Crocs: A Chequered Journey, A Cheap Backstop

Crocs, Inc. (NASDAQ: CROX) is one of those companies that sits at the intersection of fashion, comfort, and pop culture.

Founded in 2002 with its signature resin-molded clogs, the brand has had a rollercoaster of a journey on the public markets. Loved and ridiculed in equal measure, Crocs has built a global following through comfort, affordability, celebrity collaborations, and the quirky appeal of Jibbitz charms. Along the way, it has also become a case study in both operational excellence and missteps in capital allocation.

A Chequered Past in the Public Markets

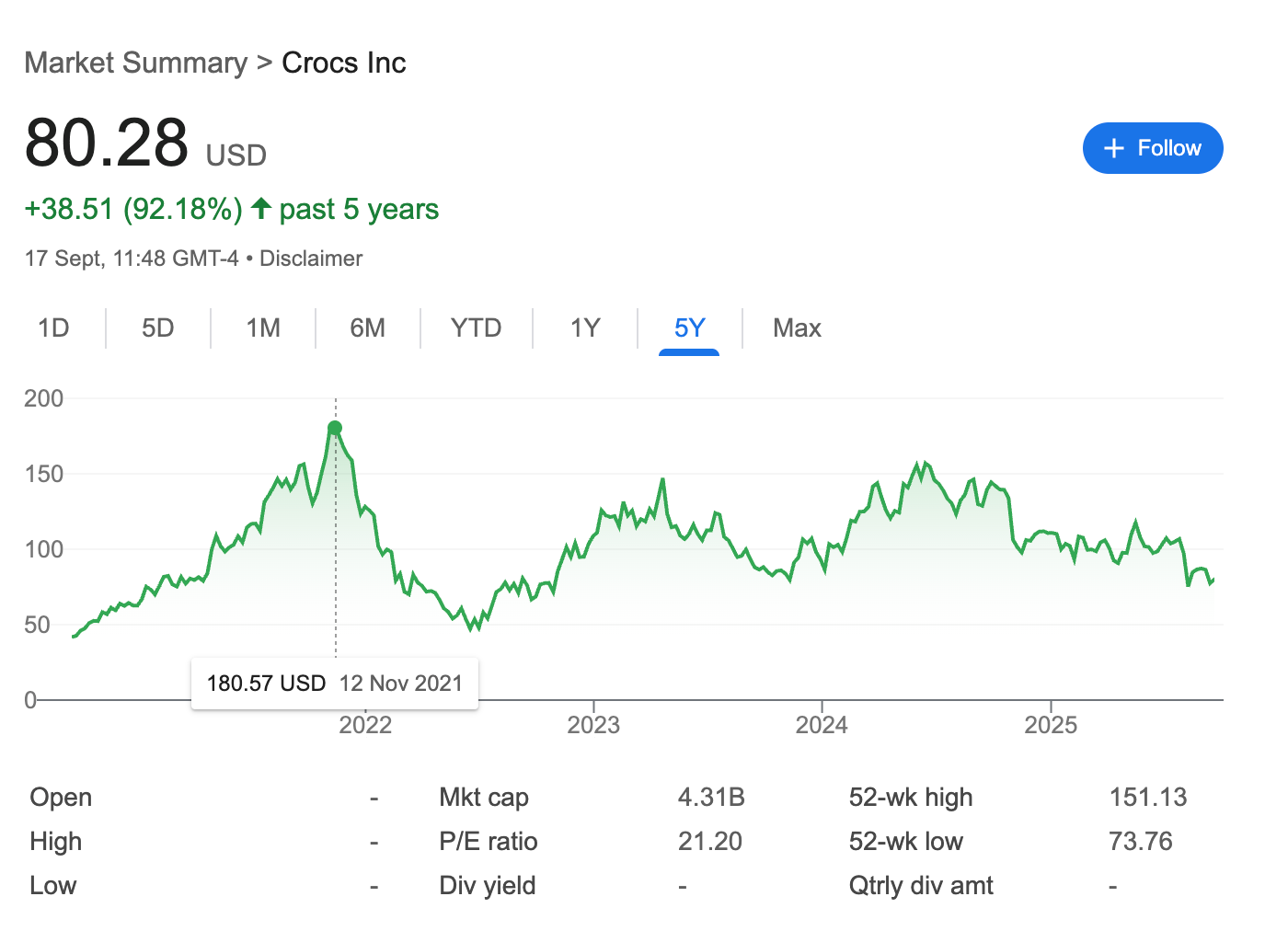

Crocs’ stock has been nothing if not volatile. From trading around ~$40 a share, it rocketed to ~$175 by the end of 2021, giving it an $11 billion market cap and a 30x trailing P/E multiple. That peak coincided with pandemic-era casualization and a wave of consumer enthusiasm.

Then came the comedown. A not-so-well-received acquisition of HeyDude in early 2022 spooked investors, leading the stock to lose ~75% of its value. Slowly but surely it recovered back toward $150 in 2023–24 before another round of negative sentiment and guidance cuts dragged it back to about $80 today — more than 50% off its highs.

This is not just volatility for volatility’s sake: it reflects the company’s chequered strategic moves and the market’s evolving assessment of Crocs’ staying power as a brand.

Operating Performance and International Expansion

Despite the stock price swings, Crocs has quietly been printing profits. Over the past four years, it generated ~$48 in EPS (with only a mild dip in 2022). Revenues have trended upwards, with international markets taking an increasingly larger share:

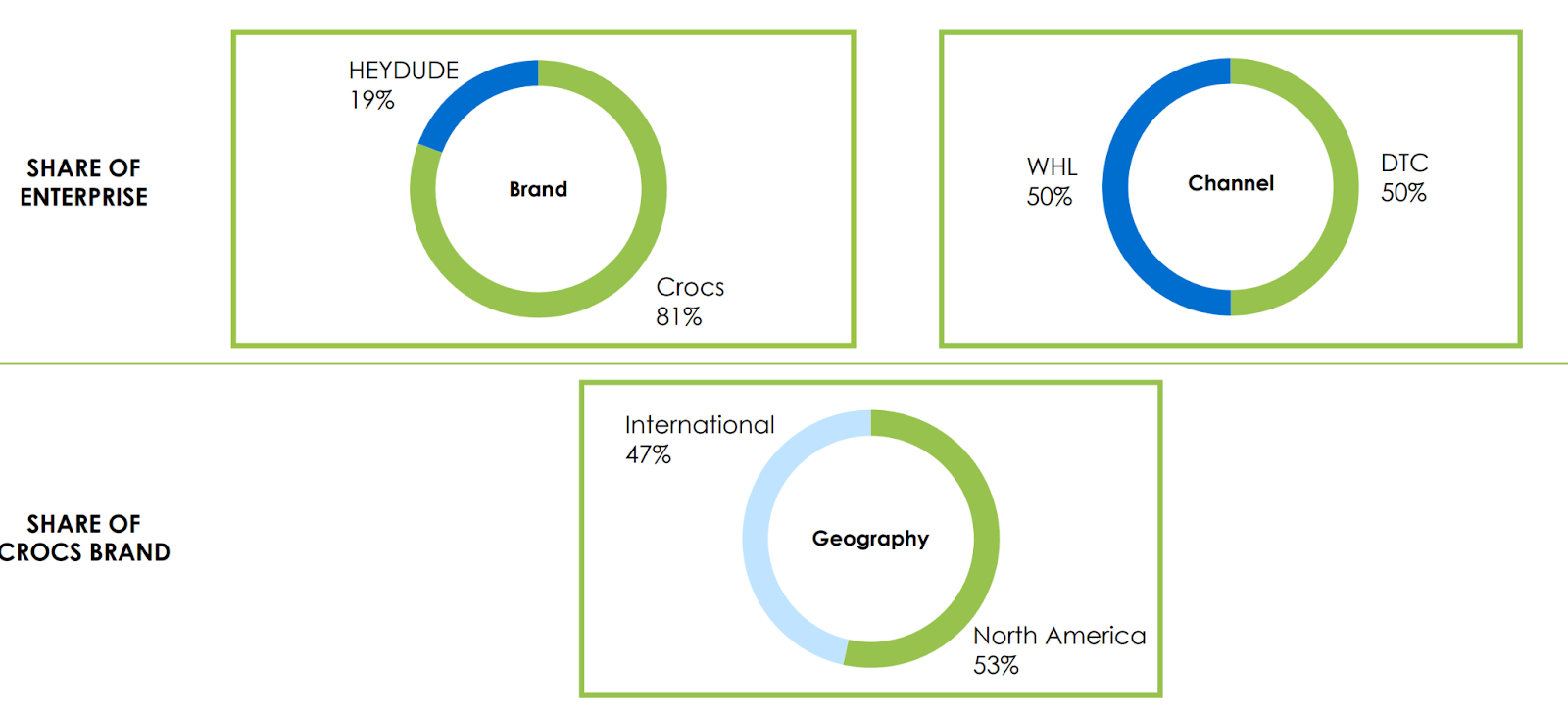

In 2022, ~38% of Crocs Brand revenues came from outside the U.S. By 2024, that number was up to ~44%.

In recent quarters, international sales even surpassed domestic, with 52% outside the U.S.

China has been a standout: 30%+ YoY growth in 2023–24, an almost unheard-of feat for a Western consumer brand in such a difficult market to crack. Alongside strong showings in Japan and Korea, this international story offsets some of the weakness in the U.S. consumer environment.

The HeyDude Misstep

At the peak of its valuation, powered by serious hubris, Crocs paid ~$2.5 billion to acquire HeyDude, a very different casual footwear brand. With lower margins, a heavy reliance on wholesale, and limited international reach, HeyDude was a stark departure from Crocs’ asset-light, high-margin DTC-driven model.

The company financed the deal with both debt and mild dilution, and as skeptics feared, the brand has struggled. By 2025, Crocs was forced to recognize impairments totaling $737 million (split between HeyDude goodwill and trademarks). This pushed GAAP EPS negative, creating the illusion of a ~20x P/E stock — when in fact, on a cash basis, it remains much cheaper.

Revised Management Paragraph

Crocs today is not founder-led; the original trio have long since stepped aside. The company has been helmed since 2017 by Andrew Rees, a professional operator who guided Crocs through its renaissance years. It was under his watch that the ill-fated HeyDude acquisition took place — a deal that in hindsight reflected more hubris than discipline.

But to his credit, Rees and his team have faced the consequences head-on, recognizing impairments and adjusting guidance rather than kicking the can. The broader picture is that Crocs remains relatively well managed: it has delivered strong international growth, generated consistent cash flow, and pursued shareholder-friendly buybacks. Recent CFO turnover underscores that the board is not complacent; instead, it appears to be pushing for sharper financial discipline. The incoming CFO, Patraic Reagan (ex-Nike), joins at a time when Crocs is cutting costs, tightening inventory, and taking a more conservative approach to guidance — all evidence that the company has learnt the right lessons and is intent on balancing bold bets with fiscal prudence.

Guidance Cuts and Macro Headwinds

Adding to investor unease, Crocs recently guided down Q3 revenue (-11% YoY) and operating margin (to 18%) and removed forward guidance. Management cited both softer consumer demand and tariff pressures. At face value, Q3 earnings could land closer to ~$160 million — a 40% decline versus last year. Not pretty reading.

Yet even on these reduced expectations, the company should still deliver ~$150 million in quarterly earnings, or ~$600 million annually, translating to $10–11 EPS. That leaves the stock trading at 7.5x forward earnings, even under conservative assumptions.

While many investors instinctively view the withdrawal of guidance as a red flag, adding to the downward pressure on the stock price, I’d argue it may actually be a healthy development. Crocs’ leadership is facing a volatile mix of tariffs, consumer demand shifts, and brand repositioning — forecasting in that environment is more guesswork than science. By stepping back from the quarter-to-quarter numbers game, management frees itself to focus on operational execution rather than trying to manage Wall Street’s expectations. My largest holding, Berkshire Hathaway has long been an example of a company that thrives without formal guidance, and I have had no problems owning it with metric tonnes of conviction. The way I see it, short-term investors may be exiting now, leaving room for long-term holders to step in — and when the fair-weather crowd eventually returns, it’ll likely be at a higher valuation, which is exactly where we’d want to be celebrating.

Valuation and Capital Allocation

This is where the story gets interesting.

On a trailing basis, Crocs typically trades in the 12–15x P/E range.

Not visible in the graph above (and properly misleading for the casual looker), adjusting for non-cash impairments, it trades today at ~4.5x (and not 20x!) trailing and ~7.5x forward — at the bottom end of its historical band, and near the panic levels last seen around the HeyDude acquisition in 2022.

Meanwhile, capital allocation has been prudent (and for context, the market cap today is $4.3Bn) and last four years of free cash flows being $510M, $490M, $815M and $923M. In 2024, the company deployed $225M in repurchases at an average of $111.51/share. In the first half of 2025, $194 has been put into retiring shares at ~$102/share. At ~$80 a share, there will be more bang for the buck - lying around is ~$1.1 billion authorization for buybacks — at today’s market cap, that could retire a quarter of the company - though it might take 2+ years of FCF to generate the required cash. Yet, it is a meaningful backstop.

Summary

The bear case is straightforward: Crocs could be past its peak. If brand momentum fades, HeyDude continues to disappoint, and tariffs weigh further, the stock could see another leg down.

The bull case is equally clear: At 7.5x earnings, with a strong cash-flow engine, ample buyback authorization, and still-growing international markets (especially Asia), the stock has a cheap backstop. If earnings hold steady or surprise modestly to the upside, the multiple could easily re-rate a turn or two higher, delivering attractive returns.

Crocs is not a flawless company — it carries the scar of a misjudged acquisition and operates in a fickle, trend-driven industry. But it is also a cash machine with a global growth engine, particularly in Asia, and a management team disciplined in capital return.

As in some of the recent posts I have written, I am tending to bias towards strong brand, strong growth companies that have suffered recent downfalls, and when those companies have good balance sheet, capital allocation, and backstops powered by it all - think of Harley Davidson, Stellantis etc.

At today’s valuation, the bad news seems more than priced in. In balance, this looks like a reasonable place to step into the stock. Given the ample options liquidity, one way to express this view is via an 2028 Jan 80/85 risk reversal - which is what I have employed to take a small position, which could be extended if I see I continued pricing and/or business improvements.

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.