The Case for India and China

Two wonderful economies with abundant opportunities

I have just about completed a fortnight long trip to India - my first visit since the pandemic broke out. It is evidently obvious that India has a palpable economy energy not found in the western world, and definitely not in the UK. New products are getting innovated, new infrastructure is being built, new services are being formulated and to counter it on the other end, a consumer class that is exploding both in unquenched thirst and aspiration for anything and everything that can be produced.

I gorged on economic and business news in India all throughout the trip and the measures of successes and failures are just out of the park. Compensation consultants in IT sector think 8-10% salary hikes are disappointing, a car manufacturer is deeply disappointed by the mere double digit growth in some segment, and money is flowing left, right and centre into everything - new age startups, traditional heavy industry, re-discovered service businesses and last but not the least commodities and energy1.

For a long time the fear of many Indian commentators was that India’s growth will yield more and more of the economy into the hands of western companies, thereby leading to a version of economic colonialism. On-the-ground truth can’t be further from the truth. Take beverages for example - there is no shortage of newly generated Indian drinks - Lahori Jeera, Arora Lemon, Vibro Paneer etc all of which are genuine Indian innovations fighting tooth and nail with the Pepsis and Cokes. This isn’t true just in this segment, but visible all through the economy. Economic growth will likely be some hybrid version, as MNCs take a few steps forward, but equally matched if not overtaken by genuine Indian innovation and both are good things for the local society.

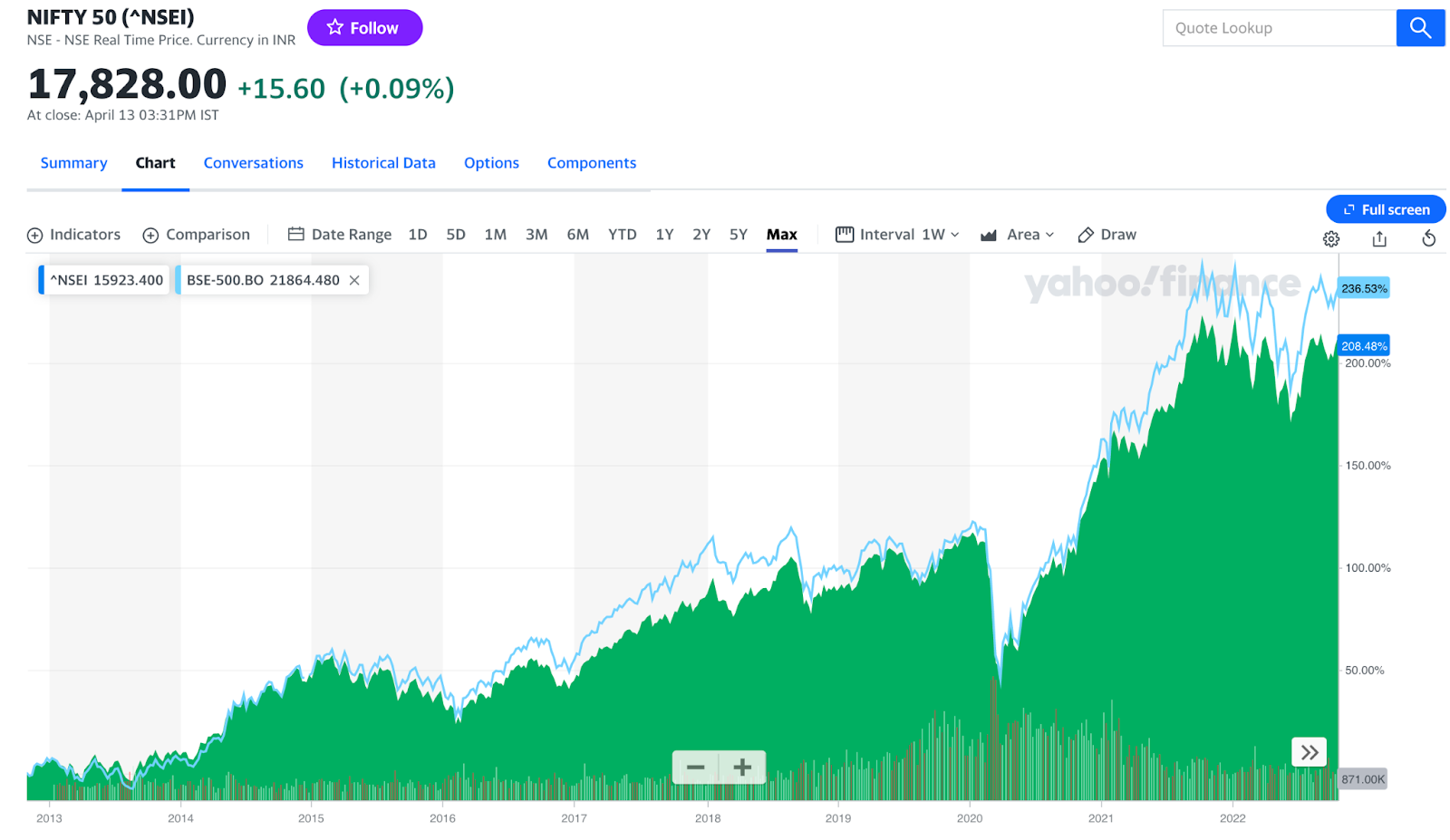

Inflation adjusted GDP growth is humming along at 6% on the long run and will likely continue to be around that, whereas the western world has done just about 2%. This growth in the economy has amply spilled into the stock market, returning some 12-13% depending on the index you choose.

Let’s move over to China, the other economic powerhouse. Driven by domestic demand and a robust expansion of economic activity both for external and internal consumption, China continues to power along on its economic progress. While I have 0 first hand knowledge of China, whatever you hear and whatever you read in the reports indicates a similar story as India, just on steroids, as the political structure in China allows them to move faster than others when the direction is known, which at this point, is largely clear to the aficionados in the Middle Kingdom.

The zero covid policy and the recent regulatory attacks on big-tech both seem contrary to that narrative, along with the fear of geopolitical concerns. However I am confident that the long term incentives for everyone making decisions is aligned in the right direction, so I expect these to be minor hiccups along the way, while China will likely press on with as much peace dividend as possible.

Investment Opportunities

Any well balanced portfolio that seeks returns in the long run is likely better off having a reasonable representation of both these countries and the economic potential presented thereof. Not only does the opportunity for massive growth present itself, it is also likely to stay somewhat uncorrelated to the rest of the world, providing net additional value, both in terms of diversification and returns. My current Coffee Can Portfolio maintains about 24-27% between these two markets2.

Indian companies have not been very interested in listing abroad through ADRs and GDRs so the choices for tapping into Indian potential from a brokerage account outside India is somewhat limited. With that in mind, I capture the India trade through IIND (ETF representing 100+ stocks from the MSCI India ETF), Reliance Industries and SBI.

IIND’s case is easy - it is an index broadly representative of the growth opportunities, trading at roughly 20x P/E. Reliance industries is a large conglomerate operating in various industries, but primarily acts on the energy input side of the economy3, and SBI, the largest public sector bank in India, represents the opportunity to tap into the financial trade of economic growth. Between these 3, I am confident I have enough of the upside locked in, while I retain the option to revisit the mix as more Indian companies list outside of India, or better still, India opens up its markets to more investment routes than today4.

China is slightly different - through HK listed tickers, the primary means allowed by Chinese government for foreign retail investors to invest in Chinese companies, you can find a plethora of options to invest in Chinese tickers directly5. I have chosen the following tickers, a broad representation of Chinese opportunity, across commodities, retail, tech and pharma.

Interestingly, of all the markets I am invested in, China represents the best value, trading at 0.35x P/S, 9x P/E, compared to 1.1x P/S and 15x P/E for my whole portfolio. By almost any metric I can see China is cheap. Either the metrics are all lying or the markets are mis-pricing the opportunity big time. I am betting on the latter and will likely continue to load up as I see further good news coming from the market.

What’s your allocation of Investments in the two most populous countries in the world?

It is a rather uncomfortable truth that India (and China) know very well that if they were to march along the progress that their countries need to necessarily chart to go from Developing to anywhere close to the Developed status, they need access to commodities and energy, and while both countries are pressing the accelerator on renewable sources, they are perfectly comfortable tapping on existing sources to keep the taps of energy running.

My coffee can portfolio far underrepresents the Indian allocation, and that’s largely because I have investments in India outside of the Coffee Can portfolio - mutual funds etc collected over the years. New investors with no such investments might be better served considering an allocation of between 8-10% in India and 12-14% in China.

57% of revenue is from "Oil to Chemicals" segments

As a non-resident India I can still invest in Indian markets directly through the NRI route, but that is a constrained environment, allowing only cash settled trades, and needs a separate brokerage than everything else I am using now. I am being a bit lazy in not choosing to go through the hassle of dealing with another set up, but that might very well change in the future.

There is also a QFII route to invest directly in A-shares (on Shanghai exchange), but those are not available to retail investors. While there are regulatory concerns regarding Chinese ADRs, my expectation is that HK listings won't be affected by that tug of war as China would like to use the HK route to tap into foreign capital.

Very good points Shree, fully aligned on the rationale for both China and India (although long term I am more bullish for the latter).

I am currently invested in these two ETFs (both 8% allocation each) -- curious to see if you recommend different ones?

iShares MSCI India UCITS ETF USD Acc (GBP)

iShares MSCI China A UCITS ETF USD Acc (GBP)

Great article. Although I wonder on China if it is investable at all for non Chinese nationals.

I thought long terms returns have been very very poor even when China has been growing fast. Only returning about 1.9% per annum over last 30 years even when dividends are included:

https://www.schroders.com/en/insights/economics/two-charts-that-show-why-you-should-ignore-chinas-index/

First we have the appropriation risk with Government completely capable of taking over economic resources of any Company.

Note that this risk also exists in UK with so called Windfall taxes resulting in Harbour energy's profits being completely appropriated by government this year hence why UK stock market is tanking and everyone is thinking of moving to US.

Secondly even if this was not to happen it is not clear what return route would be. Would these companies ever pay enough and reliable dividend to justify the investment, probably not.

Government wont like it and neither would the entrepreneurs. They would probably find a way to stop it.

Investment into China has to be seen from the prism of above two considerations more so than perceived value or cheapness.