Ryanair: Europe's Most Despised Compounder

Ryanair isn't trying to win friends. It's winning market share - and that's exactly the point.

I have stayed away from aviation investments1. Warren Buffett’s long-held scepticism of airlines - before his own eventual foray - resonated with me, and for good reason. Airlines are capital-hungry, operationally gruelling businesses where grandiose ambitions frequently collide with brutal economics. Make a few false moves, and you are staring at a mountain of debt with no easy way out.

So when I do take the plunge, the bar is high. Ryanair clears it.

The Business: Ruthless Simplicity

Ryanair (RYA.IR/NASDAQ:RYAAY) is Europe’s dominant budget carrier, headquartered in Dublin, operating point-to-point routes across the continent. Its core proposition is disarmingly simple: the cheapest ticket on the route, almost every time.

The cost discipline behind that proposition is anything but simple. Ryanair flies a single aircraft type - the Boeing 737 family - keeping maintenance, training, and parts interchangeable across the fleet. Planes carry their own pull-out staircases to avoid airport fees. Turnaround times run 20–30 minutes, maximising hours in the air. All tickets are non-refundable, eliminating an entire layer of operational complexity. Check-in is digital-only. Heavy luggage is actively discouraged to manage fuel burn. Every decision, without exception, is filtered through the question: does this reduce cost?

The only thing that sits above cost discipline is safety. CEO Michael O’Leary has been emphatic on this - and the airline’s operational record backs it up.

O’Leary himself is worth a word. He’s cultivated a persona of outrageous provocateur - floating ideas like pay-per-use toilets and standing seats - and the airline has earned a reputation as one of Europe’s most derided carriers. O’Leary has essentially leaned into this: “The day we win awards for being popular, I will quit.” But strip away the theatre, and what you find is one of the sharpest operators in global aviation: a man with a forensic understanding of airline economics and a decades-long track record of turning that understanding into profit.

The base fare gets you on the plane. Everything else - seat selection, extra legroom, food, insurance, car hire, hotel bookings - is an upsell. Critically, most of that ancillary revenue is pure commission income, with no operational burden on Ryanair. It is a well-worn low-cost playbook, but nobody executes it more seriously.

The Growth Story

Despite the reputation, customers keep coming - because cheap fares and good connectivity are hard to argue with. (I’ll admit I’ve found myself on Ryanair more times than I’d planned, and never anywhere near the advertised headline fare.)

The numbers tell the story clearly:

Ryanair is now the world’s largest international airline by passenger volume - a function of the fact that most intra-European routes cross a border.

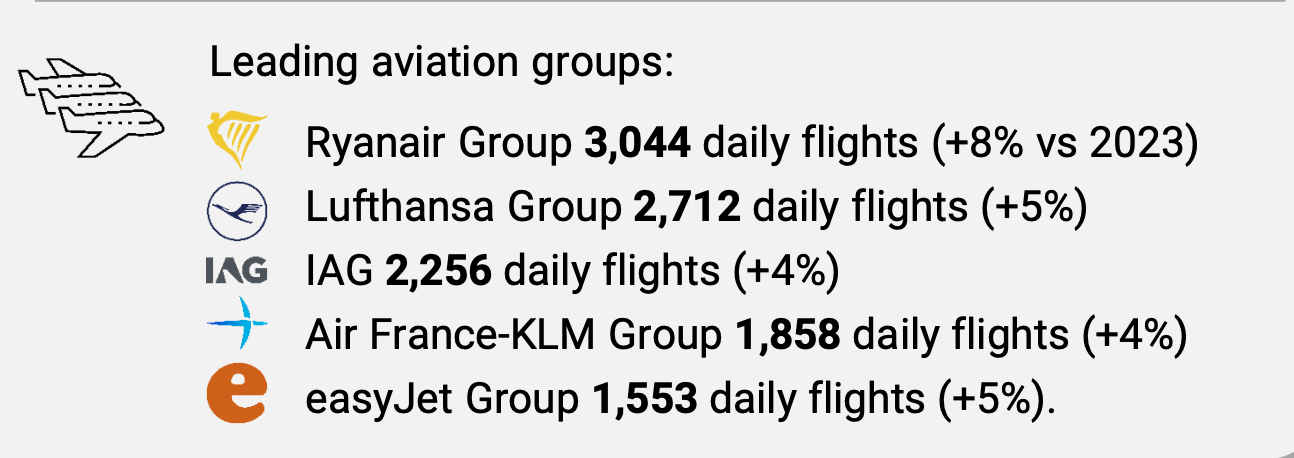

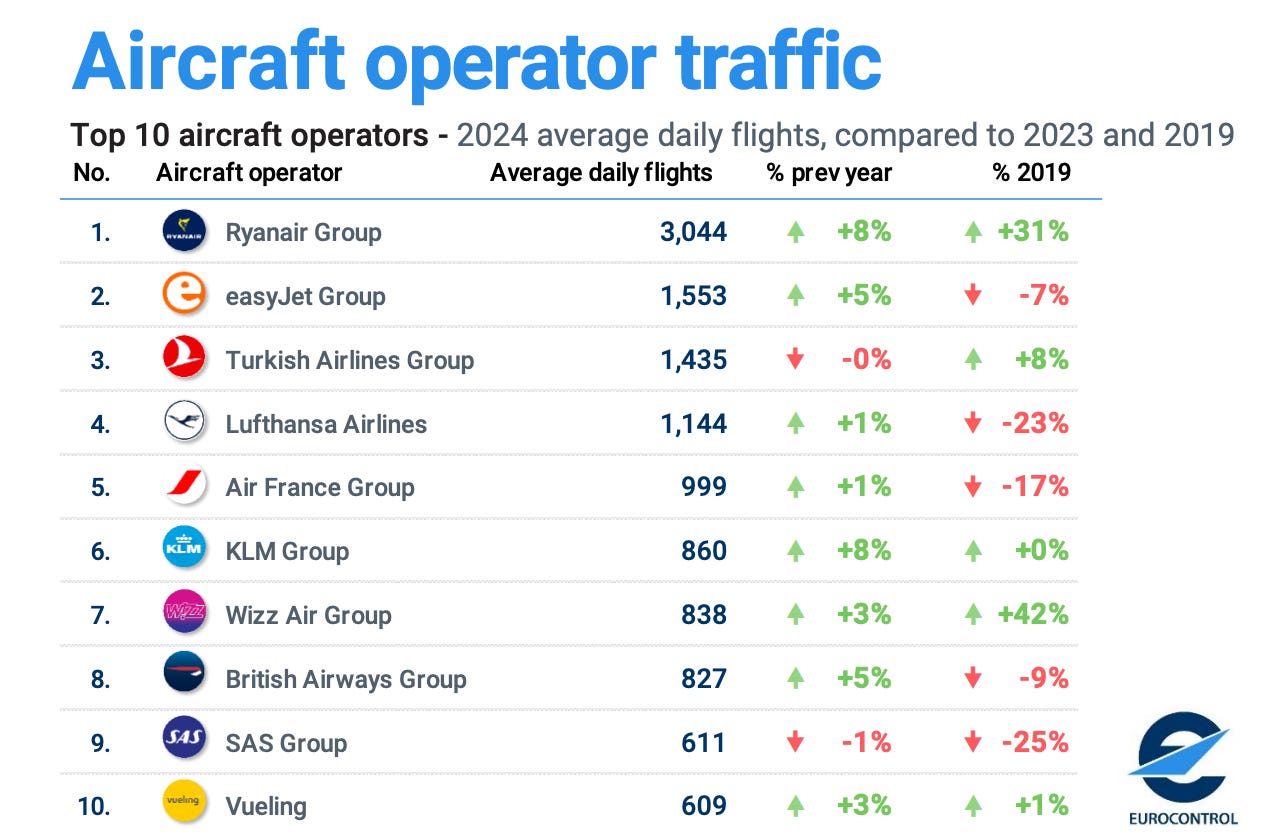

In 2024, it operated 3,044 daily flights2, leading all European aviation groups, and was the fastest-growing among the majors.

Over the five years to 2024, it grew capacity by 31% - second fastest in its peer group, and fastest among the top five.

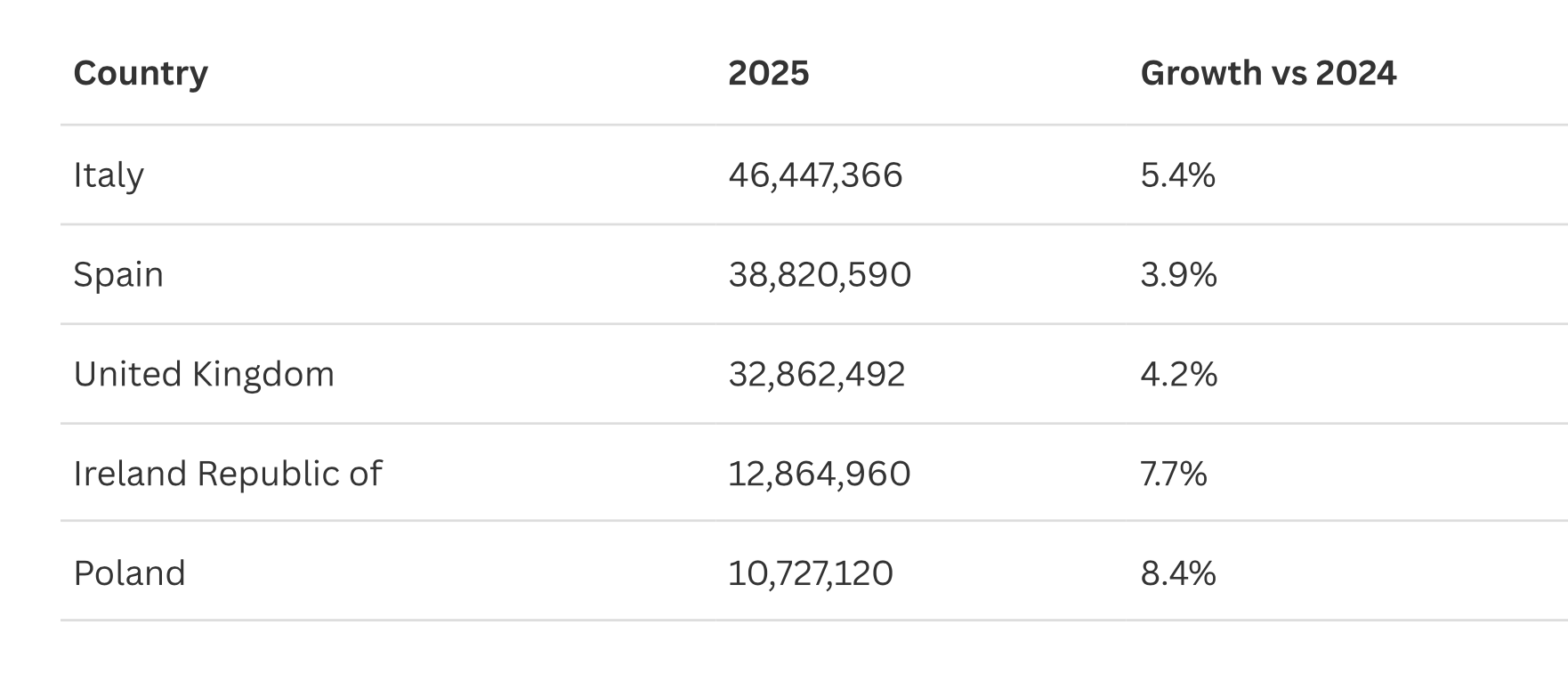

In its top five markets in 2025, passenger volumes grew 4–8%3. In Italy alone, Ryanair now accounts for 48% of all domestic passengers - a level of market entrenchment that is difficult to dislodge.

In FY2025–26, it added another 4% in passengers and 11% in revenue.

This is a business that keeps growing, almost regardless of how people feel about flying it.

The Bear Case: Three Risks Worth Taking Seriously

Being balanced requires acknowledging the headwinds. There are three that deserve genuine attention.

1. Oil prices and geopolitical risk. Fuel is Ryanair’s single largest cost, and the current Middle East situation has pushed prices higher. This is real. That said, Ryanair is approximately 80% hedged on fuel costs through March 2027, which provides meaningful near-term insulation. More importantly, fuel shocks hurt all airlines - and Ryanair’s structural cost advantage means it absorbs them better than most. A prolonged crisis could actually accelerate competitor distress and hand Ryanair further market share, as it has done in past downturns.

2. Boeing delivery delays. Ryanair has 154 aircraft on order from Boeing, against a current fleet of 359. Boeing’s well-documented production and quality control difficulties are a legitimate concern - delayed deliveries constrain growth capacity and create planning headaches. This is a risk I don’t dismiss. However, Ryanair has navigated Boeing delays before, and O’Leary has been publicly combative with Boeing in pushing for both timely delivery and compensation. It is an overhang, not an existential threat.

3. Competition from EasyJet and others. EasyJet is the closest comparable and follows a similar playbook. The European low-cost market is competitive. The honest counterpoint here is that Ryanair has consistently out-executed its peers on cost - its CASK (cost per available seat kilometre) remains the benchmark in European aviation, with only WizzAir in Europe coming close. That gap doesn’t close overnight, and Ryanair’s scale advantages compound over time.

None of these risks are reasons to avoid the position. They are reasons to size it with appropriate humility.

The Bull Case

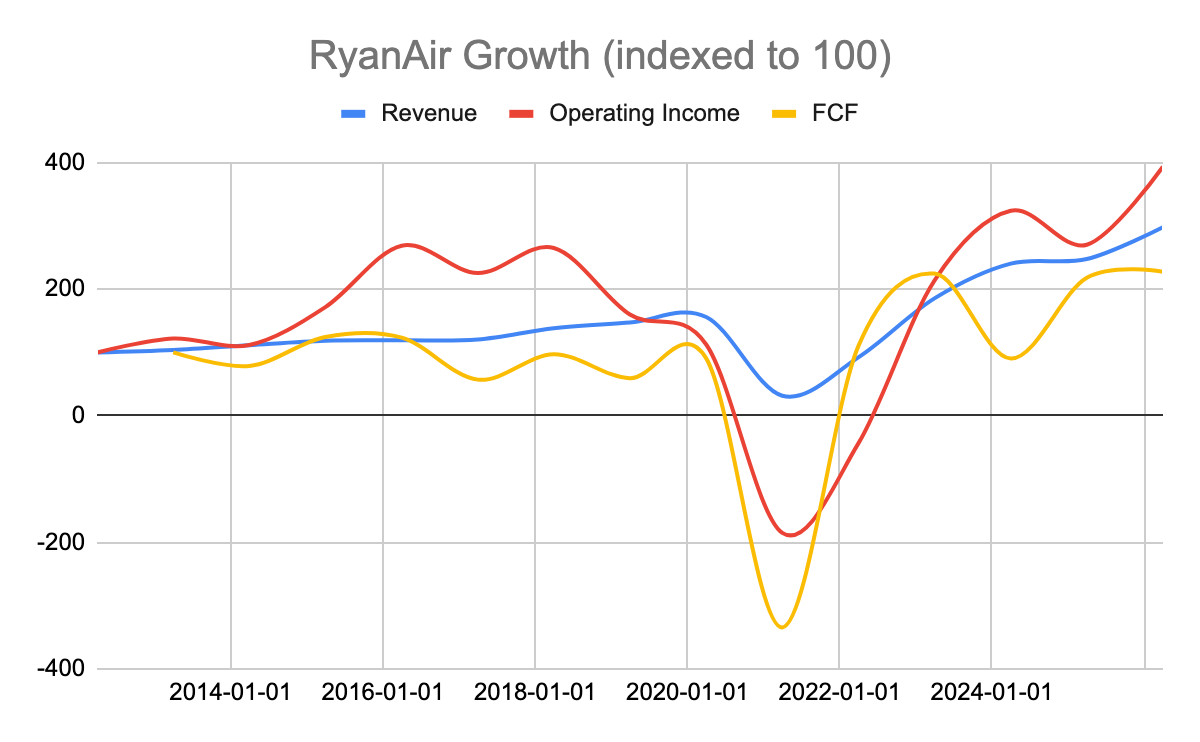

Here is why I am buying now. Its clear that the RyanAir growth story is in progress and offers a reasonable runway ahead, and a well run company with growth prospects are not easy to find at reasonable prices these days.

In that context, its notable that Ryanair trades at roughly 14x trailing earnings and 17x trailing free cash flow - a valuation I haven’t seen on this business in some time. A combination of macro headwinds and broader market caution has brought the stock down approximately 15% year-to-date, creating an entry point that a structurally sound, growing business rarely offers.

Critically, the balance sheet has just been cleaned up. Ryanair recently paid off its last €1.2 billion of debt, leaving it debt-free. For an airline - a capital-intensive business where leverage is often the thing that kills you in a downturn - this is a meaningful distinction.

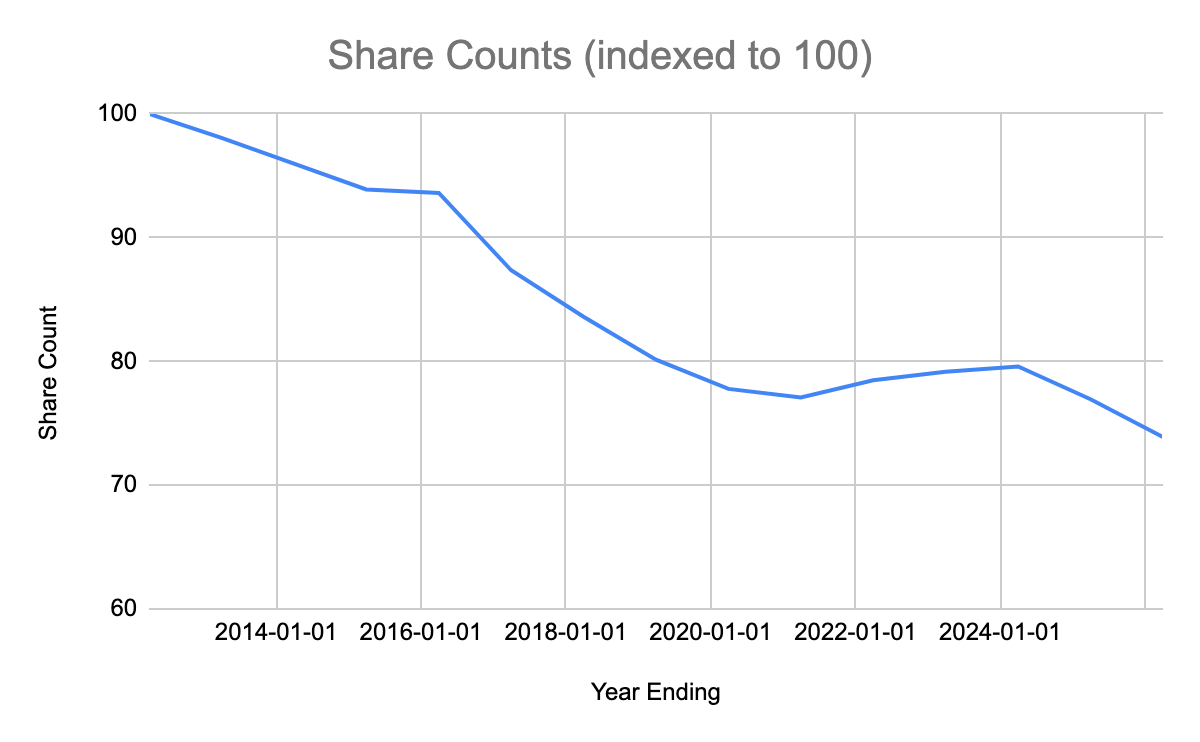

While the company has been repurchasing shares aggressively over the past decade, having retired 27% of stock, it has been increasing return to shareholders through a combination of buybacks and dividends, with the last 2 years showing a marked acceleration, returning $5.80 per share4.

The setup is straightforward: a dominant low-cost operator, with the strongest unit economics in its category, growing passengers and revenue, debt-free, and trading at a discount due to transient macro concerns. The 154 aircraft on order provide a clear runway for continued capacity growth as deliveries eventually normalise.

This isn’t the cheapest entry I’ve made recently - HOG, NVO, and CROX all came in at lower relative valuations with more questions hanging over them. Ryanair comes with fewer existential questions and a more predictable compounding path. At this price, with this balance sheet, and with this management team, the risk/reward is compelling.

Unlike my recent ventures, where I have deployed options a lot, this one is back to basics - I am acquiring the US listed ADR - RYAAY, a small number of shares at a time, and it will likely be many months before I get to my desired position size (and even that depends on exiting some options positions along the way.)

Position initiated. Happy Investing.

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.

I shorted IAG during Covid, though I don’t recall that being particularly profitable - I think it was all poor timing.

https://www.eurocontrol.int/sites/default/files/2025-01/eurocontrol-european-aviation-overview-20250123-2024-review.pdf

https://www.oag.com/ryanair-performance-stats

Here, share means a unit of the US listed ADR with ticker RYAAY.

they have good manager