Earnings Update: Facilities by ADF – H1 FY25

Margins Under Pressure, Strategy Intact

Facilities by ADF (LON:ADF), the nano-stock I recently took a small position on, has just published its interim results for the first half of FY25. As ever with a nano-cap like this, the picture is mixed, and investors need to look past the immediate noise to assess whether the long-term story remains intact.

The Headlines

At the top line, revenue came in at £17.4m, up about 14% year-on-year. This uplift was helped by the acquisition of Autotrak in late 2024, which broadened ADF’s service offering. Dig a little deeper, though, and organic revenue was actually down by about 8%, reflecting delays in some productions, tighter budgets, and competitive pricing pressure across the industry.

Profitability has softened. Adjusted EBITDA fell to £2.2m from £2.5m last year, with margins sliding from ~16.7% to ~12.6%. The mix also shifted: the number of productions supported rose to 48 (vs 38 last year), but average revenue per production fell from £304k to £225k. In short, more jobs, but smaller and lower-margin ones.

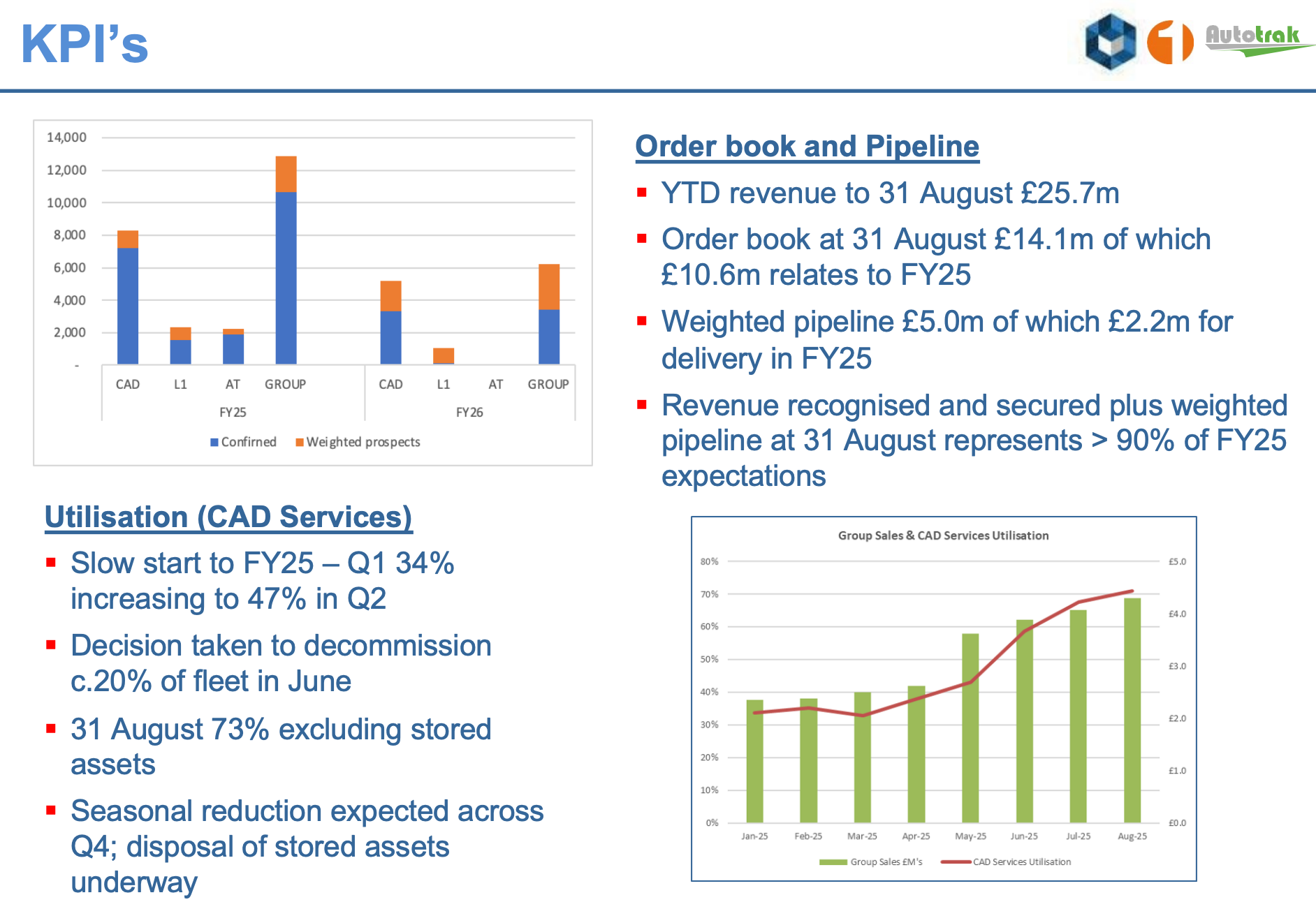

On the operational side, there are encouraging signs. Fleet utilisation, which had a weak start in Q1, has improved steadily – from ~34% in Q1 to ~47% in Q2, and to ~73% so far in Q3. Management has also decommissioned about 20% of underutilised vehicles into storage, a sensible move to cut maintenance costs and lift utilisation on the active fleet.

The balance sheet is stable enough. Operating cash flow was £4.8m (vs £2.7m last year), and net debt nudged down slightly to £13.2m. An interim dividend of 0.3p per share was declared, though this is lower than last year.

Perhaps most importantly, forward visibility remains good. As of 31 August, the company had already recognised £25.7m of revenue year-to-date. Add to that an order book of £14.1m and a weighted pipeline of £5.0m, and over 90% of expected FY25 revenues are already secured or visible.

Management and Governance

One area that merits watching is management churn. CEO Marsden Proctor stepped down in July, and CFO Neil Evans will depart at the end of October. Russell Down has taken over as Executive Chairman, and James Long has been appointed COO. Leadership changes always carry risk, especially in a company of this scale where continuity matters. That said, the core strategy looks unchanged.

The Bigger Picture

The UK film and high-end TV (HETV) market continues to grow, with production spend rising to £3.2bn in H1 FY25 from £2.9bn in the prior year. The long-term demand drivers – tax incentives, world-class studios, and a healthy pipeline of international productions – remain firmly in place. ADF is well positioned, supporting roughly a third of all UK productions by number in the half.

Still, this is not a smooth story. Returns on capital employed remain modest (3–4%), cost inflation (wages, NICs, drivers) is a drag, and the reliance on volume over pricing power makes margins lumpy. ADF is capital intensive, and acquisitions, while broadening capability, bring integration costs and debt.

My Take

When I first wrote about ADF, I described it as a niche player with a differentiated offering, operating in a market that has attractive structural tailwinds but where execution would always be uneven. These results reinforce that view.

Yes, profits are lower, management turnover is unhelpful, and the dividend is thinner. But utilisation is improving, cash flow is healthy, and the order book provides unusually strong visibility for a company of this size. The strategy – building a full-service facilities platform for high-end productions – remains intact.

This is not a stock to own if you want smooth compounding every half-year. It’s one for patient investors willing to accept some bumpiness along the way. For me, it is a rather infrequent foray into the world of nano-cap stocks and opportunity as much for education as for the alpha, though the aim remains resolutely to generate a significant upside. Put it together, and for me the long-term story remains attractive enough to stay invested. I have added modestly to my (relatively small) position on this update.

In short: margins under pressure, but the order book is the anchor.

As always, happy investing!

Disclaimer: I may hold positions in the tickers mentioned in this post. I am not your financial advisor and bear no fiduciary responsibility for your actions. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.