Performance Update (Q3' 2025)

Not every quarter is a headline — but every one adds a chapter

Q3 is already in the rearview mirror — time to see where the Coffee Can Portfolio (CCP) stands. On a lifetime CAGR basis, measured in GBP:

CCP: 13.11%

Benchmark: 13.90%

Alpha: -0.79%

Average Inflation (since inception): 4.03%

Real Returns: 9.08%

Candidly, it’s a mixed bag. A 9%+ real return is nothing to sneeze at — that’s serious compounding — but the portfolio still trails its benchmark. For all the hours spent poring over reports, running screens, building conviction, and pulling the trigger on trades, one could argue a lazy global tracker would’ve done the job. Perhaps even better — though I’d wager my liver’s better off this way than if I’d spent that extra time at the local watering hole.

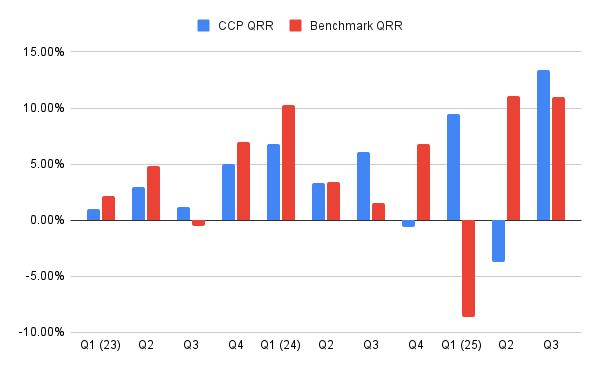

Quarterly Review

Looking at the quarter-by-quarter chart, the CCP and benchmark move in opposite directions 4 out of 11 times — a hint that returns may be uncorrelated, though I’m not sure what textbook definition of uncorrelated is, given it also has the same direction 7 out of the 11 times. More interestingly however, every time the benchmark surges (say +5% in a quarter), CCP tends to lag, and when the benchmark cools off, CCP catches up — except this past quarter, where CCP outperformed even in a roaring bull market. That’s a first; and hopefully one of many.

Six months back, I wrote:

“It’s easy to misinterpret this recent catch-up as a sign of structural advantage when it may simply be mean reversion at play. While generating solid real returns is a sufficient reason to continue with this approach, true validation will come when the portfolio outperforms even during strong benchmark rallies.”

Since then, the track record has been a coin flip — which isn’t much of an edge, so being able to achieve this more often than not, even if they don’t come consistently, would be a good achievement from here on.

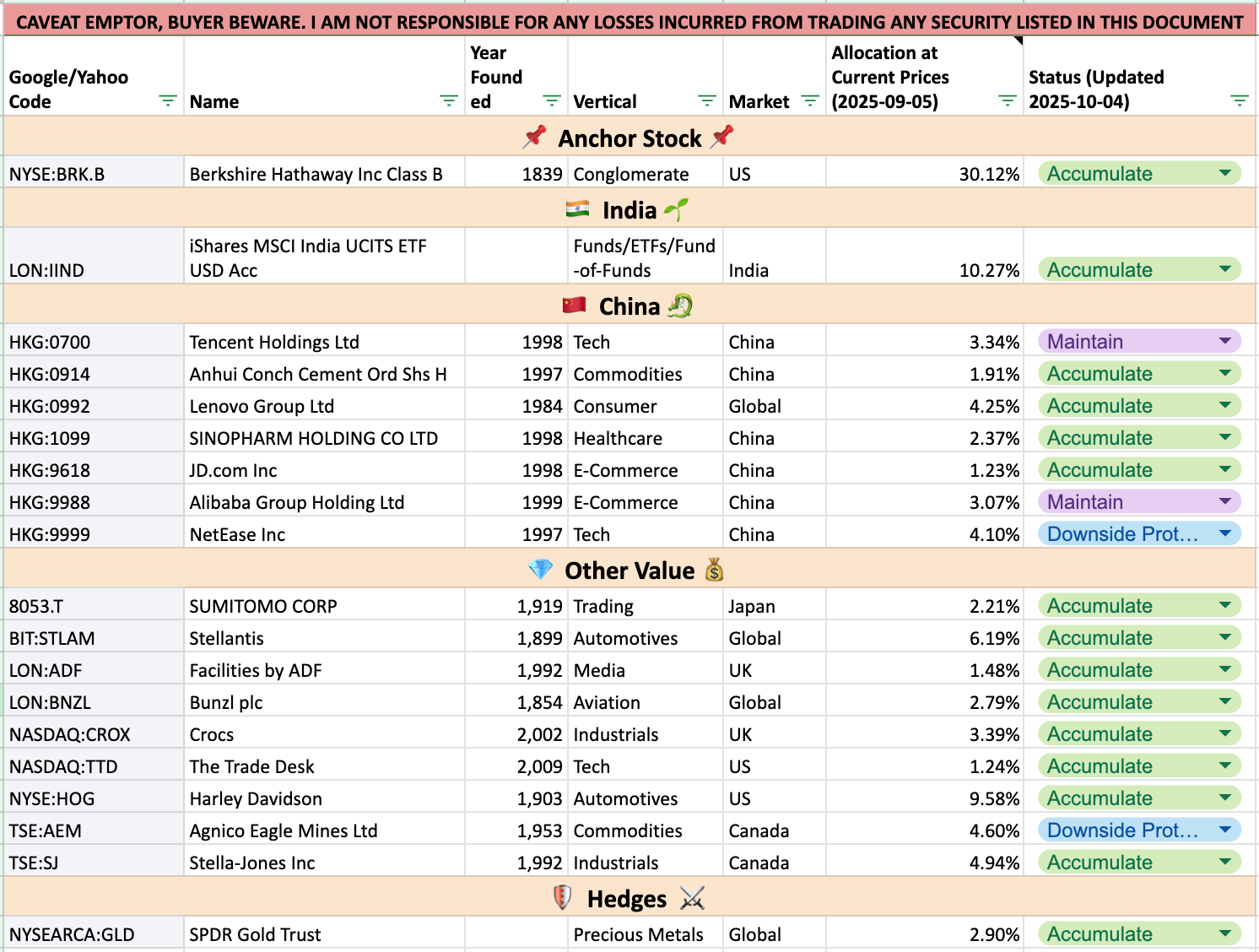

Basket Review

Before we go into the baskets, here is how the portfolio is structured:

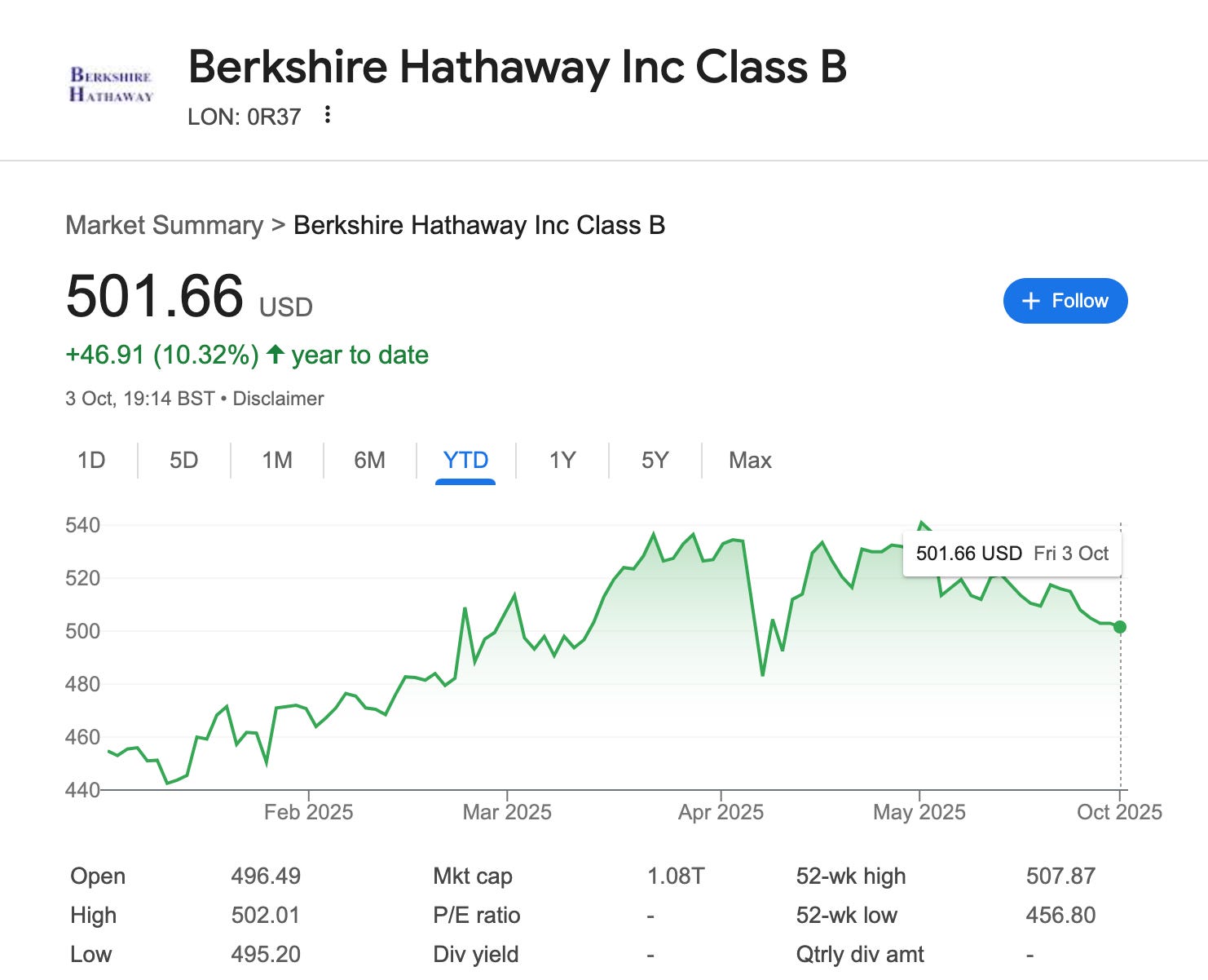

Berkshire

Berkshire continues to hum along. The stock had a roaring Q1 and has been hovering just below its all-time highs since.

Nothing exciting to report — which is exactly how I like it. I added a touch more around 465 and am happy to let this compounding machine do its thing.

China

China was a surprise out-performer in Q3, continuing its quiet recovery from earlier quarters. Alibaba led the charge, with Tencent and NetEase following suit. This basket has long felt like punctuated equilibrium — long periods of dormancy, then sudden bursts of life.

Even after this run-up, valuations remain modest- though NetEase looks close to being fully valued - I may add a stop-loss or protective puts there. Otherwise, this basket stays untouched. Sometimes the best move is no move.

India

India has largely been hovering lower this past quarter — a sign that the market is catching its breath after a strong multi-year run.

To me, these are exactly the moments to add, not retreat. I’ve been steadily increasing exposure through India ETFs, treating this consolidation as an opportunity to strengthen the long-term position.

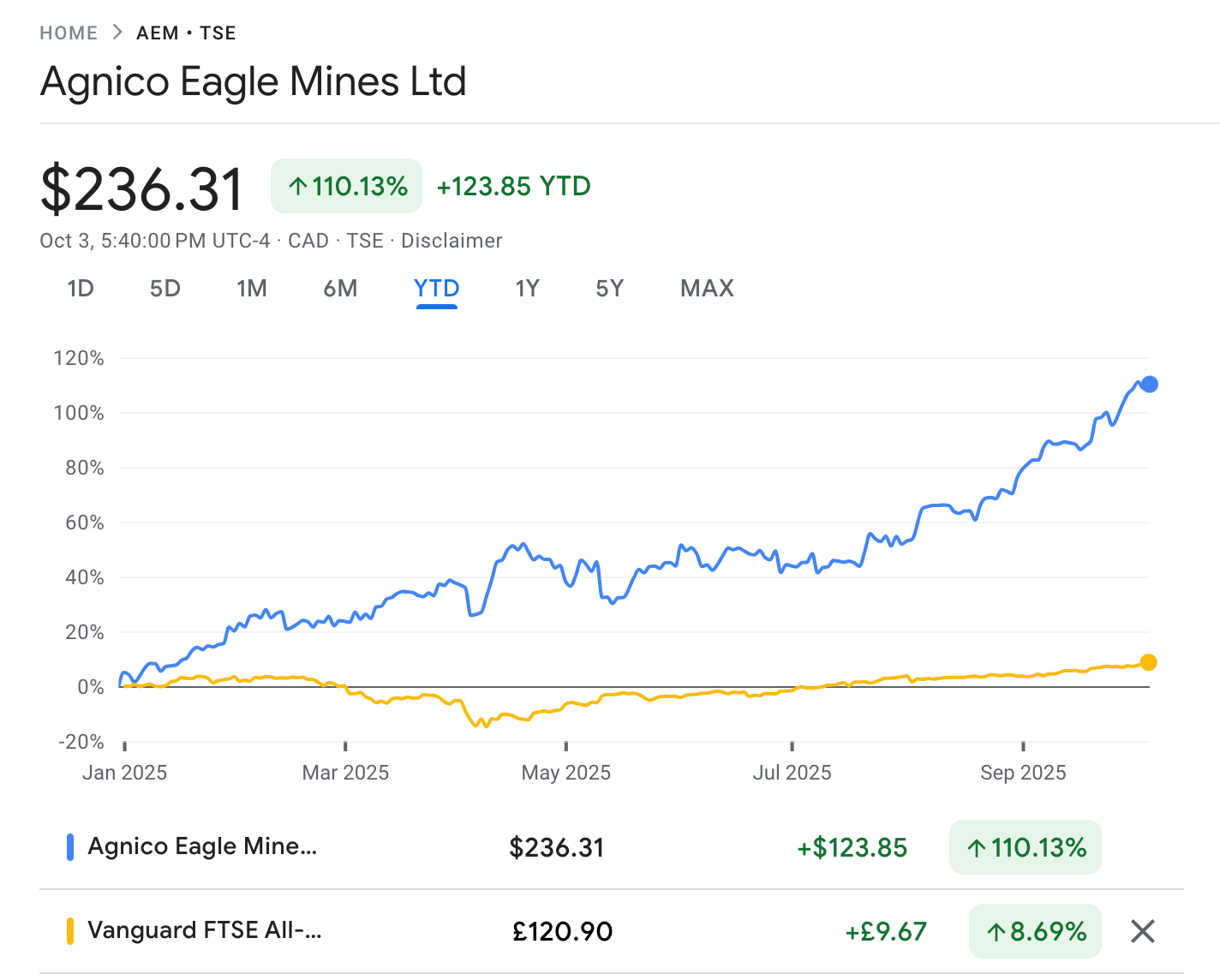

Other Value & Gold Hedge

Hard to generalize this group, but a standout has been Agnico Eagle (AEM), now a 3-bagger. It’s been a clean levered play on gold, and as investors rush toward the metal, AEM has soared.

I’ve set stop-losses to manage downside — no point letting greed overwrite discipline. Some profits may be rotated into gold itself, to balance the exposure.

All in all — a solid quarter, modest gains, and not much to tinker with. Markets will do what they do; the best we can do is stay the course and let the stories unfold.

Happy investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.