The Trade Desk: A Potential Opportunity

I’m writing about The Trade Desk (NASDAQ: TTD), which might present an interesting opportunity. Founded in 2009, TTD is a programmatic advertising technology platform.

For the uninitiated, most modern advertising is bought and sold in near real-time—essentially while you are reading an article or watching a video online, an auction takes place in milliseconds to determine which ad gets shown. The highest bidder wins, and the process repeats continuously across billions of impressions.

In this ecosystem, technology companies typically operate as Supply Side Platforms (SSPs) representing sellers, Demand Side Platforms (DSPs) representing buyers, or Ad Exchanges, which sit in between. The Trade Desk primarily operates as a DSP, helping buyers—brands or media agencies—connect to the right ad inventory.

Media agencies, for example, run teams called “Trading Desks” to connect their clients’ campaigns with the right online inventory. TTD was formed to facilitate this process—hence the name, The Trade Desk.

(Nb: I spent eight years at Quantcast, which also runs its own DSP. While we competed in parts of the market, over the years Quantcast has shifted to a niche focus, and I no longer consider TTD and Quantcast direct competitors. I own shares in both companies today and wish them both success. The advertising market is enormous, and both companies can thrive without ever capturing more than a fraction of total market share.)

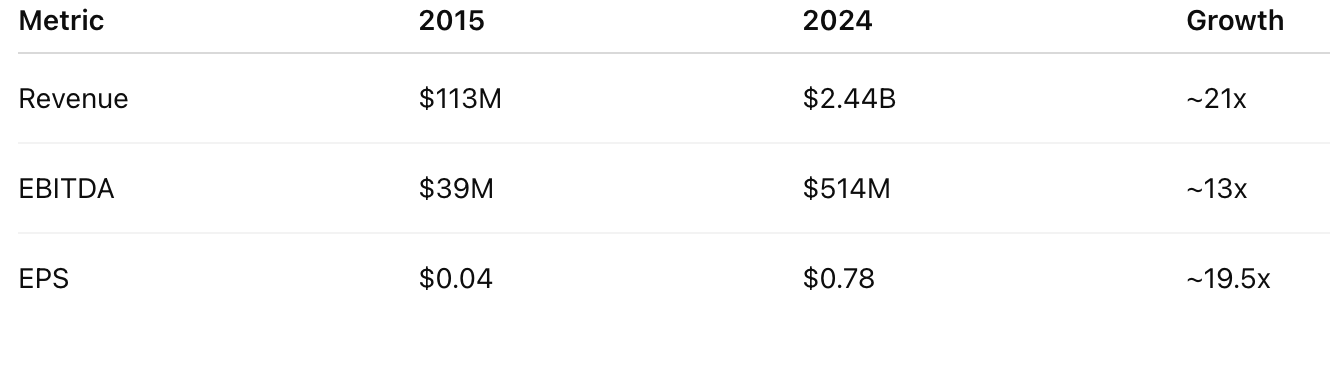

Financial Performance

TTD’s financial history has been impressive:

Revenue growth remains strong: 31%, 23%, and 25% YoY in 2022, 2023, and 2024, respectively. Early 2025 results show 25% growth in Q1 and 18% in Q2. Investors who got in at IPO ($3.01, adjusted for 10:1 stock split) have seen ~15x returns over nine years.

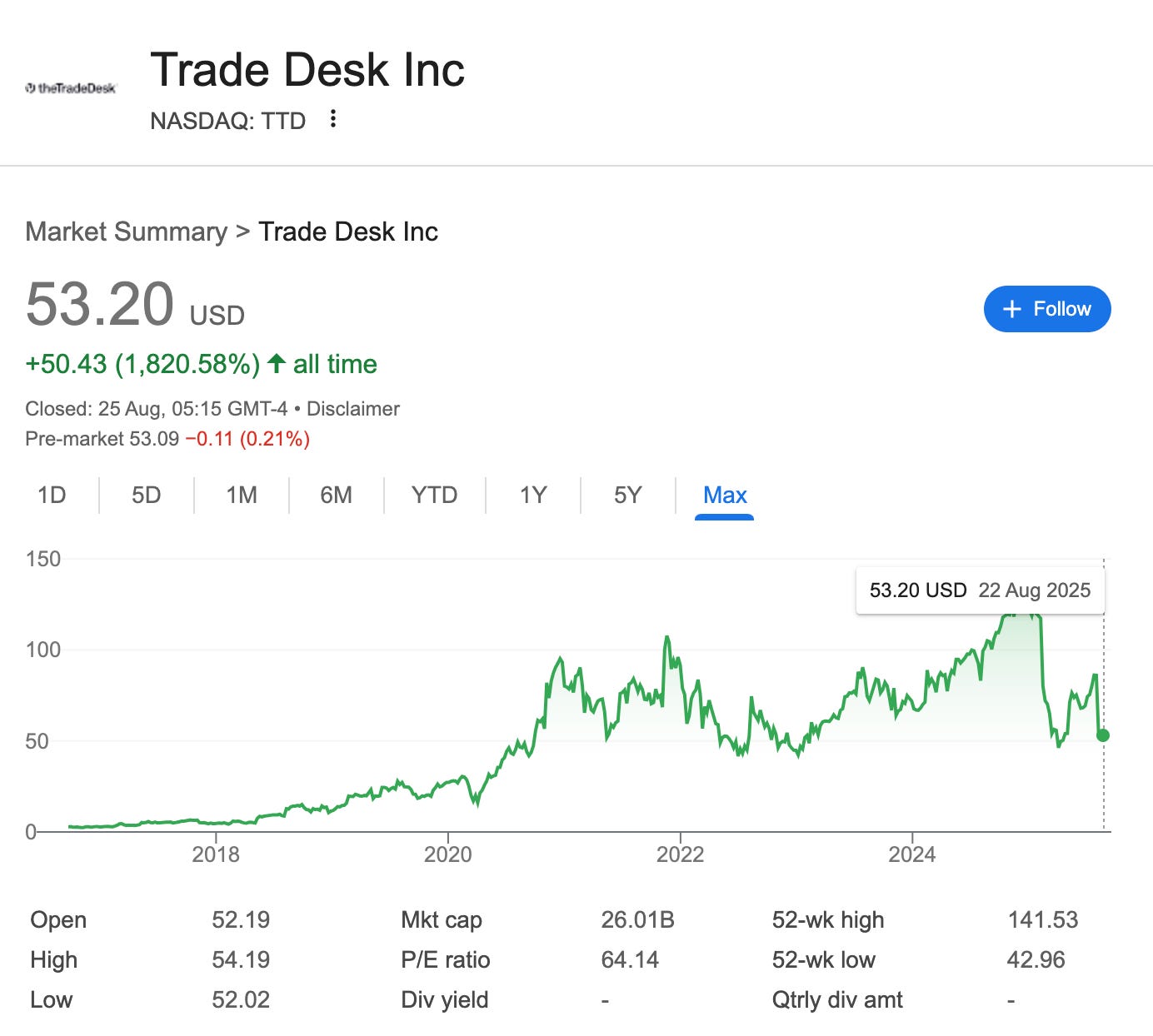

I personally held a small allocation averaging $62 that I sold around $109, believing the valuation had become rich, along with some consolidation motivations. Since then, the stock has roughly halved, reflecting concerns about slowing growth, pressure from walled gardens (Google, Meta, Amazon), and valuation adjustments—from ~25x revenue to ~13x.

Put together, The Trade Desk has been an extremely well-run company, with a long history of growth and converting that growth into solid financials and shareholder returns. Personally, I held a small allocation averaging around $62 per share and sold at roughly $109. At the time, I thought the valuation was too rich and I was consolidating my portfolio toward my highest conviction names.

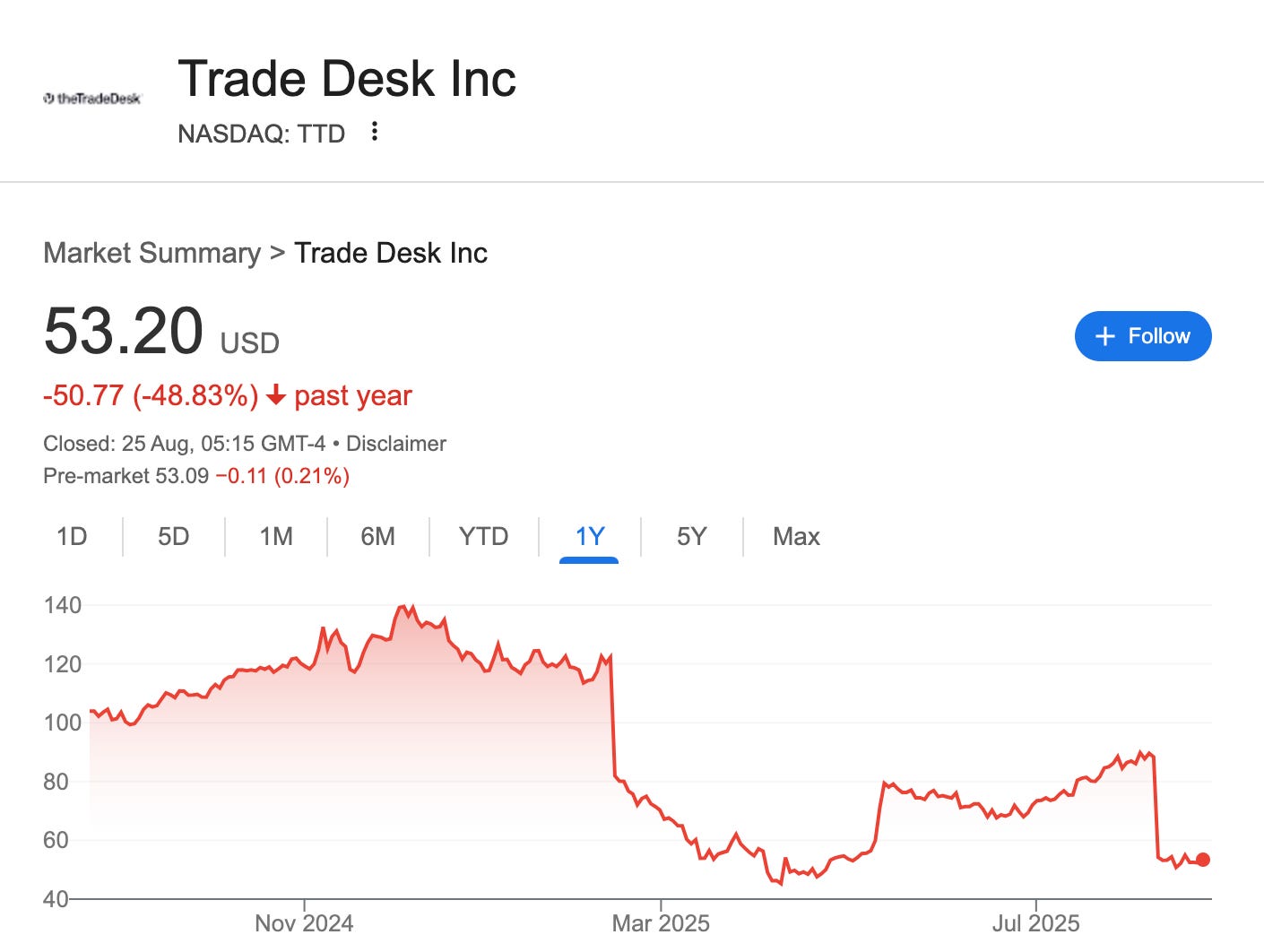

Recent Price Action and Market Concerns

Since I sold, the stock has almost halved in value. In fact, it has a couple of downgrades in recent history, both around quarterly results. These reflect a combination of factors:

Slowing growth: Recent quarters and forward guidance suggest revenue growth is moderating.

Valuation adjustment: With growth slowing, the stock’s multiple has compressed from ~25x revenue to closer to ~13x. While still elevated, this represents a significant correction.

Competitive pressure from walled gardens: Google, Meta, and Amazon control much of the premium ad inventory (YouTube, Google Search, Facebook, Instagram, Amazon) and limit access for players like TTD. Amazon, in particular, has been expanding its market share, raising questions about TTD’s total addressable market.

These are valid concerns, and the stock’s recent downgrade largely follows expected market dynamics.

Current Positioning

Even with all of those concerns, this is a company that has done very well with lots of the right dynamics for a tech growth company. TTD has weathered ups and downs before and has consistently recovered. It remains founder-led, with Jeff Green reportedly maintaining a strong culture. Engineering teams continue to attract and retain talent, which is critical in this market.

Strategically, TTD is large enough to be noticed but not so large as to be hampered by antitrust concerns. Its recent inclusion in the S&P 500 may bring additional index-driven buying over time, though short-term price movements have been volatile.

Potential Upside

Looking ahead, a simple scenario illustrates potential value:

Base case: 15% growth in 2025–2026 → ~12x sales multiple → ~$38B market cap (~50% upside).

Optimistic case: 18% growth → ~$42B (~double current value).

Historically, TTD has shown it can grow, adapt, and deliver shareholder value.

For those familiar with options, the stock offers a deep option pool, allowing alternative ways to participate. Trades like risk reversals or call spreads could offer leveraged exposure if the stock re-rates—but these carry their own risks.

Takeaway

The Trade Desk is not a “slam dunk” by any means, but it’s a well-run, founder-led company with a strong track record of growth and financial performance. Slower growth and competition from walled gardens explain recent price weakness, but strategic positioning, talented teams, and S&P 500 inclusion suggest potential for a meaningful rebound.

Risk remains, as always—but for investors willing to consider it, TTD may warrant a closer look.

With that, Happy Investing!

Disclaimer: I am not your financial advisor and bear no fiduciary responsibility. This post is only for educational and entertainment purposes. Do your own due diligence before investing in any securities. I may hold or enter into, a position in any of the stocks mentioned above. The above is NOT a solicitation to either buy or sell the securities listed in this post.