Summary Analysis: Sumitomo Corporation ($8053.T)

A defensive stock from the land of rising sun

Sumitomo Corporation is a Japanese conglomerate that is involved in a large number of business activities from coal mining (something they are divesting) to Tubular Business Development (something they are seeding). It started over a 100 years ago and has formed and reformed itself over the decades based on opportunities presenting themselves. In essence it is a typical Asian group that is all over the place, but seems to go on and on.

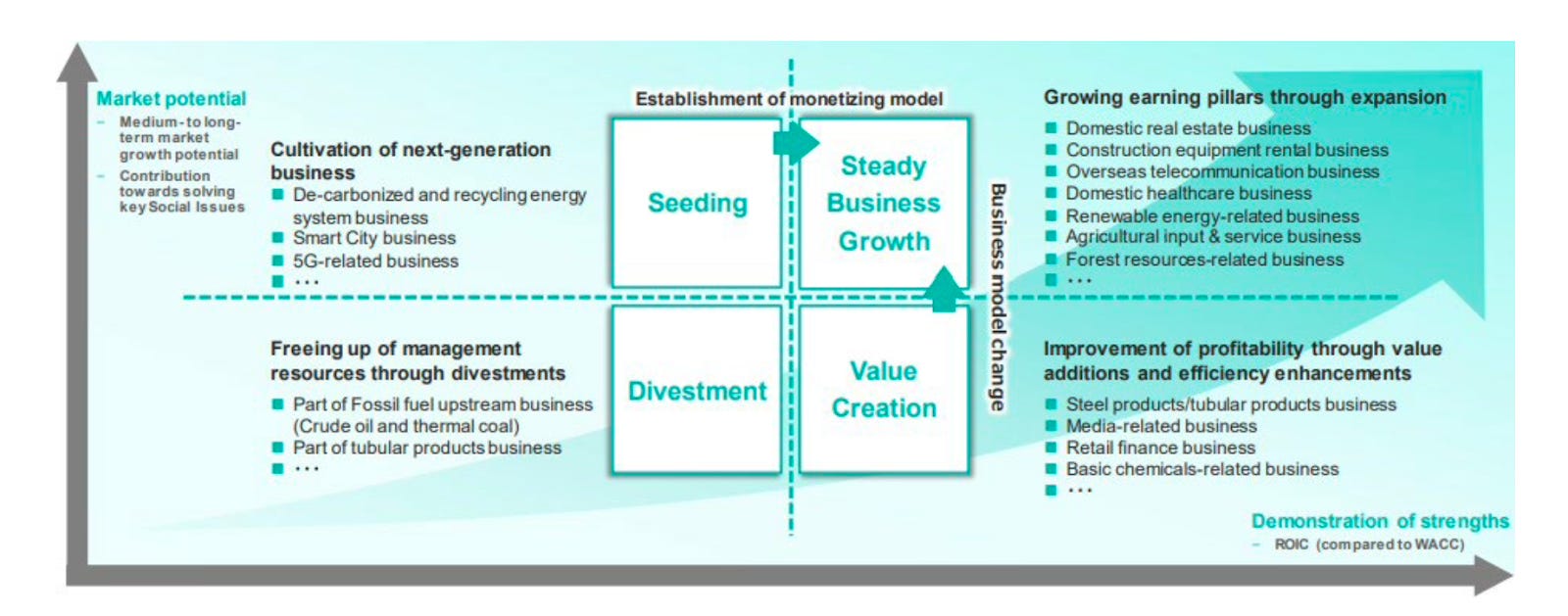

Since 2020, in its latest declared initiative, the company has been categorising all their Strategic Business Units (SBUs) into 4 categories depending on their future trajectories - Divestment, Value Creation, Steady Business Growth and Seeding. The fields of business the company cares about most today are Metal Products, Transportation & Construction, Infrastructure, Media and Digital, Real Estate and Mineral Resources & Energy.

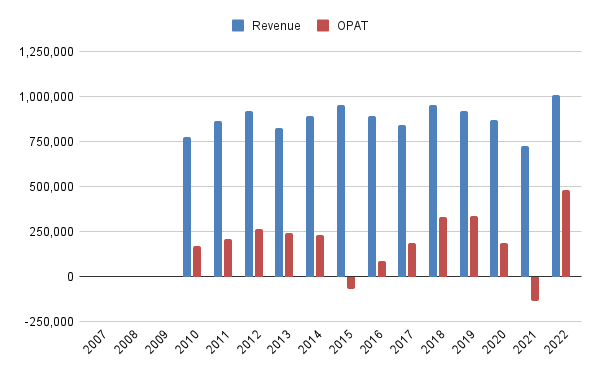

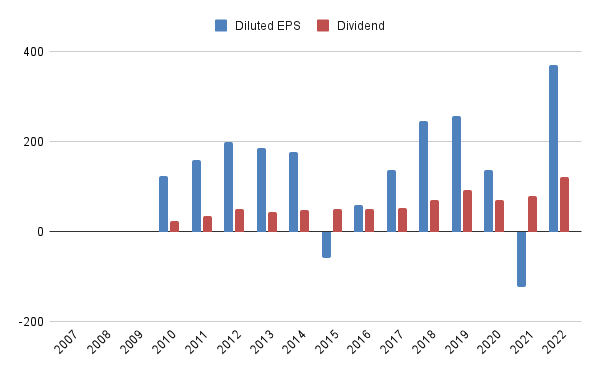

Taken together, the company represents an opportunity to tap into some Japanese style management discipline for our portfolios. Since 2010, the company has been growing revenue by only about 2.23% per year, but have been extracting about 20-21% as margins, while other metrics like Diluted EPS per share and Dividend per Share have been inching up - the business paid 24 Yen in 2010 as dividend which grew to 122 Yen in 2022, a solid growth of 9.5% per year.

Why do I like this company?

It has a consistent track record of generating incremental profits for shareholders over a long period of time1.

It has a relatively strong balance sheet covering both its short term as well long term liabilities.

They have a consistent dividend policy and have been returning boatloads of cash to investors2 - some 50% of their profits over the past 5 years, and yet their payout policy is conservative enough to tide over years like 2021 when they booked a statutory loss on the books.

It is objectively cheap - you are getting the business now at about 8x the average profits generated over the past 3 years.

What I don’t like about this investment?

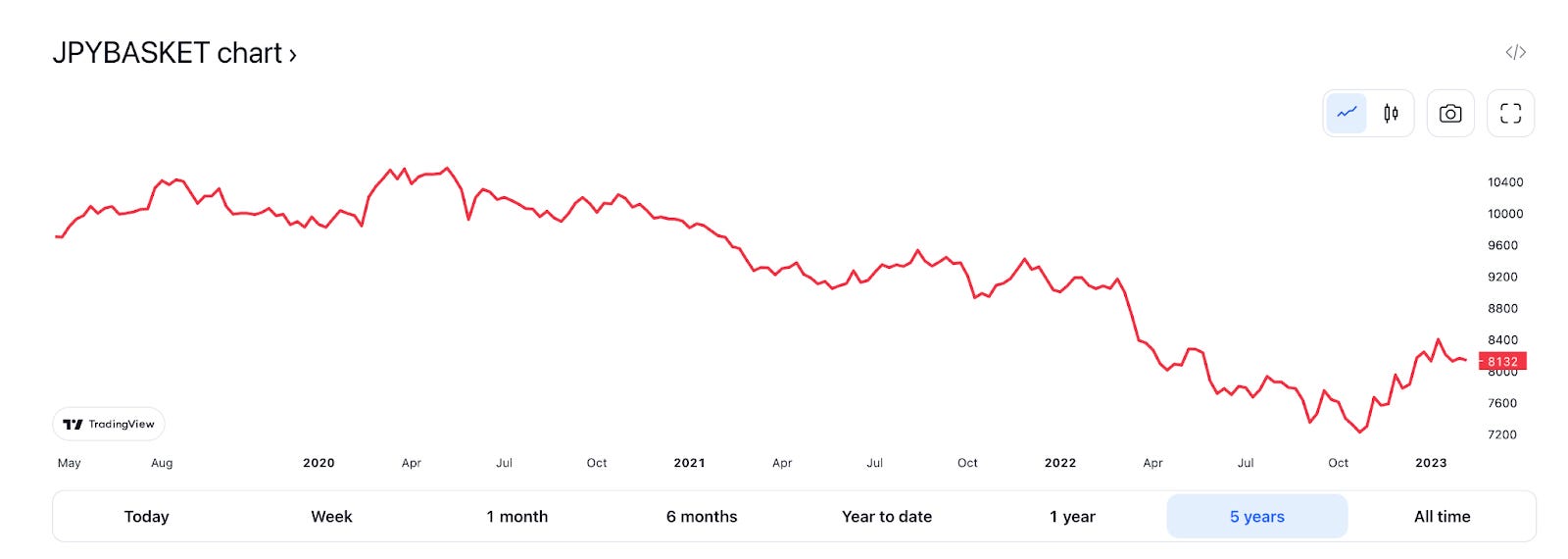

There is foreign currency risk - Yen has been dropping against a basket of currencies for a while now and the Japanese Central Bank’s decision on interest rates will have a big bearing on how the yen trades. Any stock that has significant exposure (cost or otherwise) to the Yen will have some volatility in that regard.

Closely related is the risk of the Japanese Central Bank being in a long term QE mode for a while, which also includes buying up Japanese securities from the stock market. When this position is reversed, and one should factor it in when considering a long term hold, there is a risk of having one large seller but not enough buyers, marking the price down.

Related to both the above points, the Japanese economy could be on an extended deflationary path - potentially challenging even the meagre growth rate of the revenues of the business.

Stock Logistics

The stock trades in lots of 100 - so the minimum lot size is roughly USD 1750 or about GBP 1500. It is not easy to average-buy this stock unless your general buying lots are in that vicinity. I have been buying the stock less frequently than I buy other things, precisely due to this factor.

Japan levies withholding taxes of 10-15% on dividends, depending on your residence - for UK residents it is 15%. Depending on how you own this stock and whether or not your local tax laws allow you to claim relief on withholding taxes, this might eat into your returns.

In summary, Sumitomo Corporation ($8053.T) is a defensive stock with decades of historical track record of profitable business, with a meagre growth rate, but consistent margin generation, and a growing return of capital to stockholders. I expect the share price to only grow very marginally - say about 2-5% CAGR in USD/GBP terms, but inclusive of dividend, I expect the stock to return about 5-10% CAGR in USD/GBP terms, in the good case. On the downside, I don’t expect to lose too much on a total returns basis over the next 8-10 years - an ideal combo for a defensive stock.

Programming Note: This substack has its own Twitter handle now - @coffeecaninvstr. Please follow it and share it with your investor friends.

Disclaimer: I hold positions in all the tickers mentioned in this post. This is not a solicitation to buy the stocks mentioned in the post. I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

Given the group has investments that they enter and exit, the “Share of profit (loss) of investments accounted for using the equity method” line can get a bit choppy. Regardless, the drops in income in 2015 and 2021 were both real.

Japanese stocks often have large balance sheets, but managements too conservative to do anything with it, and extracting returns from those companies can be a tricky and unduly long proposition. Having a steady dividend policy mitigates that risk.

Great article. It would be helpfull to know what the dividend yield is on current price and average price over last year or so. It seems this is a mature business growing in line with inflation/long term growth rate in World economy and pretty much paying all it can in dividends.

That being the case it would require a dividend yield significantly above 10 year Government bond rate to be worth buying. Or a possibility of getting there?

Secondly price is at all time high or close to it although in nominal and not in real terms probably buoyed by increased demand from oil sector. Does that make in that sense a higher risk stock depending on how oil sector performs.