A brief history of SBC

Compensation philosophy is screwed across the tech sector

Stock based compensation (SBC) is provided to employees of a company in order to encourage the employees to think like owners, over and top of salaries. There are broadly three forms of stock based compensation:

Employee Stock Purchase Plans (ESPP): In this, the company encourages its employees to buy shares of the company, and to incentivise them, offers a small discount (say 10-15%) over the current market price, so it can have “owner-employees”. 1

Stock Options: Employees are given a fixed allocation of shares to buy at a fixed price (normally the price equal to when the allocation is made) but is allowed to be purchased over time (say 4 years with a caveat that you can’t purchase anything in the first year). In this case, the employee benefits if the stock price goes up, but gains or loses nothing if the price remains the same or goes down. In fact, they are called “options” the same way as traded PUT & CALL options are, in the stock market, because they behave very similarly for the options holder, just that their ownership and price (set to 0) is conditioned upon employment of the individual. By giving a large time period to exercise these options, an employee could hold on to the options for a long period and just cash in when appropriate.

Restricted Stock Units (RSUs): In the RSU model, the company agrees to give you a set amount of shares for free, so long as you fulfil some restrictions - very often this is just continued employment with them for a set period of time, often starting at 1 year cliff and for a period of 3-5 years. So, essentially, consider this as a guaranteed retention bonus, just given in the form of shares.

(These three are roughly in descending order of risk taken by an employee and in increasing order of pain taken on by non-employee shareholders.2)

History of SBC

While many companies have offered stock to senior management for many many years, the idea of granting stock to your entire workforce (or a vast majority of them) is rather recent - some 30-40 years old. In fact, it boomed in line with the take off in Venture Capital (VC) funded start ups (90s). If your company depended on VC to get off the ground, then you want to strike the balance of bringing in the most important resource you needed - i.e. brainpower, yet conserve cash to improve the chances of an exit, as companies are often unprofitable in early years. Indeed, founders themselves weren’t allowed to draw much of a salary, as the VCs wanted you to have maximum skin in the game.

A balance was found in this endeavour by paying early employees less than market wage, but offering them ownership in the company that they could cash in if the company succeeded. If the company indeed succeeded and became profitable in time, then you could dial down giving stocks and instead use cash and pay market rates to your staff. While the legal structures of options were probably from before then, this growth phase of start-up economy, in the 90s, is what popularised stock options for the first time.

This system was largely based on the stock options system and stayed so blissfully till the dotcom-bust in 1999-2001 happened. Suddenly there were swathes of employees who had paid Alternate Minimum Tax (AMT) on their unrealised gains, but had not gains to cash in as their companies went bust, taking some employees down with them to bankruptcies.

Combined with the after-effects of AMT and a change to accounting principles through introduction of GAAP, many listed companies adapted by offering RSUs34 post 2006 - these structures are elegant as the tax event coincides with the point at which the stocks are entirely yours and free to sell and hence you can both enjoy the money and pay the taxes to the government.

However, even if listed companies were offering SBC to their employees, till late 2000’s it was minimal and might have amounted to no more than 2-3 months equivalent of salary per year, as they were offering market or above-market salaries to the staff they were hiring in any case.

In parallel a lot of companies in the tech space were constantly getting disrupted by newer upstarts, so much so that very often a large company would be forced to acquire a company that would have been started by their own alumni, paying doubly so for brain drain from their companies.

While many companies tried to solve for this, the first one, at least in my living memory, that cracked this was Google. They realised the importance of preventing upstarts and disruption, as they themselves were one (to Yahoo, for instance), and came up with a series of cultural innovations, including having an extremely favourable working environment, 20% of self-work time and getting acquisitions right.

However the killer change they brought about was the idea of paying their employees so much in SBC (through the RSU route) that most employees never felt the need to leave their jobs and go attempt a start up. Over time, this add-on to their salaries went from the 2-3 months, to being close to 12 months (or much more) worth of RSUs. Further, as Google’s stock kept rising, the value of these RSUs would compound over time, while you were getting new RSUs each year to keep you looking forward to more. In time there were 1000s (if not 10s of 1000s) of employees whose packages exceeded $250K per year due to the effect of RSUs, when market salaries were only about half of that.

I would argue that Google was the first one to get the defence on the attack from side-on competition and upstarts right. And because it worked, Facebook (now Meta) followed suite a few years later and other companies, even the older ones like Microsoft morphed their compensation packages (and acquisition strategies) to this new found path of wisdom.

Problems with SBC

The problems with SBC is rather clear. From being a tool to encourage people to come to work for a startup, to being a tax efficient way of compensation, we have now reached a point where SBC is nothing more than golden handcuffs for employees. It prevents movement of labour (to form new startups, or join other less paying companies) and in effect has reduce the amount of innovation and cornered talent among the few who can afford it.

Given the fact that these companies offer such a fantastic employee environment: excellent working conditions (vs working in factories), relaxed working hours (vs early stage startups), no need for stressful travel (vs consulting), great job security (till recent months), the idea that these companies had to further pay ridiculous amounts of SBC, on top of being at the 99%ile of the pay spectrum, to retain their employees sounds very much over-the-top. Other industries do a perfectly good job of chugging along without having to resort to such extreme measures.

Now, leaving aside the effects of labour market and economy, let’s switch to non-employee shareholders. All of the above compensation policies result in the company diluting existing shareholders by issuing new shares. These in effect reduce the percentage of stock holding that you and I as shareholders hold.

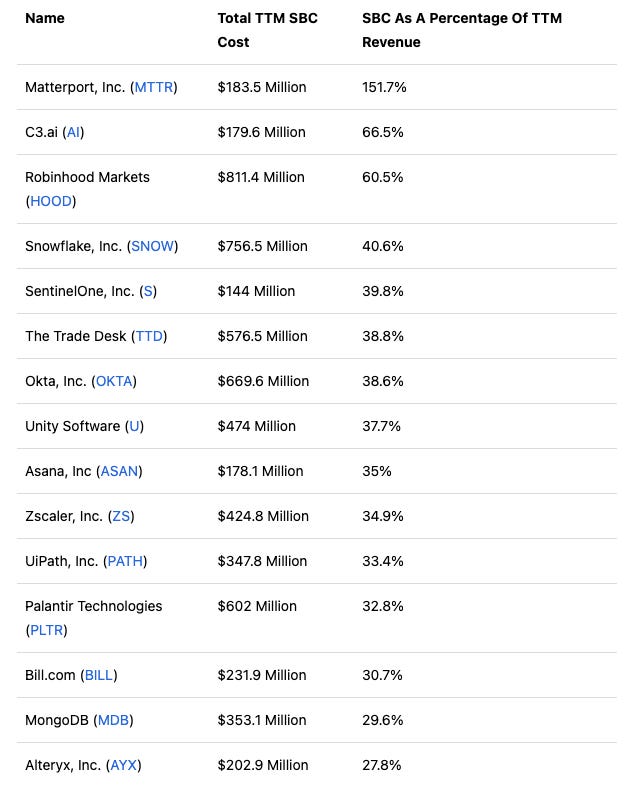

How bad is it?

Here is a list of 15 companies whose SBC as a percentage of revenue is on the highest side.

Meta gave out $12B in stock based compensations in 2022, which is more than half of the net income of the company for the same time period. Think about it - half of the net income is eaten up by internal employees leaving a materially lower share of profits for the investors themselves. Alphabet (Google’s parent) spent $19B in 2022, some 32% of their net income for the same time period. These are outstandingly large numbers for these companies!

If you want see another example from my own portfolio that has done an exceptionally poor job of SBC, it is ASX:IRE (Iress Ltd.), whose share count has grown from 125M in 2010 to 188M in 2022 - a whole 50% of the company has been diluted away to pay for employees and executives. This company is so bad on this that I have stopped buying this stock altogether.

Complicit Investors

Sadly the investment community has largely turned a blind eye to this aspect for many years now. While the companies were growing their revenues and the stock prices were on a tear, there was too much fun to be had among the shareholders, employees and managements that nobody thought a second about these things.

However, now that the party is being challenged by moderating growth and tightening financials, the focus is on SBC and so should it be (or should have been all along).

Solutions?

Ideally, companies with healthy P&Ls should reduce their use of SBC by a material amount. It is still crucial to have employees motivated and retained for long periods of time for institutional knowledge, and it is important to offer healthy compensation and good working conditions, but is doesn’t need to be outlandishly generous. A moderate amount of stock in magnitude and in form better aligned to shareholders is much better for all parties involved - for instance stock options are always better than RSUs as they are only exercised if the stock price has gone which is as beneficial for the non-employee shareholders.

In fact I would argue that moderate amount of SBC, making the entire P&L sustainable is better even for employees as it gives them a long-term view into a stable income, instead of the unsustainable levels of SBCs that many of these companies are doling out, but in parallel subjecting workforces to layoffs, which are always painful.

However, it is hard to see how this is going to be fixed. While some of the companies with most egregious SBCs have been forced into (painful) layoffs and have been punished by investors, in general, compensation programs across tech companies are unlikely to change. This is because the management, up and down the levels, reward themselves through these compensation policies too, so there is going to be little internal incentive for them to update their compensation packages. In fact even if boards wanted it, there would be wholesale revolts at most companies bringing the business to their knees. Activists could force the hand a bit, but tech companies like Meta and Alphabet’s voting rights are controlled by founders through special class of shares, that any change is unlikely to happen through that route.

What should we do?

As an investor, if it is a tech company you want to invest in it, keep an extremely close eye on SBC line items. Think carefully about whether you think this is justified or not. When reviewing growth numbers, don’t just look at revenue and profit numbers, look at the long term per share numbers too. The good companies would be keeping the per share numbers as good as the absolute numbers, if not better (through buy backs) and the worse ones would have per share growth numbers materially lower than the absolute numbers. Remember your upside is strictly based on the per share numbers.

Depending on how this is structured, it can be hugely beneficial for employees, as very often they are structured over six months and the company offers it on a discount to the lower of the entry and exit prices, offering employees a free six month look-in period.

I have read literature about how stock options are perhaps the most dangerous form of SBC as it encourages employees and managements to take a short-term view to push up the stock so they can cash in, while RSUs build a more long term mentality. There is merit to this argument at some level.

Unlisted companies continued to offer stock options as there is no liquidity of shares yet, but AMT is still applicable if I am not wrong. Companies often permit employee participation in some funding rounds precisely to let employees gain enough liquidity to pay off their taxes.

Unlisted companies almost never resort to RSUs, and that’s because the tax event happens before the employee gets a chance to cash out. One of my previous employers in Singapore granted a bunch of RSUs to me and I accepted without understanding this nuance as we thought Singapore didn’t tax such gains. The founder and I came to know only when tax advisors were wheeled in as part of an acquisition process. Thankfully, the year when my tax were to come due coincided with the acquisition.

And by the way WFT Matterport?

Great article - this is one of the myriad reasons I exited S. (exit will probably be as ill timed as my purchase, as everyone seems to be throwing themselves at AI now)