Real returns is all we need to stay the course

With market throwing tantrums, fell blessed with what you get

I have attempted to get this post published the last weekend, but was interrupted by sudden stock movements. Given the volatility in the markets, I decided not to schedule this particular post and get it out when I have a stable snapshot of things. Given the markets have been relatively calm for the past 24 hours, this seems like any other time to get this out.

When volatility strikes, and the markets move as much as they have in the past few trading days, it is easy to lose sight of why we are here. We are here because we want to generate above inflation growth in our purchasing power over the long term. Put another way, the purchasing power that we are deferring over time should not only hold its value against inflation, but produce something over and above.

It is also important that in the long term, you are to expect somewhat range bound returns - i.e. good years will be followed by bad years and vice versa. Over time, the returns should somewhat revert to the mean. Since 1999, the CAGR for MSCI World index, in GBP terms, has been 7.58%. In the intervening period, inflation has been ~2.6%-2.7%. This means that global equities have returned about ~4.8%, adjusted for inflation, over the past quarter century.

Where do things stand today?

Let’s do a quick recap of how the Coffee Can Portfolio is doing.

Nominal Returns Since Inception1 (through IRR method) in GBP: 8.6%

Comparative Returns of the Benchmark: 6.6%

Alpha: 2%

UK Inflation (5-year average): 4.4%

Real Returns (Since Inception): 4.2%

As you can seen, I am extremely fortunate that the Coffee Can Portfolio seems to be catching up with the benchmark recently (though it underperformed for many many quarters in 2023 and 2024).

The remarkable observation, however, is that the benchmark has also returned 2.2% over inflation in the same period, even after accounting for the recent drawdowns in the market. This is obviously lower than the 4.8% long term real returns, but just as we are suffering serious drawdowns, being in positive real returns territory is a blessing in itself.

Where am I going with this?

If you are a disciplined investor, you are likely to get above-inflation returns over the long term, but (a) being disciplined and (b) long term is equally important. It is easy to forget it all when the markets are doing what they are doing. However, it is times like this that we should remind that this is part of the experience. Having a 2.2% above inflation returns right when things look pretty bleak, is a good reminder why we are equity investors.

The rest of this post will be about the Coffee Can Portfolio itself.

Investment Approach & Portfolio Philosophy

The Coffee Can Portfolio is built with a long-term horizon, aiming to enhance real wealth while ensuring my family’s purchasing power grows meaningfully over time. The structure remains heavily equity-based, with minor exposure to gold and no bonds. Stock selection follows these core principles:

Focus on well-run companies with strong capital allocation.

Defensible purchase price with a margin of safety where possible.

No strict bias toward under-valued stocks, but opportunistically adding when value presents itself.

Willingness to be contrarian—largely avoiding trendy tech stocks despite past holdings in Microsoft, Google, and Amazon.

Ultimately, the portfolio’s purpose is to generate returns meaningfully above inflation so that when my wife and I eventually retire, we are comfortably financially independent. Short-term fluctuations and benchmark-relative performance are secondary, though interesting to analyze.

Q1'2025: What Changed?

While this has been a weak quarter for the markets, most holdings either held up better than expected or mildly surprised to the upside. Of the 24 tickers (some being ETFs) in the portfolio, 5 underperformed in this quarter, while 20 outperformed the market. The portfolio’s relative strength came from two key factors:

The benchmark itself declined ~5% this quarter.

The portfolio held steady, cushioning the drawdown.

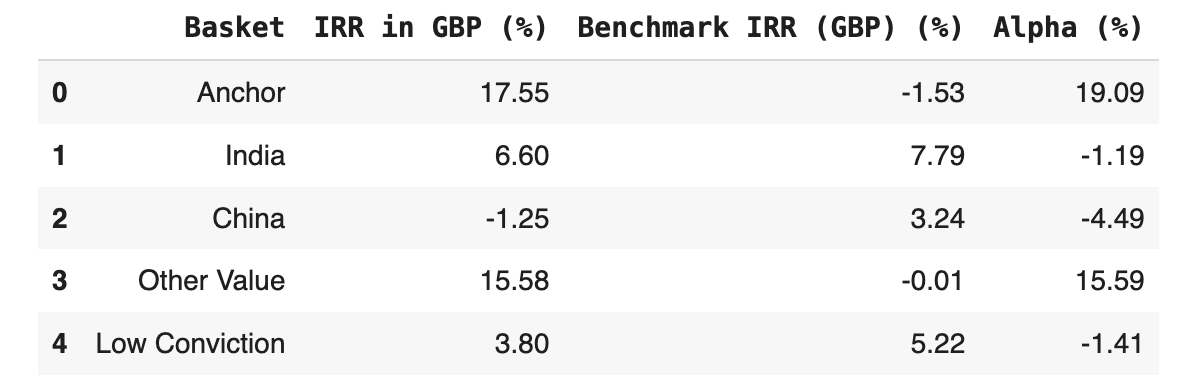

Performance by Basket

I introduced the concept of baskets in this post - please read it if you haven’t.

As you can notice that returns of the portfolio wildly vary by basket, but this is normal. Some baskets will outperform while others will lag, from time to time. The only way to get everything firing is to have too much correlation, but that’s kind of the opposite of what we want from a balanced long term portfolio.

Anchor Stock: Berkshire Hathaway

Berkshire (past writings) has been a standout performer, as the market has rekindled its interest in what was previously an out-of-fashion stock. I’ve written about Berkshire before and remain confident in its trajectory, though Warren’s increasing age is a long-term consideration.

Chris Bloomstran, an encyclopedia of knowledge on this company and a major shareholder via Semper Augustus, assigns an intrinsic value of $522 per share. The stock has now caught up with his valuation and recently traded above it, though it has also suffered some setbacks in the past week.

China: A Long Road to Catching Up

China (past writings) remains well below the benchmark, and just before the tariff tantrums kicked in, it was even close to the benchmark returns — something that seemed improbable when investors had all but written off the Chinese market. I’ve held a contrarian bullish stance on China, but with tariffs being particularly punitive on China, specifically on net exporters like Lenovo, the basket is likely to underperform some more time. The whole point of consistently adding to this basket of seven stocks was to generate substantial alpha, and I am still hopeful of it. 🤞

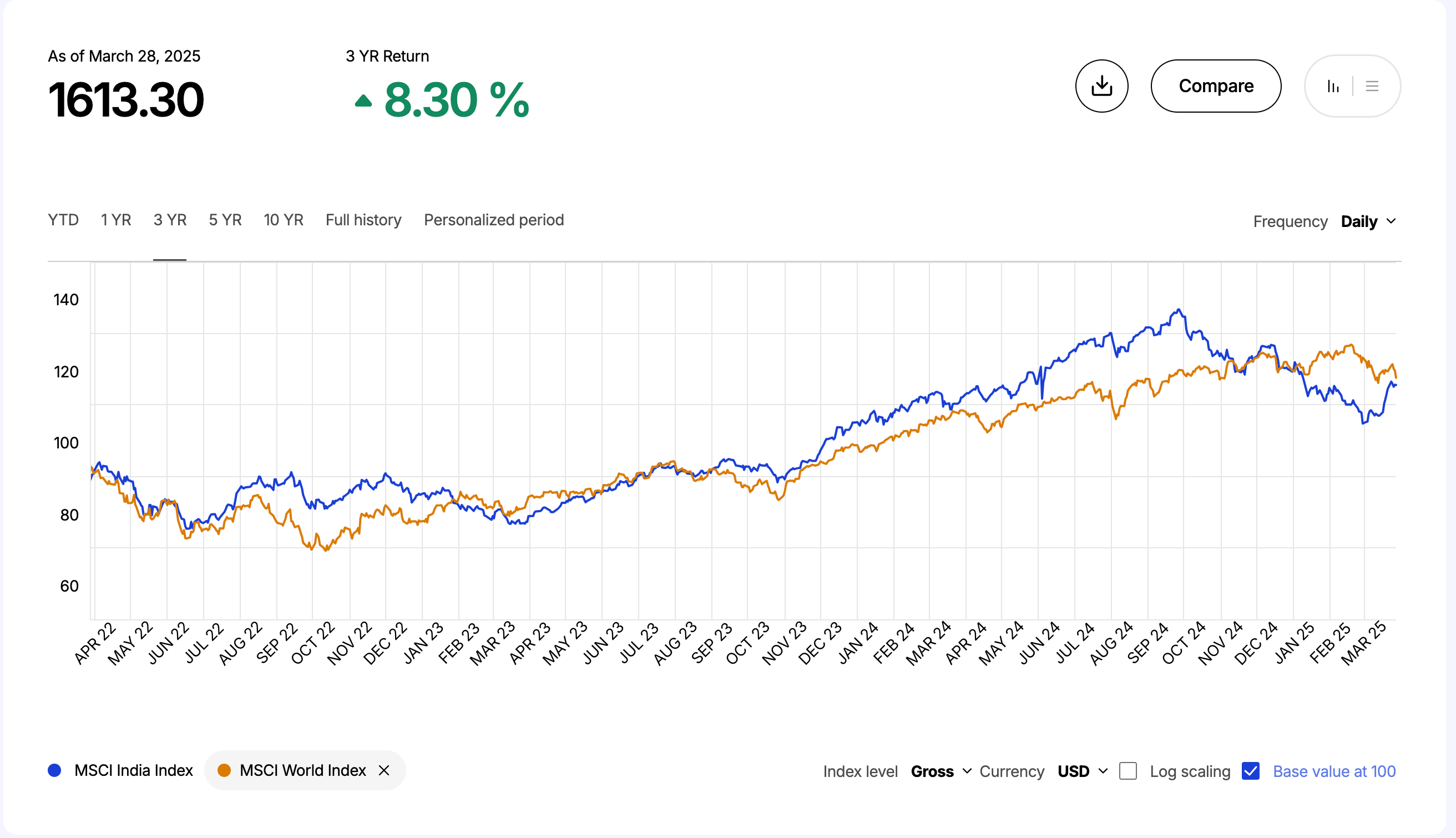

India: A Temporary Correction?

India (past writings) is among the few markets outside of the US that have kept pace with the global markets, and even generated excess returns for substantial periods of time.

Presently, India’s small- and mid-cap segments are undergoing a correction, but I’m not concerned. The combination of public policy, private investment, and broader market dynamics points to a resilient and healthy economy. I see no reason to change my position and may even add selectively.

Other Value Stocks: Steady Contributors

This segment, comprising five well-run companies acquired at attractive prices, has done well:

Winners: BAE Systems plc, Agnico Eagle Mines Ltd

Lagging but promising: Sumitomo Corporation, Bunzl plc, Stella-Jones Inc

Stella-Jones and Bunzl are currently dealing with recent weak results, but I expect them to eventually join BAE and Agnico in delivering outsized returns.

Low Conviction Stocks: A Work in Progress

The “Low Conviction” segment remains a drag, though several constituents are closing the gap with the benchmark. Between Q2 and Q3, I plan to exit some positions while consolidating others into more defined baskets.

Looking Ahead: Real Outperformance or a Lucky Quarter?

After five quarters of significant underperformance, this rebound is welcome.

However, one observation: even a broken clock is right twice a day. It’s easy to misinterpret this recent catch-up as a sign of structural advantage when it may simply be mean reversion at play. While generating solid real returns is a sufficient reason to continue with this approach, true validation will come when the portfolio outperforms even during strong benchmark rallies. Let’s see if that happens.

In the meanwhile, Happy Investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.

roughly 2020