Summary Analysis: Agnico Eagle Mines (TSE:AEM)

A well run gold miner

There is a sudden outburst of interest in commodities among the investment community. Despite my rather insignificant existence in this world, I have had at least 3 fellow investors reach out asking some or the other details about Gold or Silver ETFs1. I try and avoid following too many trends, instead focussing on building a portfolio that can stand the test of time. With that in mind, precious metals were already a small part of my portfolio. I have previously written about gold. Today I want to speak about a (primarily) gold miner.

One of the relatively smaller, but better performing companies in my portfolio is Agnico Eagle Mines (TSE:AEM / NYSE:AEM). AEM is a Canadian gold mining company headquartered in Toronto, Ontario. Established in 1957, the company has grown to become one of the largest gold producers in the world.

Agnico Eagle Mines Limited was first listed on the Toronto Stock Exchange (TSX) in 1969. The company subsequently expanded its public listing to the New York Stock Exchange (NYSE) in 1978.

The company's primary focus is on gold mining, although it also explores and produces other precious metals like silver and zinc. It operates several gold mining projects and properties in Canada (LaRonde, Meadowbank, and Canadian Malartic mines), Finland (Kittilä mine), and Mexico (Pinos Altos and La India mines), among other locations.

Past Performance

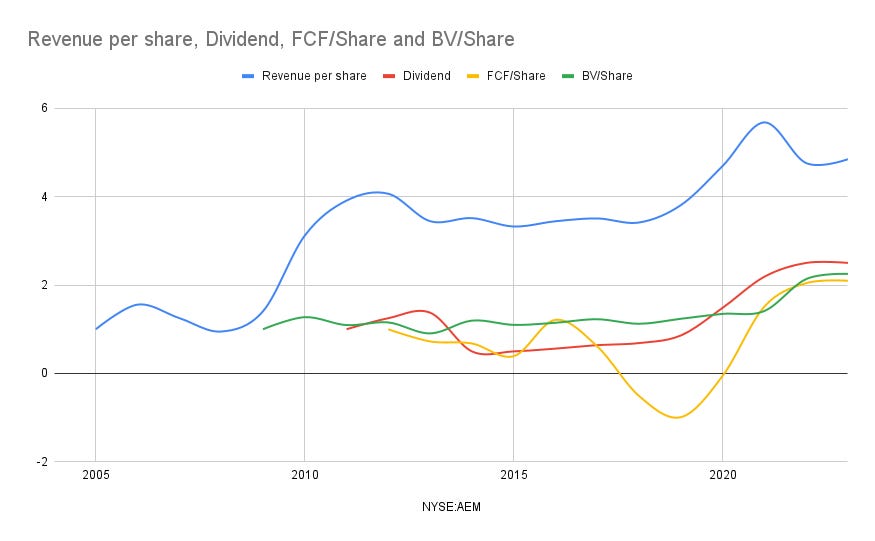

In terms of finances, over the past 15 years, the company has been growing its revenue per share2 at about 11% per year, EPS by 14.77%, FCF per share by 5%, and Book Value Per share by 5.97%. Dividends have been consistently rising, hitting USD 1.6 per share.

Agnico Eagle Mines has been recognised for its operational efficiency, high-quality assets, and commitment to safety and environmental stewardship. The company’s consistent performance and growth strategy have made it a respected name in the global mining industry. In summary, the kind of company long term investors like us should be looking to own.

Acquisitions and Growth

Over the years, Agnico Eagle has expanded through strategic acquisitions and continuous exploration efforts to increase its reserves and production capabilities, most recent of which was Kirkland. Completed in 2022 the deal provided Kirkland Lake Gold shareholders 0.7935 of an Agnico Eagle share for each Kirkland Lake share they owned. This acquisition brought in 100% interest in mines such as Detour Lake and Macassa mines in Ontario, and the Fosterville mine in Australia.

In a 2023 transaction, AEM acquired Yamana’s remaining3 50% share of the Canadian Malartic Complex, a 100% interest in the Wasamac project, located in the Abitibi region of Quebec, and several other exploration properties located in Ontario and Manitoba. They paid about $1Bn in cash plus 36Mn shares of AEM.

Across these transactions, AEM diluted its share count from 245M at the end of 2021 to 497M at the end of 2023. Revenues have gone up from $3.9Bn in 2021 to $6.6Bn in 2023. Mergers are always tricky, especially large ones like the AEM-Kirkland ones, but so far, it seems it has gone relatively well, evidenced by the good growth in per-share financials.

Relationship to Gold

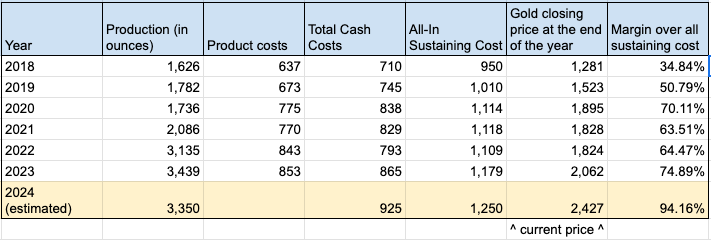

Producing an ounce of gold requires a significant amount of capital investments as well as material operating costs. A company like AEM regularly publishes these numbers. In 2023, it took about $1,179 in all-in sustaining costs4. The costs of producing an ounce of gold is relatively stable, after factoring in inflation. However, the spot price of gold changes from year to year. Therefore, the gross-markup the company can charge depends on external factors - i.e. the price of gold, but the costs of production are more or less fixed. The company's fortunes therefore vary significantly with gold price - and the share price bobbles up and down in a levered manner with the change in gold price. These 1 year, 5 year and longer term charts tell you the story of this relationship.

Given this fractious relationship to gold, shouldn’t we prefer holding gold itself? Maybe, which is why I have gold. However, I like AEM as a company and while I am conscious of the relationship, I am happy to treat my stake in AEM as a company with a good track record and able to produce stable returns and an ever increasing dividend payout. If the company didn’t depend on large acquisitions like the Kirkland one to grow, and instead chose smaller, organic additions, I would be happier, but in balance, they seems like a reasonable hold in the long term.

The company also provides an optionality into plays on other commodities such as copper, nickel and zinc. From their annual report:

While the Company’s primary focus is on gold, it monitors opportunities and considers the exploration, development and mining of, or investment in companies that focus on strategic and critical metals including copper, nickel, and lithium.

For what it's worth, as it stands, AEM on a dividend-included basis, is outperforming gold by a few percentage points in my portfolio.

Comparison to peers

I have not looked too deeply into all of AEM’s competitors, but it seems that all of them have generally volatile times in the market and AEM has outperformed both on 1-year and the long-term horizon, while also losing out barely on the 5-year term. Not perfect, but a pretty good track record.

Reserves & Pricing

AEM owns the right to mine gold, silver, copper & zinc for many years into the future from its mines. Estimates of these reserves are provided each year in the annual reports. For instance, the “Proven”5 gold reserve is 6.43M ounces of gold, which can be valued at about $15Bn which alone is about a third of the market cap of the company. Add to this “Probable”6 reserves of another 47Mn ounces of gold. We haven’t come into the Silver and Copper reserves and resources as yet. When valuing a company like AEM, one should not just look at price to earnings or price to FCF. Instead, what is useful is that the current stock price of about USD 70, CAD 95 is historically low compared to its earnings (18x vs 35x in the past 5 years).

It is possible that the valuation looks cheap because gold is at a present day high, and the market expects gold prices to come down. That doesn’t tally with all the other excitement around commodities these days. The way I see it is that AEM is a solid counter to be owning and while it has run up a bit in recent days, seems like a fundamentally good stock to own.

Summary

Agnico Eagle Mines is a well operated gold miner, with growing interests in other commodities, that presents a good play on precious metals and the energy transition. Growing organically as well as through acquisitions, AEM has a good track record of shareholder value generation. I own it for multiple reasons and look forward to adding to it.

As always, Happy Investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

This is largely because US ETFs are not investable from the UK. So, investors want to know the UK equivalent ETFs.

I focus on per-share to take away the dilutive effect of share counts increasing when acquisitions are executed.

AEM already owned the 50% in a joint ownership model with Yamana.

All-in sustaining costs per ounce of gold produced (also referred to as “all-in sustaining costs per ounce” or “AISC per ounce”) on a byproduct basis is calculated as the aggregate of total cash costs on a by-product basis, sustaining capital expenditures (including capitalized exploration), general and administrative expenses (including stock options), lease payments related to sustaining assets and reclamation expenses, and then dividing by the number of ounces of gold produced. These additional costs reflect the additional expenditures that are required to be made to maintain current production levels.

The highest confidence level, representing mineral deposits with well-established geological and economic parameters.

A lower level of confidence compared to proven reserves, often based on inferred or indicated resources and preliminary economic assessments.