CROX: Taking Profits on a Satisfying Win

The Boring Thesis That Returned 6x

I initiated a position in Crocs (CROX) in September 2025, drawn in by what seemed like extremely defensive pricing. The business had taken a hit, and management had absorbed a massive drawdown from their HeyDude acquisition, causing the stock to crater. At the time, I wrote:

“Yet even on these reduced expectations, the company should still deliver ~$150 million in quarterly earnings, or ~$600 million annually, translating to $10-11 EPS. That leaves the stock trading at 7.5x forward earnings, even under conservative assumptions.”

Sadly, the business did not deliver to that level. The last three quarterly results came in at $145M, $105M, and $137M, all well below my expected $150M run rate. Upcoming guidance remains soft, with revenue expected to come in 4% lower y-o-y next quarter.

The Capital Allocation Story

I also wrote at the time about the strength of the company’s capital allocation.

Meanwhile, capital allocation has been prudent (and for context, the market cap today is $4.3Bn) and last four years of free cash flows being $510M, $490M, $815M and $923M. In 2024, the company deployed $225M in repurchases at an average of $111.51/share. In the first half of 2025, $194 has been put into retiring shares at ~$102/share. At ~$80 a share, there will be more bang for the buck - lying around is ~$1.1 billion authorization for buybacks — at today’s market cap, that could retire a quarter of the company - though it might take 2+ years of FCF to generate the required cash. Yet, it is a meaningful backstop.

That thesis has very much held up. Free Cashflow (FCF) deserves some nuance here: Q1 is traditionally when the company builds and ships inventory, causing working capital to expand. The remaining three quarters are when inventory runs down and cash comes in. So the right lens is trailing twelve months (TTM), not any single quarter. On that basis, TTM FCF has been sturdy at $663M, with $520M deployed into buybacks. The share count has fallen from 56M to 50M shares since I last wrote, and repurchases over the past twelve months appear to have been made at prices below where the stock trades today, making them accretive for ongoing holders.

I was mildly disappointed by the lack of repurchases in Q1, despite the seasonally cash-light nature of the quarter. But activity has resumed in Q2: “Subsequent to March 31, 2026 and through April 23, 2026, we repurchased 0.8 million shares of our common stock for $73.6 million.”

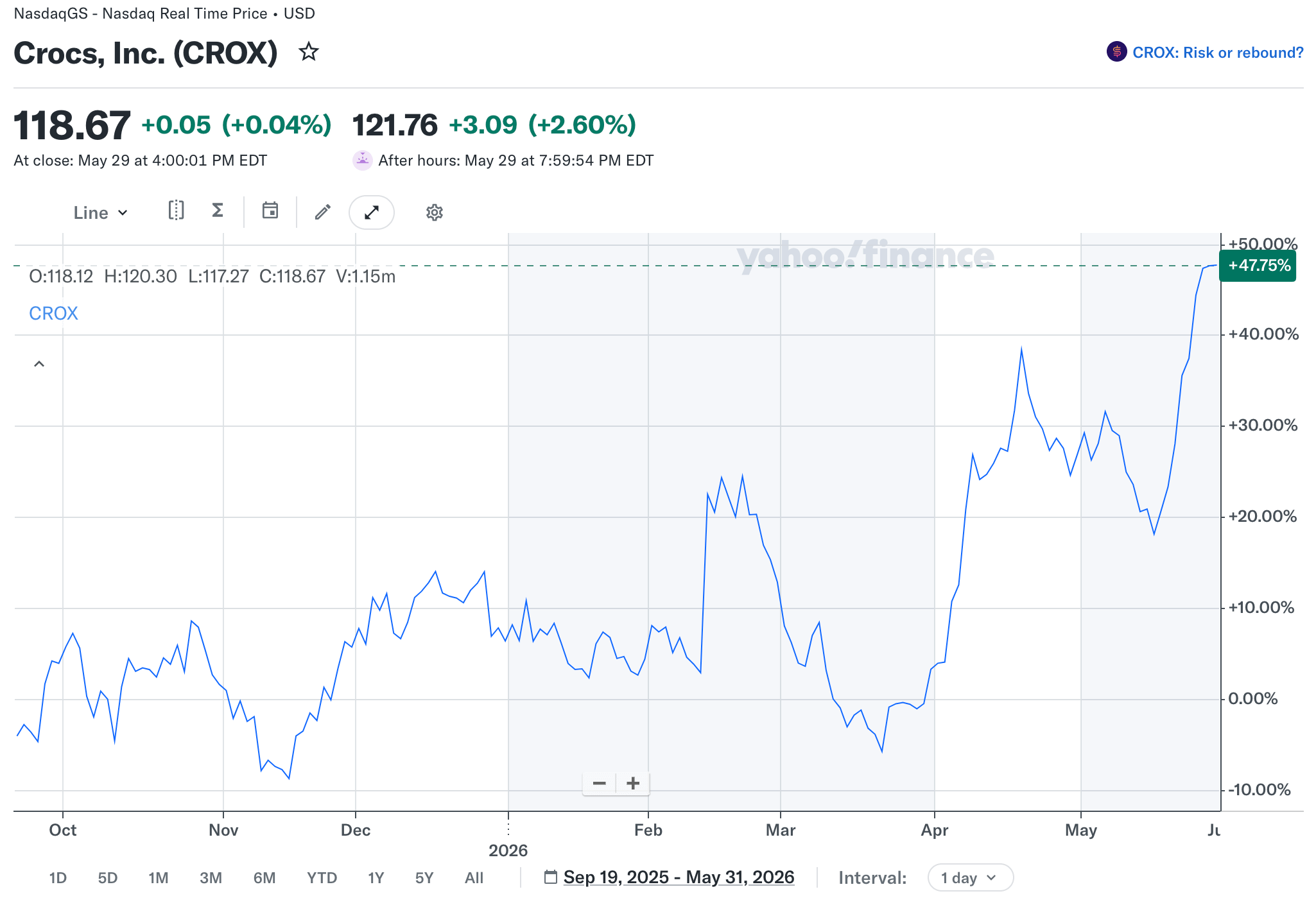

So it is a mixed story. The income side has been underwhelming. The capital allocation side has been steady. The market, to its credit, seems to have registered both: the stock is up roughly 40% since I first wrote about it.

What Actually Happened

The business did not rerate by 40%. The stock did. This is precisely the kind of opportunity I look for: a position defensive enough that, given time, you should see either a business rerate, a valuation correction, or preferably both. Here, the business did not rerate at all. The valuation simply corrected from an oversold level, exactly in line with the thesis.

I held the position through a 2028 Jan 80/85 risk reversal, which moved from roughly $6 a contract to about $40. Without putting down much cash, I was able to extract the upside, making it the best IRR position in my portfolio!

What I’m Doing Now

I’ve been thinking for a while about how to manage this position. The options structure means every move up or down gets severely magnified, and I have enough volatility elsewhere in the portfolio, not of the good kind. So I’ve decided to take profits and move some of the proceeds into CROX stock directly. This lets me retain some exposure and potentially build on it, without the leveraged profile of the options position. It also frees up some cash to enter and build positions elsewhere.

I don’t generally encourage readers to follow me into trades; everyone should evaluate their own risk. But in this case, I genuinely wish you had. A 6x return in six months is not the kind of thing value investors like me see very often, certainly not in recent years. I’ll enjoy this one.

More such wins to come, and happy investing to all CROX shareholders.

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.