Learnings from Equity based Decumulation

Systematic Withdrawal Plan (SWP) works well

In 2018, my very-much-retired parents sold a flat in Bangalore that they owned. In the years leading to that, they were receiving a bit of rent from the said flat, which provided a bit of cashflow, but wasn't close to the kind of yield they could have generated from the same amount of money being in liquid forms - bonds or equities. As they were going through the process, they asked me what's the best thing to do with the money they were about to receive from the sale.

The natural response to this situation is to invest the money into safe money-market or government funds or fixed deposits (FDs) or annuities that would yield a safe return and not risk any loss of capital.

I evaluated the options and wasn’t impressed with the rate of return on any of the options, with most of them yielding between 6%-8% p.a., in India, where inflation was close to 5%-6% p.a. each year, and equities were doing 12%-14% p.a. over the long term.

Even though interest rates worldwide have gone up today, so has inflation and the problem faced by my parents then is relevant today and is probably one we will all face even in the future. So I was very much interested in finding a solution that had the following characteristics:

There should be a steady stream of cashflow that my parents can use for their day to day expenses.

Such a stream of cashflow should ideally run till they lived, specifically accounting for, fingers-crossed, good longevities.

There must be scope for increasing the cashflow if they so desired based on inflation and other needs1.

In addition to changing the cashflow amounts, there must be flexibility of change in the future - i.e. being able to reverse the decision if one wanted, even if such a reversal came at a cost.2

This arrangement should come with minimal intervention.

As a plus, the corpus can be passed on in inheritance.

With these in mind, I suggested that they invested all of their money in a couple of equity based funds in India, and then set up a Systematic Withdrawal Plan (SWP), in which the fund manager sells a small portion of your holdings every month to send you off a fixed-amount cheque each month. The remaining units continue to stay invested in the market.

If you keep the rate of the withdrawals in the SWP close to the expected long term returns, perhaps leaving a small buffer for safety, you can receive a much higher yield. In India, expected returns were 12%-14%, so we could keep the SWP as high as 10% which is a very healthy return strategy and ticks all the requirements checkbox above.

The consensus is to call this approach Decumulation. You are essentially doing the opposite of the accumulation years - where you would accumulate each month by buying a bit of equities - in decumulation, you sell a small amount of your equity holdings each month to fund your retirement.

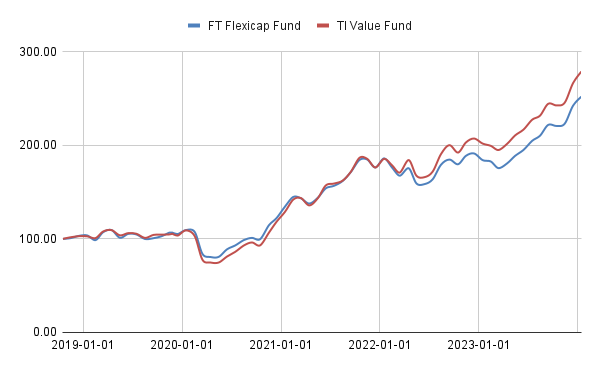

In India, setting this kind of arrangement is relatively easy, so this needs little intervention. We chose Franklin Templeton India for this. The corpus is split between Franklin India Flexi Cap Fund - Direct Growth and Templeton India Value Fund, and the drawdown was set to ~9.7% per year.

Performance of this approach

How have the funds done themselves? It had a rocky start in the early days - in 2019, the funds went nowhere, and then they took a bit of beating during the onset of the pandemic, but since then the funds have been on a tear right up to the beginning of this year. Happy days indeed, but past performance is as they say..

The chart below show their performance indexed to 100. All performance numbers listed here are net of fees.

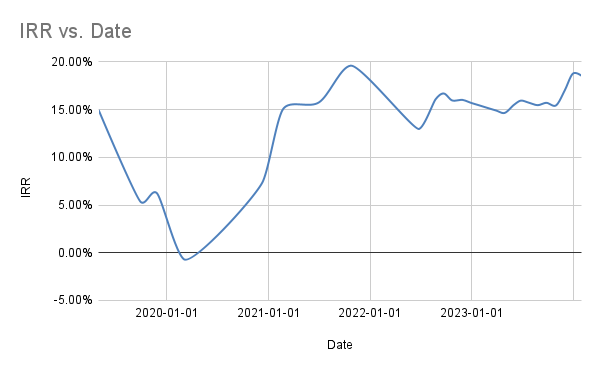

As it stands today, their corpus has grown significantly while they have been enjoying some money along the way. I went and looked at the returns on an ongoing/cumulative basis, and following the fund performance the IRR has swung wildly in tune to the market performance themselves. With time, as should be expected, the cumulative IRR seems to be stabilising now in the 15% p.a. range (give or take a percentage), and these returns are net of all fees.

I find that this strategy has worked reasonable well, at least over the past 5+ years, despite some market idiosyncrasies. All else being equal, it might work for many more years, if not decades.

Obviously, if you live outside of the India, entrusting your retirement corpus on to a fund in India and hoping it will all work out, is probably a bad idea.

If you aren't invested in India, then expecting the corpus to return 9-10% consistently without eroding permanent capital is also perhaps being too ambitious. However, I feel that this strategy tells me that I could form a similar strategy for my own withdrawal phase, after perhaps adjusting some of the numbers.

At the moment, it looks like holding a global index like FTSE Global All Cap Index Fund, and then aiming for a drawdown of 6-7% should work out reasonably well for those living outside of India.

As for the future of my own Coffee Can Portfolio, I expect to combine the dividends and a slow decumulation, similar to what is described here, to be enough to fund a retirement, assuming that the corpus is big enough by the time I retire, which is very much the hope here.

As always, Happy Investing!

Disclaimer: What’s mentioned in this post is strictly for educational and entertainment purposes only. I am not your financial advisor and bear no fiduciary responsibility for your actions. Do your own due diligence, or consult a financial advisor before investing in any securities or planning your retirement.

The reason I am writing this post now is because my parents just asked me to increase their monthly payouts and that set me on the path of reviewing things and got the material for this post. In the interest of transparency, a previous version of this post was written by me here, but has been updated for numbers.

This is in contrast to what happens with annuities, where such decision is permanently locked in

Great insights and pointers Srini 👍