S&P 500 in Coffee Can mode

Review of a paper on buy & never sell on S&P 500

The past 2 weeks have been a bit crazy for me, with travel and some post-travel workload keeping me busy. Hence I am running light on content. Instead of breaking the habit of writing every weekend, I will pen a quick post to review a piece of literature I read a while back, relevant to the topic of this substack.

S&P 500 is considered among the gold standards for comparison of portfolio returns, as it has itself returned some 11.88% per annum1. Since 1957, when the S&P 500 was first introduced, to now, the index has been chopping and changing along the way. For instance, the 7 companies that drive the S&P 500 (Microsoft, Apple, Google, Facebook, Amazon, Netflix and Nvidia) didn’t exist back then. Every now and then, the S&P 500 committee decides what should be in and what should be out. They are guided by basic principles and selection criteria, and largely follow the theme of “500 largest capitalised liquid companies listed in America”.

Given the S&P constituents change all the time, what we see as S&P 500 performance is the performance of this ever changing index - this includes new companies coming into the index, as well as companies going out of the index. Think of the S&P 500 as a fund, except that instead of a single fund manager managing it, it is guided by the S&P 500 selection committee (and their rules and criteria). If you think like that, then every company coming into the index can be considered as being “bought” and every company making it out of the index can be considered as being “sold”.

So, if the index is participating in selling of stocks, then it is no more acting in the Coffee Can Investment philosophy of buy and never sell. However, what if you had a choice of buying and never selling S&P 500? How would that option work out?

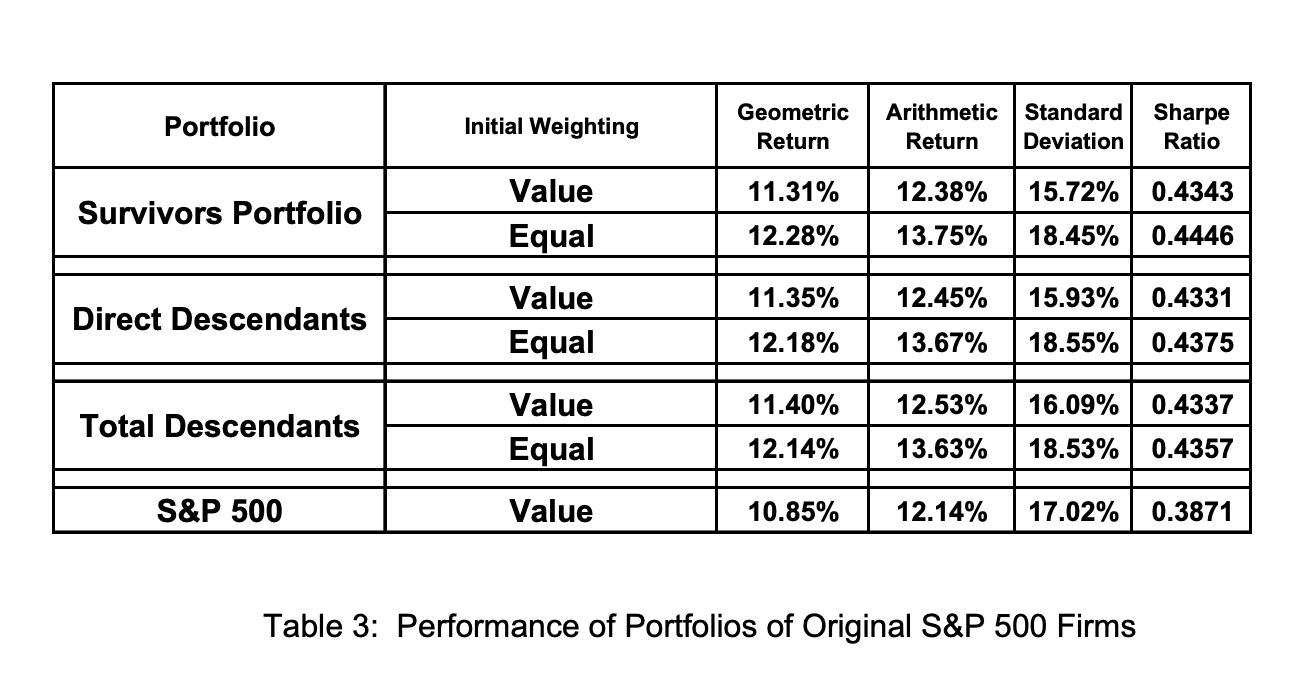

This is where some research content comes in handy. In 2004, two well respected researchers in the field of finance, Jeremy Siegel2 and Jeremy Schwartz3, authored a paper titled “The Long-term Returns on the Original S&P 500 Firms”. They analyse the original constituents from 1957 and run their performance on a “buy and never sell” methodology and compare that to the ever changing S&P 500 index.

What they found is that the survivors from 1957 (or versions of theirs descendants - spinoffs, splits etc, are included) have performed exceptionally well, in fact beating the S&P 500, over the 47 years in question.

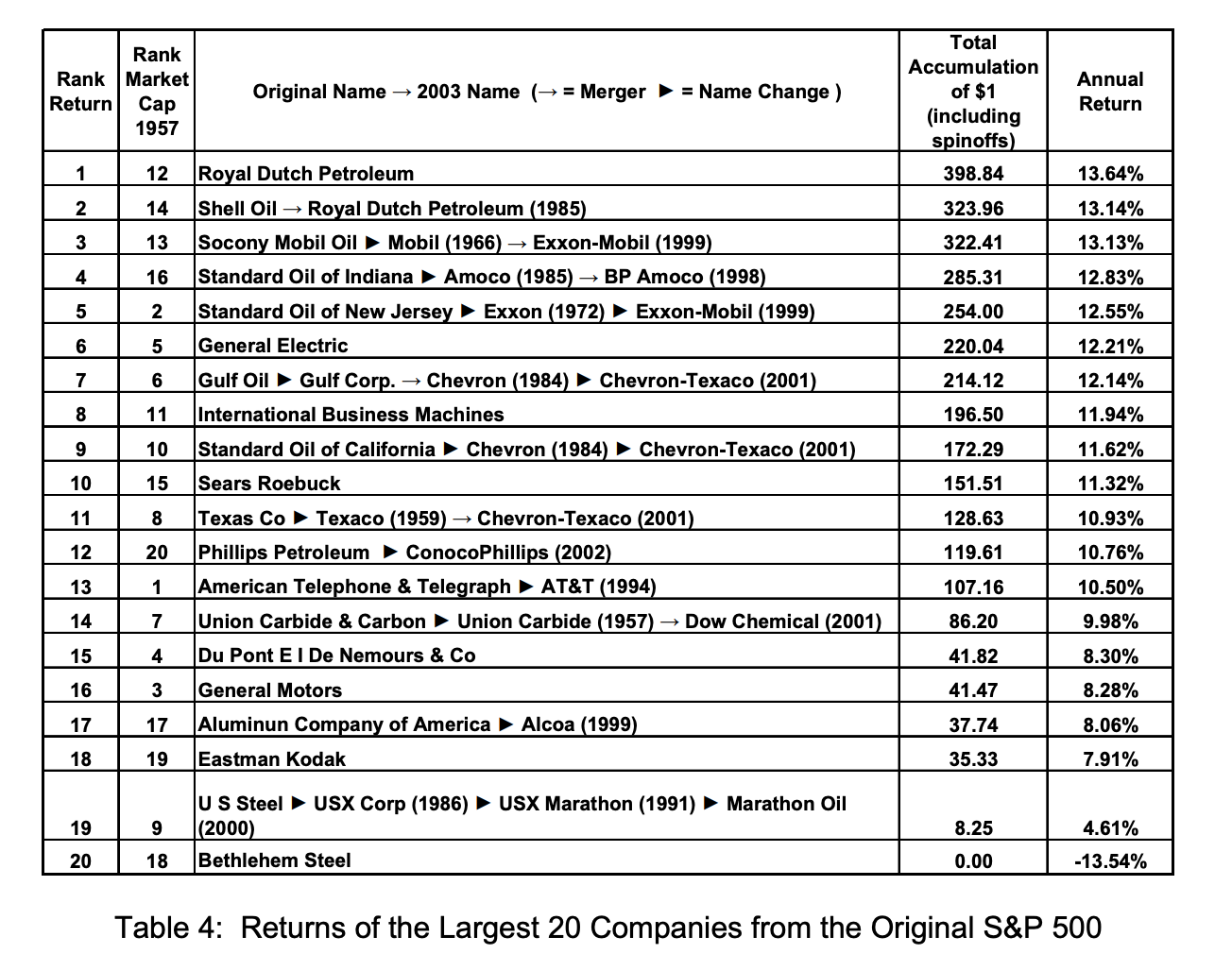

While looking at these results, you must consider the reality of a world that extensively changed in these intervening years, as post-war expansion in America, introduction of communication technologies, the massive explosion of media (Radio, TV etc), expansion of the use of the automobile, the introduction of computers, and eventually the Internet, all were changing the lives we were living, and the economy around us4. In fact the top-20 companies from then are barely recognised as important economic players today:

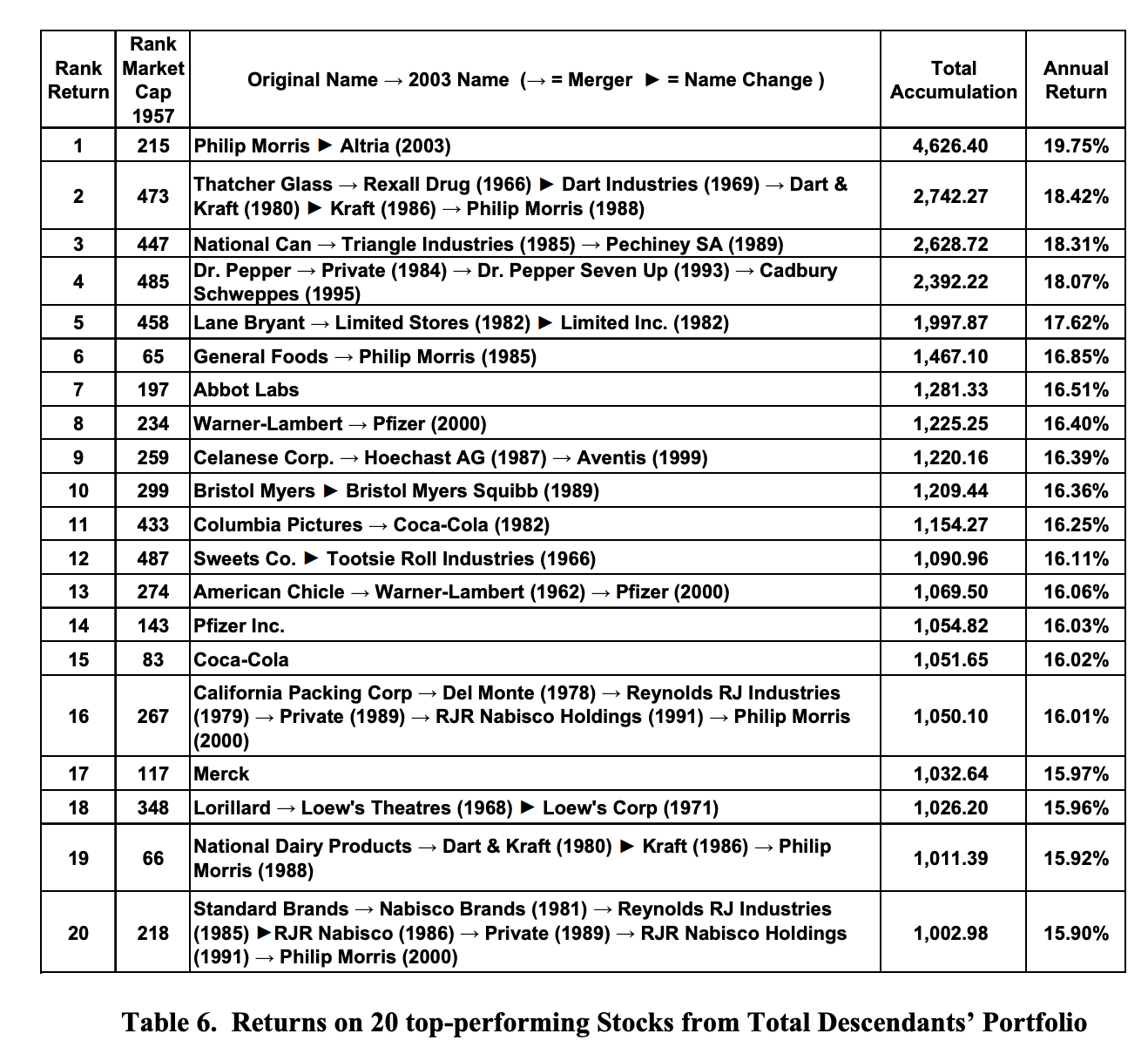

And yet, despite their waning relevance over the decades, the returns of these companies, along with the 480 others in the index some of whom did exceptionally well, made up enough performance that the lack of changed in composition hardly ever mattered. Look here at the top-20 performing stocks from that collection - see if you can recognise many here.

This paper was authored some 20 years ago and one might need to rerun their research methodology to keep up pace with everything that has happened in the S&P 500 world since then and it is likely that their findings are now invalidated, or reinforced, but nevertheless, 47 years is a long period and their findings are material enough for us to consider this seriously.

This is another evidence to why buy and not sell can be a superior style of investing, something that this blog strongly augurs for. The paper is quite an easy read and if you have time, have a go at it. In the meanwhile, happy Investing!

Upto 2021

From ChatGPT - “As of my last update in September 2021, Jeremy Siegel is an American economist and finance professor. He was born on January 10, 1945. Siegel is best known for his work in the field of investments and finance, particularly his research on stock market returns and long-term investing strategies.

Jeremy Siegel is a professor at the Wharton School of the University of Pennsylvania, where he has been teaching since 1976. He holds the position of the Russell E. Palmer Professor of Finance and has received numerous awards for his teaching excellence.

One of Siegel's most famous works is the book "Stocks for the Long Run," which was first published in 1994. In this book, he argued that, historically, stocks have provided higher returns than other asset classes, such as bonds or cash, over the long term. The book became widely influential and has been cited by many investors and financial professionals.”

From ChatGPT - “As of my last update in September 2021, Jeremy Schwartz is an American finance professional and author. He is associated with the investment management firm WisdomTree Investments, where he has held various leadership roles.

Jeremy Schwartz is particularly known for his work in the exchange-traded fund (ETF) industry.”

I use the term “us” rather loosely. I wasn’t born till well past half way through the period in question, and didn’t step on the American soil till the research completed. I am guessing most readers might have similar experiences. 😆

Great article. I think the findings would almost certainly be invalidated now due to rise of Big Tech and probably by a very big margin.