Love Dividends, but Don't Chase Them!

Some scenarios & some personal history with dividends

I have always been enamoured by the simple concept of dividends. It is like interest, but with the optionality of the interest growing (or declining) with time. When done right, investing in dividend paying companies can be excellent investment thesis.

At its core, the general thesis goes something like this. Let’s call it Situation D:

Company earns profits

Company pays some of it in dividends1

Company retains the rest to re-invest in the company

Because the company re-invested in its profits, company can earn more profit, so rinse, repeat, but now at a higher level

This narrative is however, too simple. Because in recent years, the following has also been a successful strategy, specially for tech companies. Let’s call it Situation G:

Company earns profits

It reinvests small part of it in growing the business

It retains the rest as cash for acquisitions. Every few years, it pulls off an acquisition, and the acquisition is presumably, additive in profits.

Company buys back stock to cover for dilution, but otherwise, doesn’t pay anything back to shareholders, but…

The book value, and in turn, the market-cap of the company grows and grows.

Both are very successful stories. But either can easily go wrong.

Imagine this alternate story for situation A, mathematically titled Situation A':

Company earns profits

Company pays dividends, and reinvests and blah blah blah

A few years later, Eventually growth kind of stalls but company builds a reputation for paying dividends, and the stock price is anchored to the dividend.

Eventually the company has one (or more) bad years, the company has to either cut the dividend. Stock tanks.

But the CEO of our investment is smart. She doesn’t cut the dividend, but instead borrows to pay the dividend as she knows that it will eventually all be right.

It does not become right. The company has debt, little profits and voila, the dividend has to be cut. Then the stock drops.

So, perhaps dividend paying companies are bad? Not really, because imagine this alternate ending for Situation B, now consistently called Situation B':

Company hoards cash, but doesn’t find acquisitions

Eventually finds an acquisition, but other companies are interested too.

The Company’s CEO is hell bent on winning this deal. He bids and bids and bids up the price in order to win the love of target’s shareholders.

Eventually he wins, the target is acquired

The acquisition is a mess. The culture doesn’t fit. Synergies don’t show up.

Eventually the CEO (or his CFO) writes off the whole acquistion.

Shareholders got nothing from the profits generated by the company in the past.

So, if A can turn into A' and B can turn into B', what should be the approach of we investors?

If we are long term investors, as we all presumably are, the first thing is to recognise that all of our investments can turn bad in the future, regardless of how good their past track record is. We can fool ourselves into believing that when we see the first sign of trouble we will exit the company thus timing it perfectly, but that’s easier said than done. In practice, you might get it right2 at best half the time if you are really good at it.

So, the simplest solution is diversification. Diversify just enough that if your thesis goes wrong in a small proportion of your holdings, you are well covered.

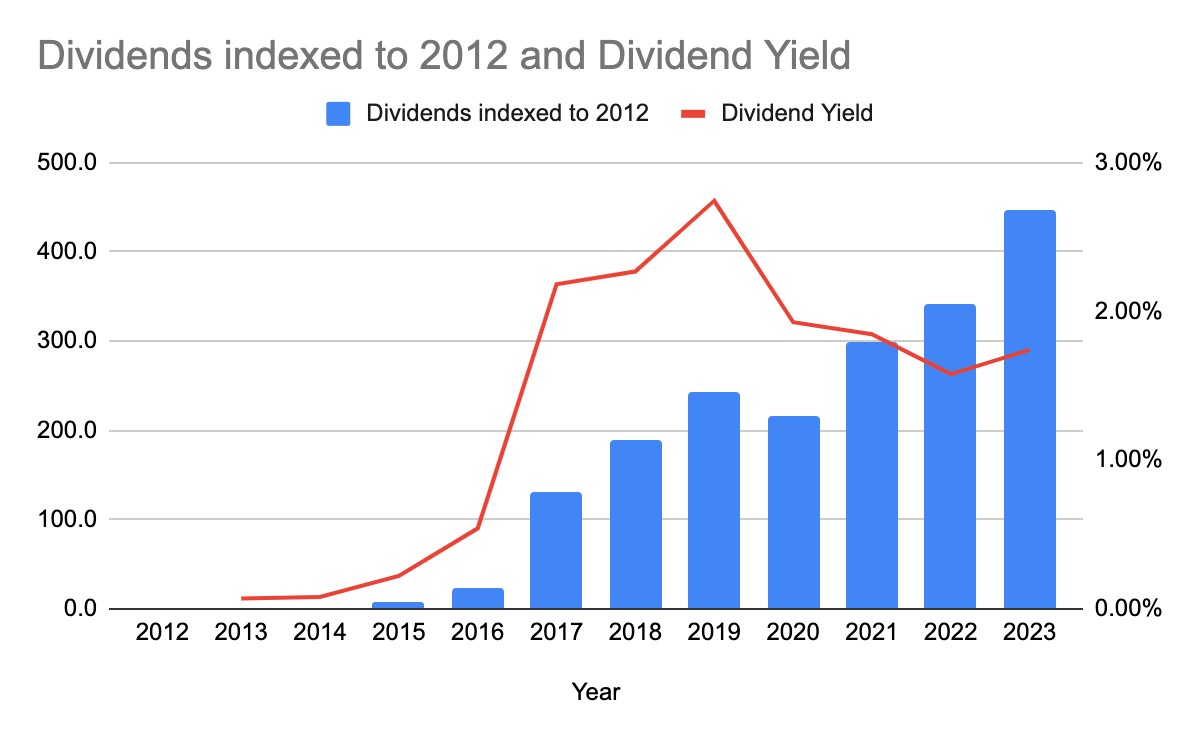

Coming back to dividends and investing, I want to share some personal stories from dividends. Here are my dividends per year, indexed back to 2012:

Over the years my dividends have grown steadily, largely because I have (a) grown my corpus by adding more to my securities portfolio and (b) because I have reinvested all my dividends. As my corpus is maturing, and as my ability to add to my corpus is slowing down, the dividend growth is also slowing down, but that’s to be expected. I eventually expect my YoY dividend growth to be somewhere in the 5%-7% range, some from the companies growing their dividend and some from my reinvestments.

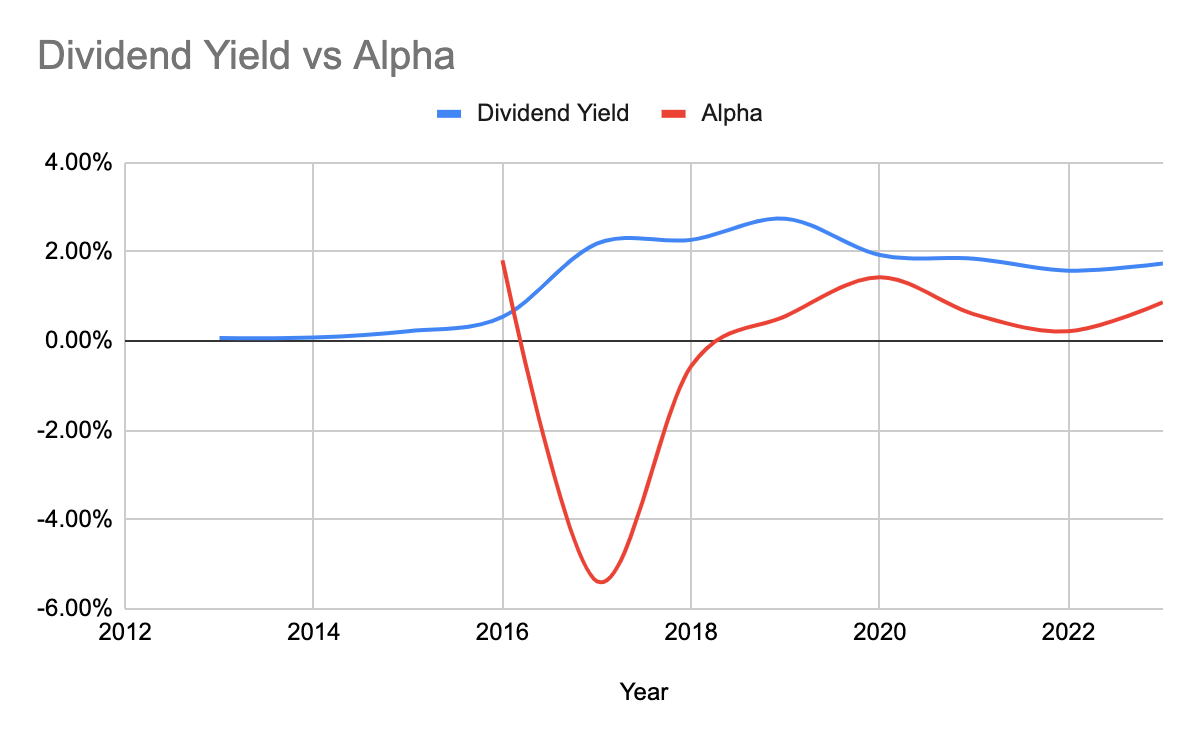

Now if you notice the right axis and the accompanying red line carefully, you will see that my dividend yield shot up to as high as 2.74% and has since pared back to 1.74% today. Why is that? That’s because I went about chasing dividend yields between the years 2017 and 2020. It was from a misguided notion that it would be better for my portfolio to do so than to focus on overall returns on invested capital. Sadly, chasing dividend yields meant that my growth suffered significantly. If there is ever a chart describing my idiocies in investing, you can’t find one more pointed that this one:

My alpha fell down significantly as I chased dividends. Bad idea! ❌

Thankfully lessons were learned, investments were restructured and now my alpha is back, albeit with a lower dividend yield. The big lesson was to invest in companies that are in a great shape business wise. If they are able to sustain (and grow) their profits from year to year, and the management is generally prudent with what they do with their money, sometimes reinvesting, sometimes acquiring and sometimes returning the money back to me, I am happy buying and holding them for long periods of time. Even in this restructured setup, my dividends have been growing steadily and I am reinvesting every penny of it. ❤️

My mantra now is “Love dividends, but don’t chase them”

As always happy investing!

Payout Ratio is the technical term for how much of a company’s profit it pays out as dividend

Getting it right might mean (a) retaining an investment that eventually turns around and compounds OR (b) exiting an investment that never turns around, or at least not in the foreseeable future.