Have you hit your Financial Equilibrium?

Have you hit your Financial Equilibrium?

Target Financial Equilibrium first and multiply your options in financial life

Are you worried about achieving Financial Independence?

Does it seem too daunting?

How about aiming for Financial Equilibrium first? This can be done when you build a corpus between 1/5th and a 1/3rd of your target retirement corpus. Read on to learn more.

Most people that are targeting a retirement goal often target Financial Independence - the state where they could live a comfortable life if they didn’t have a source of income. However, this is often a very large number (at 4% safe withdrawal rate, that’s 25x your annual expenses) and seems daunting.

They will get there, as surely evidenced by the successful retirement of the past 1-2 generations, but so much of their life decision making goes into worrying about this daunting aim. For instance, people work longer hours, more stressful jobs, take more capital risk, reduce their life style etc. All this is understandable, as the maths often leads us to think that that’s the right path.

However, let me propose a different path forward. Aim for Financial Equilibrium first. What’s Financial Equilibrium?

It is that point in your investing life where you don’t need to put away any more money into your retirement corpus, but you don’t yet actually retire. Your capital is working in the background, compounding away, while you are free to keep your month to month (or year to year, to smooth away minor distortions) expenditures in equilibrium - spend what you earn. Or earn what you spend.

Illustration

Let me give an illustration to visualise the numbers. Let’s imagine an investor who starts her career at 24 and works to 65.

She starts with a salary of £30,000 per year (Current UK median salary if £34,000)

Sets aside 10% of her income each year (and 20% from the age of 55, when hopefully all childcare costs are gone). This 10% is not far off from the auto-enrolment pension default of 8% in the UK and I don’t think it is super aggresive.

Her salary grows by 2% in most years, but every 5 years, she gets either a promotion or a bigger raise, putting her salary up by 5%.

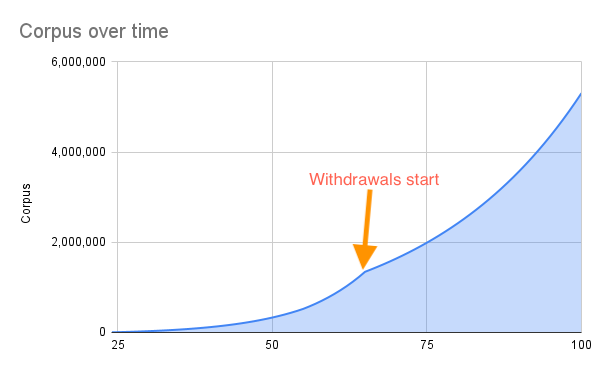

If her wealth grew by 8%, she would be left with £1,344,759 at retirement and at a safe withdrawal rate of 4%, she would enjoy growing retirement incomes starting with £53,790 in the first year and end with a whopping £5,306,540 as corpus at the age of 100, possibly for passing on to successors.

The reason for ending up with so much in corpus at age 100 is that the investor is only withdrawing 4% of the outstanding corpus, but the corpus itself is growing at 8%, so it grows in perpetuity - true magic of compounding!

.

Don’t worry too much about the assumptions here - I don’t expect anyone to live this life. Most people’s life will go through ups and downs, and no investor is going to earn 8% consistent growth over their life time, but that’s not the point. The point is to draw a benchmark so we can discuss the next point in the illustration.

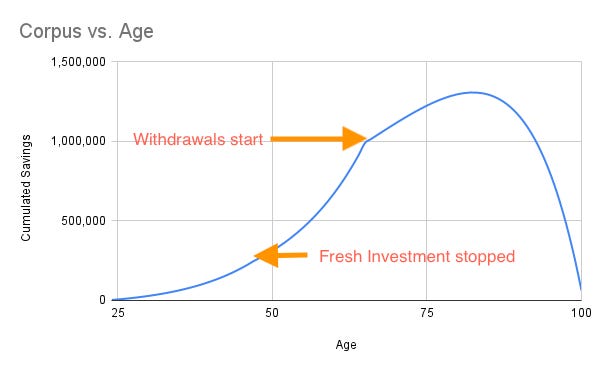

Now if she stopped investing at the age of 47, when she had £267,603 in her corpus, and does nothing but let it compound, she would still end up with £990,140 at retirement and even if we keep the withdrawals the same as in the previous case, her money wouldn’t run out till 100!!

The reason the slope on the latter part of this second curve is so steep is because we are not just withdrawing 4%. We are withdrawing the same amount as in previous case. So, lifestyle choices at retirement are exactly the same as with the previous case, which happens to be 5.43% in the first year and gets bigger and bigger, as the corpus is smaller than the base case.

Result: Build corpus from 24 to 47. Let it compound to age 65. Live off it till age 100. Let that sink in!

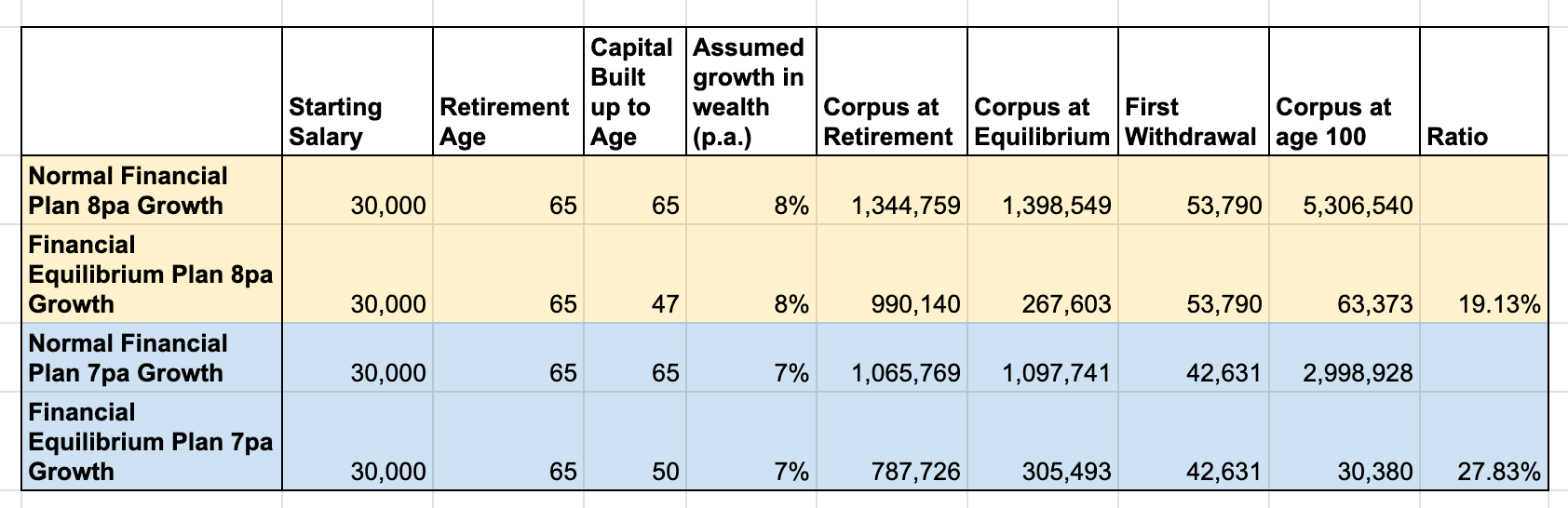

I re-ran this simulation with a 7% growth. I still get healthy numbers, but she would have to invest till age 50 to achieve a corpus that won’t run out till age 100.

Result: Build corpus from 24 to 50. Let it compound only at 7% p.a. to age 65. Live off it till age 100. Incredible!

The point at which our exemplar investor stopped investing (ages 47 & 50 in the two growth scenarios) is the point of Financial Equilibrium. Note that in one case, Equilibrium was achieved when less that 1/5th of the desired end-corpus was achieved, and in the second case, just over a 1/4th. Given how low it is to our often desired state of Financial Independence, this should be our first milestone as long term investors.

As mentioned below, these simulations are over-simplistic and would need to be customised for each person’s life needs. However, it is possible to come up with some reasonable estimates within 30 minutes of hacking around with Google Sheets. If you have a Financial Advisor, then ask them to prepare one ahead of your next meeting.

Want some inspiration? Here is the sheet I used for this analysis. Feel free to use it.

Dependencies

There are some dependencies to the success of such a strategy:

Starting your investing journey early. If you start late, then your financial equilibrium point will be reached later in your life.

Very very long term thinking & extreme diligence. This investor methodology works only because money is being let to compound at very long periods of time and is diligently invested in well returning asset classes. If you are too conservative, then the growth just won’t be enough to get you to financial equilibrium soon enough.

Needless to say, leaving your long term corpus alone.

Optionality at Financial Equilibrium

Now that we have discussed what Financial Equilibrium is, and seen some illustrations, and discussed the necessary ingredients for the success of this methodology, let’s see what benefit is bestows upon investors who achieve it.

Plan 0 (Default): If you are fortunate to still have excess income, the option to put it away for financial independence or increasing your retirement wealth i.e. this is what most people do by default.

Option to cut down your work to match what you need to run your day to day expenses.

Option to take up an aspirational job but with a lower income - perhaps a startup where you can have more fulfilling work1. Or start something of your own so long as you don’t need your retirement capital.

If it feels constrained, option to take your lifestyle up a notch. Spend a bit more on things you love2.

Headroom to fund things that makes you happy - be it a hobby or a charity or that venture that your nephew or niece wants to give a shot at.

Finally, option to invest in blue ocean asset classes3 - start-ups, self-business, cryptocurrencies, penny stocks, NFTs, growth stocks, YOLO options, meme stocks - whatever floats your boat.

I am sure there are other such options we can think of. The point is to encourage the reader (or their financial advisor) to think of alternate ways to retirement planning that could take pressure of investing in later years of life, and possibly allowing the investor to lead a more meaningful life and career.

As always happy investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before any financial decisions.

As someone who has spent more years in smaller companies than in big ones and whose professional satisfaction has largely been derived from working in environments of high autonomy, I strongly recommend this option if one can find it. As someone who is at Financial Equilibrium myself, I wouldn’t go worrying about a higher paying job, unless it was also something better in aspects other than money.

Ramit' Sethis’ How to get Rich is a wonderful watch in this space.

If you are having fun with these investments, do them by all measures. Don’t do it for wrong reasons (i.e. envy) and then feel bad if you are unable to get good returns. Financial Equilibrium should enable a happier living, not give you a noose long enough to hang yourself.

How you have managed to explain this complex topic with sheer simplify is amazing.

Interesting and Thought Provoking ideas indeed. Very Nicely summarised. "Financial Equilibrium should enable a happier living, not give you a noose long enough to hang yourself."