Portfolio vs AI

How resilient is a portfolio vs oncoming AI changes

The past year or two have been the coming-out party of Generative AI and Large Language Models (LLMs). Across text, video, audio and images, AI tools are set to significantly automate, enhance and in some cases exceed the human power of creativity. This is set to make significant changes to how the world functions, specifically, in how human effort is put to economic use, in the coming years and decades.

To remind ourselves, the broad category of Artificial Intelligence or Machine Learning is not new. For context, yours truly wrote his master thesis on this topic1 some 20 years ago. Along the way, not only did many many uses of AI and ML show up, but were put to practical use across the spectrum of the industry2 - think of voice assistants, recommendation engines, spam filtering, photo tagging and detection tools, completion and grammar check on various text products etc, all of which were readily available to us from a variety of tech providers well before the onset of the latest craze.

For some years now, industry across sectors have been adopting AI in what I call “hard world problems” - i.e. in Robotics across logistics, manufacturing, self-driving cars etc. This has been going on for many years too, well before generative AI and LLM came along.

So, what has changed now? It is collection of breakthroughs by researchers across companies and academia, in the category of problems called Generative AI. In essence, instead of algorithms being able to do things like categorise things, or look up things, or move and control something precisely, all of which have well defined outputs, AI algorithms can now generate whole creative artefacts based on learning from large sets of training data. Their outputs are no longer bound by what the programmers of the system thought of, and instead can span a wide variety of skills, like writing poems, generate videos, produce speeches and so on. These creative artefacts are a significant step up in machines’ ability to generate outputs that are well above what we have been used to with computing machines so far.

Business and Industry have adjusted, adapted and evolved with all of the AI that has come before this latest round of innovations. The question then is, what will this new round bring to us in the form of changes and disruption? The rest of this post will talk about the impact Generative AI (including LLMs) are likely to have on the coffee can portfolio companies. Beware that this is a very subjective assessment and one must make their own judgments, as well as the fact that I am not an expert on the topic.

AI and the Portfolio

There are two factors we must consider - (a) the risk to the business from the promulgation of AI and (b) the opportunity that such a change might bring to the business. In some cases a company that is threatened will also likely possess the highest opportunity to innovate and benefit from the changes. So, it is not necessary that the two are coordinated in all cases.

Let’s start with risk levels. Companies with the highest risk are likely those whose businesses are directly under threat from the changes, primarily because they expose a large surface area for the AI changes to attack.

At medium risk are those companies who have some lines of their revenue at risk, but have some sort of mitigation either in place or likely to have one in place soon enough. Companies with cloud revenues are in this category, as changes in AI will necessarily change the way cloud services are put to use. If these companies can’t ride the coattails of that change, they will be left behind, at least on those revenue streams.

At lower end of the risk spectrum, companies in many sectors that have little to do with AI and whose revenue streams aren’t going to be impacted by the changes any time soon. Remember that all innovation before Generative AI has already been baked into these businesses and their valuations etc.

High Risk

I am putting Google, Iress, and Disney in the high risk category.

The entertainment industry will see innovation on how best to use AI, and Disney’s biggest assets - their ability to generate high quality content at high gross margins will be challenged as newer, innovative competitors invest in the area, putting at risk Disney’s marketshare. Parks business may not be easy to attack, but the characters and the streaming business are all up for higher levels of competition.

Google’s own generative AI still seems to be a few steps behind and it’s cloud business may also come under threat. More importantly, if people spending time on search are going to spend it on ChatGPT (or other tools), then their advertising is likely to be affected too.

Medium Risk

Tech in general will be materially impacted, or risk some part of their business from Generative AI related changes. In this, I list Tencent Holdings, Alibaba, NetEase, Microsoft and OpenText as Medium risk.

Tencent, Microsoft and Alibaba all have big cloud businesses, that could be disrupted if they don’t keep up with new GPU based architecture and infrastructure needed for AI products. Think of Intel - they did nothing wrong in their core product offering, it is just that the world switched to needing something else and they didn’t keep up. I see the above portfolio companies in the same light.

NetEase and Tencent are both in creative businesses and both can be upended by new products coming out using AI much more efficiently. Tencent also has a massive portfolio of investments, many of which will face similar challenges.

Despite the fact that Berkshire is composed of a lot of Apple, I am categorising that company as Low risk, largely because I think Apple itself doesn’t have a big surface area that can be attacked by Generative AI, and Berkshire contains a lot of other sources of revenues that seem devoid of related risks. Somewhat similar is the case with OpenText, whose cloud business is rather bespoke and niche, and the business is well supported by customer support and professional services.

Low Risk

It doesn’t take a big leap to estimate that rest of the sectors in the portfolio such as Trading, Construction, Consumer, Utilities, Healthcare, Commodities, Aviation, Industrials, Financial Services are unlikely to be disrupted due to generative AI. Some of these businesses might become slightly more productive in the wake of the AI toolkits that will no doubt come along, but at its core, these companies are in brick and mortar industries who success depends on large amount of logistics, supply chain, brand building, distribution channels and workforce management, with almost none of these being in the “creative” industries category, except Disney, that has already been categorised as High Risk.

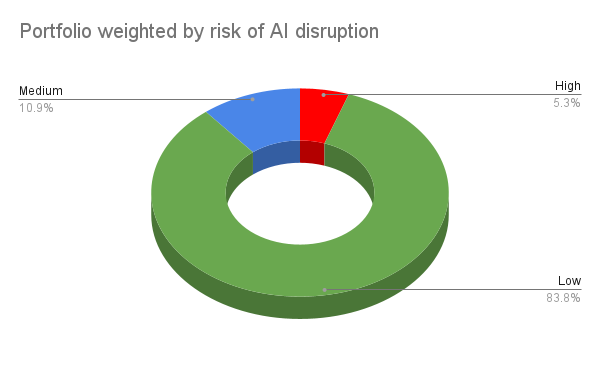

Portfolio split by AI risk

This is how the allocation of my portfolio looks like today.

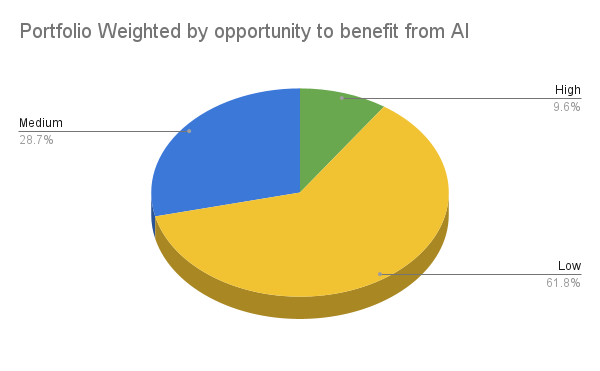

Portfolio split by opportunity with AI

Now, let’s consider opportunity. I think all the tech companies stand a high chance of being able to rethink and out-innovate their peers in this period of AI changes. Some of them might be lagging today, but they have the ingredients to pull it off, either by producing end products, as Microsoft is heading towards, or buy selling the infrastructure to others who desire to do so, like Amazon through their AWS offering.

The vast majority of brick and mortar companies listed in the low risk section, are correspondingly going to see lower opportunity to participate in this upside. And some companies will fall in the middle, with a possible outside opportunity of enhancing their revenue streams but perhaps nothing substantial.

Put it all together and you get a split that looks like

Summary

The portfolio seems defensible enough that the compounding of these businesses, and the investment opportunity for us, shouldn’t be too much as peril, but the opportunity to participate in the upside is quite limited.

While on one side, I am tempted to include companies that are possible winners from this technology change, like NVidia, but it is a crowded trade and I am yet to come across reasonably priced opportunities. While it is not optimal, I guess owning a cross section of the big tech through Amazon, Google, Microsoft is what I will live with till I find compelling alternatives.

What do you think? Share some comment love.

nb: All risk and opportunity assessments are entirely subjective. I am putting all of this into a sheet for you to take a look at and play with, if desired.

ps: The substack hasn’t seen a lot of subscriber growth recently. If you like the content you read here, can I request you to kindly share it with your networks so more people can join the coffee can community please?

This resulted in a paper titled “Pre Linguistic Verb Acquisition from Repeated Language Exposure for Visual Events.” and presented at ICON’2004, by my co-authors. In effect, we were figuring out if computers can learn the difference between “run” and “walk” without being programmed to do so. What we learnt is that Recurrent Neural Networks can do the job effectively. Research was also coming out that living organisms had versions of recurrent neural networks in their heads and they used it for timing events.

Sadly, I don’t think this moved the research community much forward and immediately after granting me a master’s degree, it was quickly forgotten.

In the AdTech industry, a rather niche industry in the broader scheme of things and where yours truly works, Machine Learning has been put to use for many years across campaign goal optimisations, control problems and even fraud and brand safety.