The Turtle vs. The Golden Hare

The Maths of Being Frugal

The old adage says the wealthiest person isn’t the one with the most money, but the one with the fewest needs. In personal finance, that’s only half the story. The full truth? The person with the fewest needs is the one most likely to tell their boss to “have a nice day” decades ahead of schedule.

Sounds intuitive? Great, keep reading. Doesn’t sound intuitive? Even better - read twice.

The Contestants

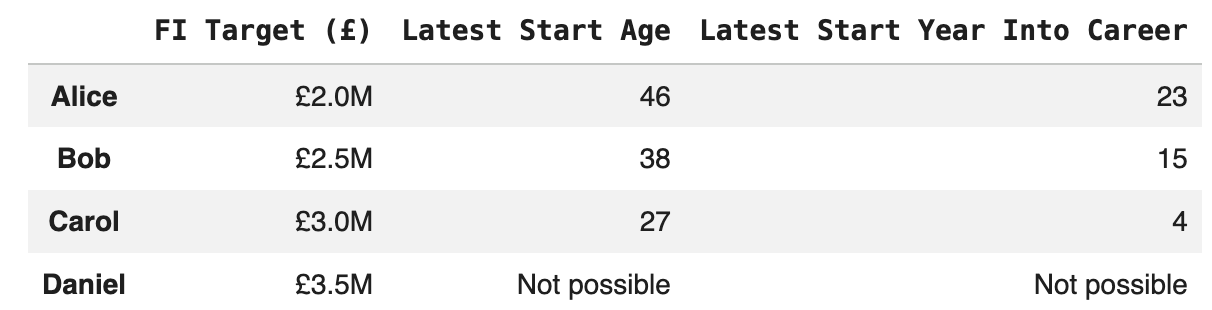

Meet our four lab rats: Alice, Bob, Carol, and Daniel. They all start their careers at 23, earning a very respectable £40,000 (roughly the UK median). They are identical career clones: 3% annual raises and a 10% “I’m essential” promotion bump every five years.

The only thing that separates them is their “burn rate”—how much they spend on life, lattes, avocado toast and Netflix subscriptions:

Alice: The Frugal Ninja (£20k spend)

Bob: The Middle Ground (£25k spend)

Carol: The Lifestyle Creeper (£30k spend)

Daniel: The Big Spender (£35k spend)

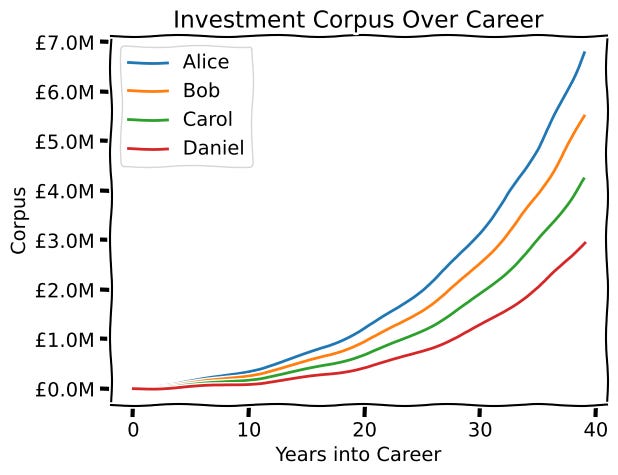

They all invest their leftovers into a boring, reliable 7% return.

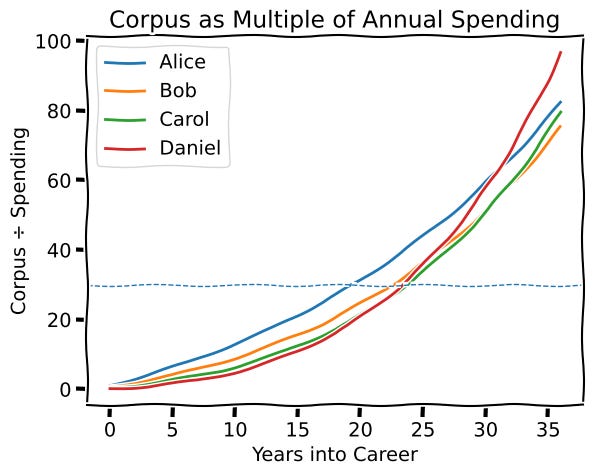

Scenario 1: The “No Shit, Sherlock” Graph

Unsurprisingly, Alice’s bank account starts looking like a hockey stick while Daniel’s looks like a gentle slope. Because Alice saves 50% of her income while Daniel saves barely 12%, she isn’t just “wealthier”—she’s playing a different game.

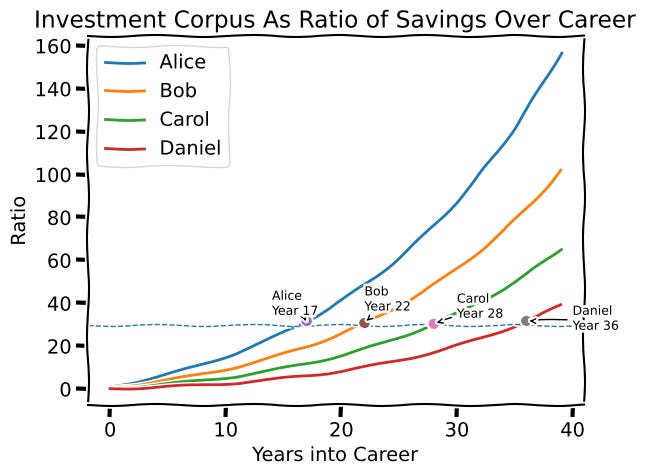

Remember, however, that Financial independence is whenever your corpus reaches roughly 30x your spending (I am buffering the normally used safe-withdrawal rate of 4% down to 3.33% to build a bit of buffer)

But here is the kicker: Alice hits Financial Independence (FI) at age 40, or in 17 years. Why? Not just because she has more money, but because her “Freedom Number” is half of Daniel’s. She’s climbing a shorter mountain with better gear.

Scenario 2: The “Late Bloomer” Epiphany

Let’s say our heroes spent their early years being “young and dumb.” Even though they don’t spend their money, they blew their savings on crypto scams, NFTs, SPACs, or other bad investment choices. Or they are extremely responsible and help out their families with their savings. Eventually, they “find religion” (and Vanguard) and start investing properly at 7%.

If the goal is to retire at 65 (current UK retirement age), how long can they afford to not be on the compounding train?

Alice, with her low overhead, doesn’t even need to start until she’s 40. Meanwhile, Carol needs to have her life together by age 27, not too long after her career starts. Daniel stands no chance in this scenario.

The lesson: A low cost of living is a time machine. It buys you the right to make mistakes.

Scenario 3: The Turtle vs. The Golden Hare

Now, let’s make it unfair.

Alice is a “low-flyer”: 2% raises, promotions every 7 years.

Daniel is a “high-flyer”: 5% raises, promotions every 4 years.

(and Bob and Carol along the continuum)

Even with a “worse” career, Alice still crosses the finish line first. Daniel is trying to fill a massive swimming pool with a firehose. It’s impressive to watch, but it takes forever to get deep enough to dive in. Alice is just trying to fill a bucket with a garden hose. She’s ready to go for a swim while Daniel is still watching the water level slowly creep up the deep end.

The Hard Truth

In the real world, being Alice is hard. It means saying no to the fancy car, the upgraded flat, and the third vacation. It takes willpower. But being Daniel is also hard - it’s the silent stress of knowing your lifestyle is a house of cards that requires a high-octane salary just to keep the lights on.

The takeaway is simple: A lower spending path is the ultimate cheat code. It allows you to:

Survive a slower career path without panic.

Absorb financial body blows (job losses, bad investments) without folding.

Exit the rat race while you still have the knees to enjoy it.

The choice isn’t just about how much you make - it’s about how much you need.

What does your glide path look like? Are you building a mountain, or just a very expensive treadmill?

On that note, Happy Investing!