A Deep Dive into VEU: Exploring International Equity Opportunities

Diversifying Beyond US Borders for Long-Term Growth

Let’s talk about VEU (officially NYSEARCA:VEU), an ETF explicitly created to track the universe of opportunities in the equity markets outside of the US. For those concerned about the US market's current valuation or future performance, VEU serves as a natural starting point to explore international investment opportunities.

What is VEU?

VEU tracks the FTSE All-World ex US Index, which itself is a subset of the FTSE All-World All Cap Index (minus US-listed stocks). This broader index also underpins Vanguard’s FTSE Global All Cap Index Fund, which I’ve used as a benchmark for my coffee can portfolio and discussed in previous writings.

With approximately 3,800 stocks (about half the size of the global tracker), VEU serves as the natural ex-US complement to a global index, making it an excellent starting point for thinking about ex-US equity opportunities.

Performance Metrics: A Mixed Bag

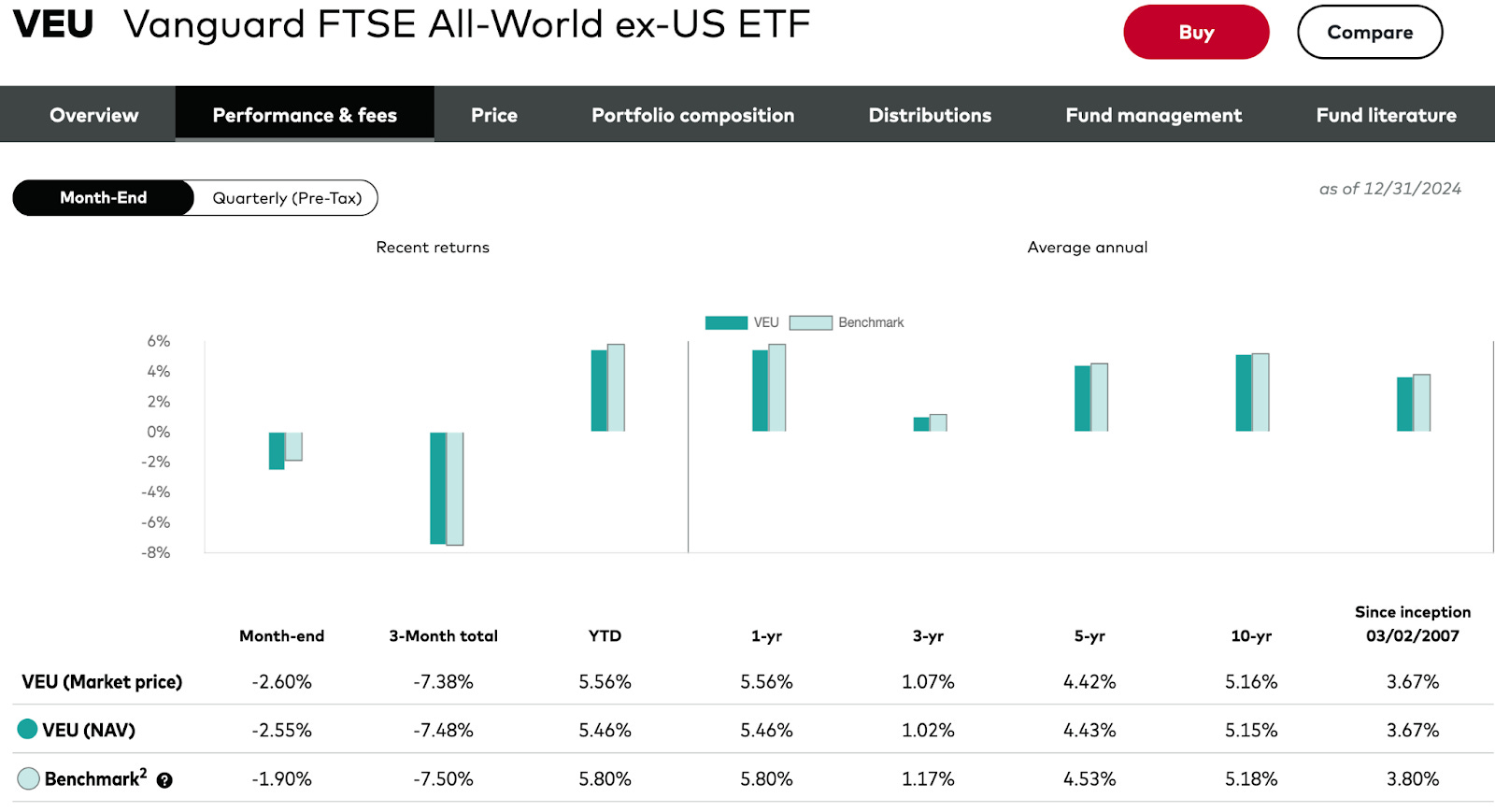

Here are the market price returns for VEU:

Including dividends of approximately 3.5%, we’re looking at a ~7% CAGR over a 15-year period. While this sounds decent on paper, for many, this translates to underwhelming returns—a potential “grave of under-performing equities.”

But does this tell the full story? Let’s dig deeper.

The Context: A Tale of Two Eras

From the mid-2011 period to today, the narrative takes an interesting turn. The 10 years prior to 2011 were lackluster for the US market:

The dot-com bubble burst.

A build-up to the 2008 peak, followed by the Global Financial Crisis (GFC).

Result: A flat decade for US equities.

Since 2011, however, the US markets have seen an extraordinary bull run, with returns approximately 4x over the past 13-14 years.

The Role of the US Dollar

This bull run has coincided with one of the largest bull runs in the US Dollar (USD):

Over the same period, the USD rose ~40% against a basket of international currencies, equating to a ~2.62% CAGR.

The connection between these two trends is pretty strong. The outperformance of US stock markets, coupled with the strength of the US bond market, has likely driven foreign investors to increasingly buy US equities and bonds, creating a self-reinforcing cycle of demand for the USD, among other trends at play no doubt.

Conversely, the 10+ years around the turn of the millennium (when the S&P 500 delivered near-zero returns) coincided with a 2.73% annual decline in the USD. This reinforces the correlation between US stock performance and the USD’s strength across both bullish and flattish phases of the past 25 years.

Implications for International Markets

Export-driven economies, particularly emerging markets, often keep their currencies weak to maintain competitiveness. By contrast, the US’s role as a net importer with a massive trade deficit has made a strengthening USD a significant tailwind for the US economy.

However, for US export-oriented companies, think magnificent-7, this presents a unique challenge, as about half their revenue is international. They’ve had to convert those offshore revenues into a consistently appreciating USD, which likely shaved off a fraction of their performance, which I believe underlines the performance of these companies in the recent past, in even greater light.

Is it at all possible that the USD is over-valued? I think so and I don’t believe I am not alone - this FT blog summarises that USD might be overvalued by ~22%.

VEU: A Headwind Turned Tailwind?

Here’s where it gets interesting for VEU. Since both the ETF and its dividends are in USD, while its constituent companies operate in non-USD currencies, the USD’s rise acts as a headwind for the ETF’s returns.

If we adjust for this ~2.6% USD headwind, the long-term returns for VEU improve significantly:

Adjusted performance: ~9.6% CAGR over 15 years.

This paints a much more respectable picture, especially for investors seeking diversification away from the US market.

Why Consider VEU Today?

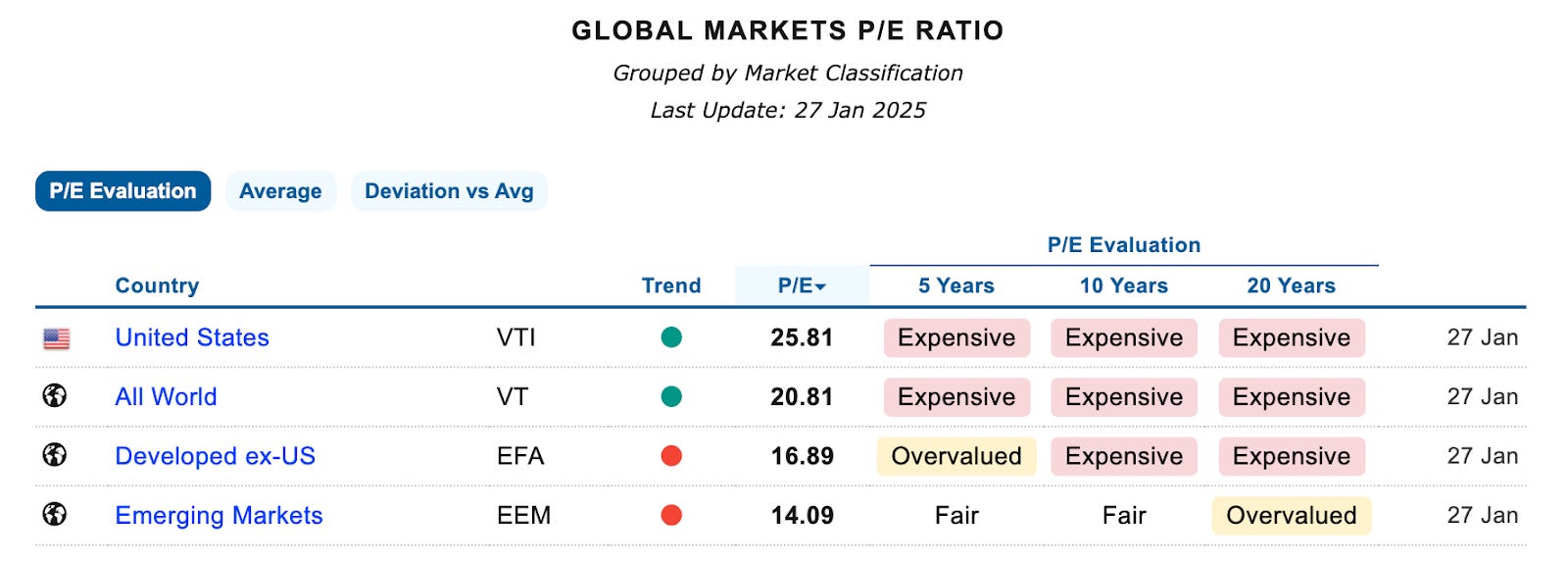

Relative Valuation: While VEU may not be cheap by historical standards, its valuation compared to US equities is far healthier.

Portfolio Diversification: If the US stock market faces tepid returns over the next decade, it’s likely correlated with weaker USD performance. This makes international exposure—via VEU—a good hedge.

Historical Returns: Adjusted for forex headwinds, VEU has delivered competitive long-term returns.

Practical Considerations

For UK and European investors:

VEU Access: VEU cannot be purchased directly in the UK or most of Europe.

Alternatives:

For those comfortable with options trading, strategies like risk reversals, outright calls, or selling in-the-money puts can provide exposure1.

Pulling It All Together

If US stock markets are headed for a period of slower growth, it’s likely to coincide with weaker USD performance.

Looking international is a valuable complement to a US-heavy portfolio allocation.

VEU offers a broad and diversified way to access international markets, serving as both a hedge against US underperformance and a potential source of attractive returns.

Factoring in currency headwinds, VEU’s long-term performance is far better than it appears at first glance. If international sentiment improves, VEU could become a very lucrative holding over the next decade.

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities.

I have built up a decent position using the combination of all the methods mentioned. I also have a IBKR Singapore based account, where buying VEU directly is possible and I might bring it to use in the coming months.