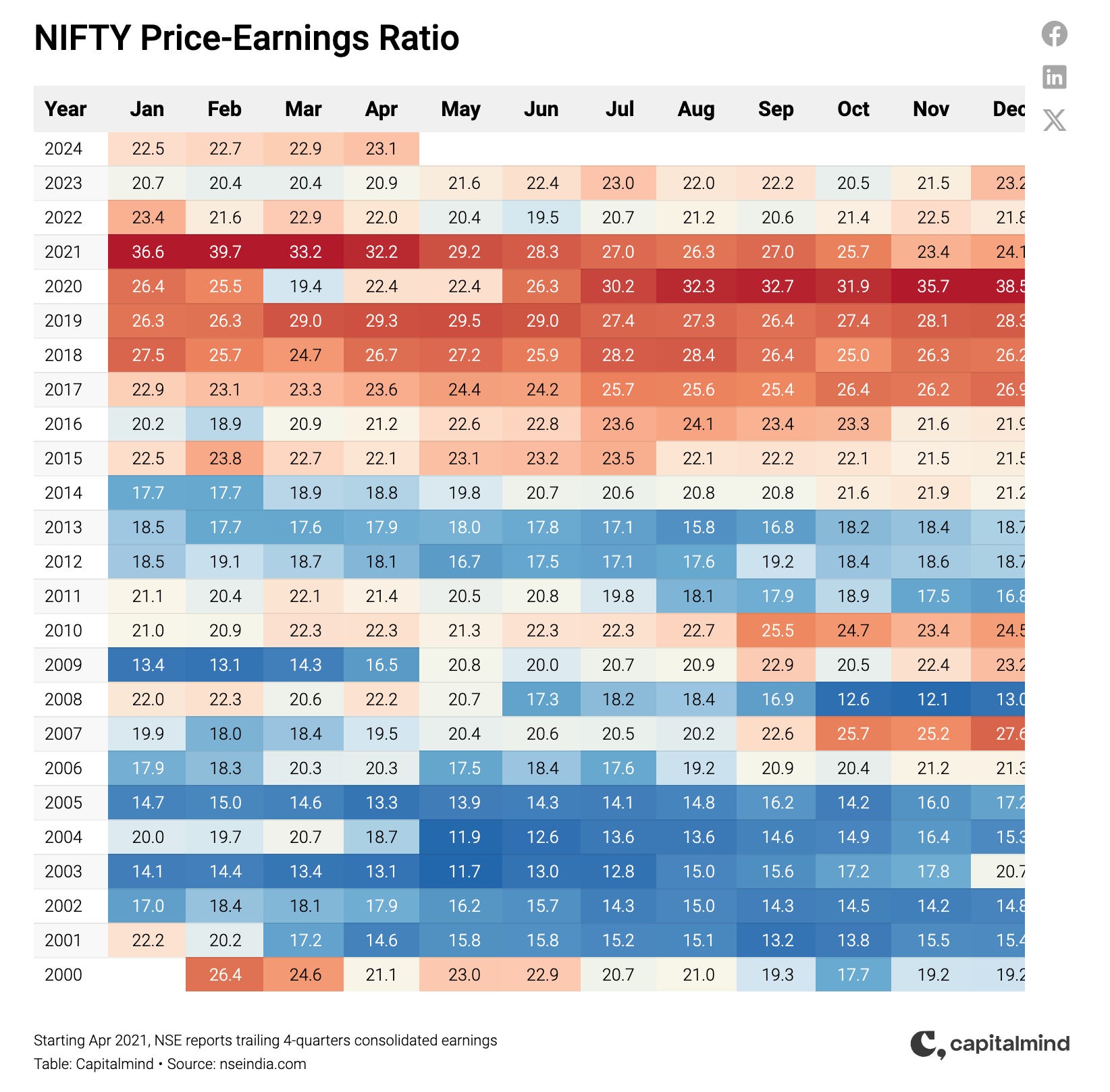

The big risk then is around valuation. Like any other vibrant stock market, the Indian market is prone to more frequent greed and fear cycles, causing possible drawdowns in the short to mid term. The current run-up in the markets make this a more real possibility within the next 12-18 months, though the market is still well under its 21st century peak in terms of valuation, which was achieved in early 2021.

Invest in India

Due to historical reasons, I have India holdings sprinkled across multiple forms - mutual funds I have held for almost 2 decades as well as ETFs listed abroad. At the moment, the concentration of my India portfolio is around these three foreign listed ETFs:

iShares MSCI India Small-Cap ETF (BATS:SMIN) - listed in the US, and trades in USD and it tracks the MSCI India Small Cap Index, and holds about 486 small cap stocks. This has gone up 45% in the past year and doubled in the past 3.5 years!

iShares India 50 ETF (NASDAQ:INDY) - listed in the US, trades in USD and it tracks the Nifty 50 Index. This has gone up 21% in USD terms over the past year (roughly in line with Nifty’s movement, adjusted to currency movement in the said time period)

iShares MSCI India UCITS ETF USD Acc (LON:IIND) - listed in the UK trading in GBP, or as LON:NDIA in USD, and it tracks the MSCI India Index and holds about 136 companies. This has gone up 32% in GBP terms over the past year. This is also the ETF mentioned in my Coffee Can Portfolio.

Summary

✔️ An economy that’s firing on all cylinders

✔️ A financial environment that’s conducive of healthy local and foreign investment

✔️ Continuity in economic policy, across multiple political regimes

❓ Possibly rich valuations - fair risk of drawdowns in short to medium term

I am starting to think that my allocation to India is too little. Perhaps time to up it? I will look to build up a larger allocation over the next 12-18 months.

As always, happy investing!

ps: If you are new to the substack, a recent post that garnered a lot of page views is - perhaps worth a few minutes of your time?

Disclaimer: I hold positions in some of the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

Painfully, China has dropped by about 18% or so in the intervening period! 😥

Part of the contrast exists because Indian regulations make it extremely hard and unfavourable to invest abroad, or rather take the Indian Rupee out of India and put to use. So, institutional investors as well as retail prefer to deal with less hassle by investing locally. However, I don’t see anyone clamouring to send their money abroad as the local economy and the market is doing perfectly fine.

The Capitalmind Podcast is an excellent source of content on these topics.

But there is enough local bullishness if they pared back.

Despite initiating the greatest economic revolution in modern Indian history, his own party has disowned him for lack of loyalty to the political dynasty. Since I don’t want to bring in a political angle to this blog, I suggest the book Half Lion, by Vinay Sitapati as an excellent nuanced read on this topic, where he draws both the rights and wrongs of the PM’s policies during his single-stint tenure.

Well summarised Srini 👏👏